PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939657

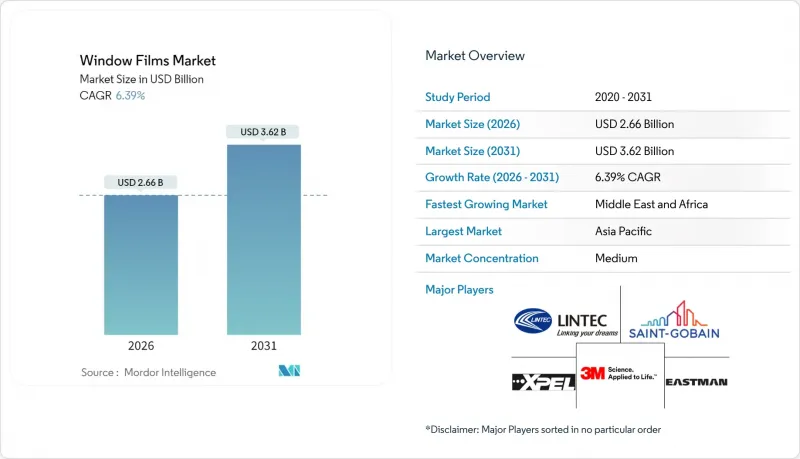

Window Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Window Films market size in 2026 is estimated at USD 2.66 billion, growing from 2025 value of USD 2.50 billion with 2031 projections showing USD 3.62 billion, growing at 6.39% CAGR over 2026-2031.

Strong demand pivots from basic solar control toward multi-functional films that combine energy management, safety, and connectivity benefits, increasingly specified in automotive, building, and specialty applications. Net-zero building mandates accelerate retrofit activity, while an expanding electric-vehicle (EV) fleet and rapid glazing replacement cycles keep automotive volumes buoyant. Suppliers are introducing nanoceramic and low-emissivity constructions that meet stringent energy-code requirements without compromising the radio-wave transparency required for 5G-enabled driver-assistance systems. Asia-Pacific remains the production and consumption hub, yet Middle-East and Africa emerges as the fastest-growing geography as mega-projects in Saudi Arabia and the UAE embrace high-performance glazing. Market concentration stays moderate because leading incumbents defend their positions through innovation and regional capacity expansion, even as electrochromic smart glass and low-cost commodity films intensify competitive pressure.

Global Window Films Market Trends and Insights

Growing demand for safety and security films

Heightened awareness of active-threat scenarios drives wider adoption of 24-mil security laminates that retain glass fragments during forced entry or blast events. Installers are increasingly specifying multi-layer urethane constructions that surpass legacy polyester products in terms of tear resistance and edge-grip performance. Facility managers value the ability to combine intrusion mitigation with UV filtration, allowing a single product to address both safety and energy challenges. Insurance premium rebates in hurricane-prone regions further stimulate retrofit activity. The technology is migrating from high-risk government sites into schools, retail chains, and mixed-use towers as stakeholders seek cost-effective envelope hardening. Manufacturers answer the trend with security films certified under ANSI Z97.1 and EN 12600 impact protocols, reinforcing their relevance in global building codes.

Net-zero mandates driving energy-saving solar-control films

The EU Energy Performance of Buildings Directive and California's Title 24 cap glazing U-factor and solar heat-gain coefficients, pushing owners to upgrade existing windows rather than pursue costly replacements. High-performance solar-control films demonstrate immediate Energy Performance Certificate uplifts, enabling property portfolios to meet 2030 decarbonization targets. Nanoceramic formulations cut infrared transmittance while preserving daylight, an important factor in wellness-oriented interior design. Research prototypes of smart photochromic films indicate potential annual energy-use reductions of up to 35% when paired with low-E double glazing. Roll-to-roll manufacturing keeps price points competitive against electrochromic glass, positioning films as the mainstream retrofit path for millions of buildings needing efficiency gains.

Technical and warranty issues during installation

Advanced multi-layer films require pristine surface preparation, controlled humidity, and precise squeegee techniques. Variations in installer skill create bubbles, edge lift, and optical haze that trigger warranty disputes, particularly in price-sensitive emerging markets. Trade associations publish visual-quality standards, yet enforcement remains uneven. Manufacturers answer with expanded certification courses and pre-cut kits, but these initiatives raise channel costs and limit bespoke solutions. In the automotive aftermarket, compound curves amplify complexity, prolonging installation time and inviting consumer dissatisfaction when defects appear.

Other drivers and restraints analyzed in the detailed report include:

- Rapid glazing replacement cycle in automotive aftermarket

- Insurance-premium rebates for hurricane-resistant films

- VOC-emission regulations limiting solvent-based adhesives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar-control and UV-blocking constructions retained a 40.89% slice of the window films market in 2025, confirming their status as the go-to retrofit option for instant heat-gain reduction and occupant comfort. Strong sales track widespread awareness of fading protection in furniture, artworks, and automotive interiors. Premium nanoceramic variants command higher average selling prices thanks to neutral color rendition and longevity in harsh climates. The market now witnesses hybrid products that fuse spectrally selective coatings with decorative patterns, appealing to retail storefronts seeking brand differentiation without sacrificing performance. Suppliers promote metallized-free stacks to avert radio interference in connected buildings and vehicles.

Insulating/low-E products post the fastest 7.26% CAGR through 2031, buoyed by net-zero policy targets and rising heating-degree-day counts in mid-latitude regions. Their multi-layer sputtered stacks cut conducted and radiative losses, allowing single-pane windows to approach double-pane performance metrics at a fraction of replacement cost. Demonstrated payback periods of three years or less in temperate zones catalyze adoption among facility managers retrofitting Class-B office stock. The window films market size for insulating/low-E solutions is projected to surge as building codes tighten, yet production complexity and higher installation skill requirements still confine uptake to professional channels. Decorative, privacy and safety niches continue serving specialized demand pockets in hospitality, healthcare and critical-infrastructure verticals.

The Window Films Market Report is Segmented by Type (Solar-Control and UV-Blocking Films, Decorative Films, Safety and Security Films, Privacy Films, Insulating/Low-E Films, Others), End-User Industry (Automotive, Building and Construction, Marine, Aerospace, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 45.84% of 2025 global revenue, thanks to China's dual dominance in construction floor space and vehicle production. Ambitious building-energy regulations in Japan and South Korea propel premium low-E and smart-film installations, while India and ASEAN nations show double-digit growth off lower bases as urbanization surges. Local supply chains grant competitive cost positions, evidenced by large-scale capacity additions in China and Singapore announced by major multinationals. Regional distributors bundle films with shading devices and building-automation sensors, highlighting holistic facade value propositions.

Middle-East and Africa records the highest 6.83% CAGR through 2031, underpinned by Saudi Vision 2030 giga-projects that must endure extreme solar loads and meet LEED or Estidama green-building criteria. Developers in Riyadh and Dubai specify high-selectivity films to curb HVAC bills while preserving expansive glass facades emblematic of contemporary architecture. Skilled-labor shortages and competing construction material demand occasionally constrain installation capacity, prompting suppliers to train applicators under accelerated programs and pre-qualify subcontractors for mega-project packages.

North America and Europe constitute mature arenas where growth relies on code-driven retrofits and premium segment penetration. The EU's mandate to refurbish the worst-performing 16% of commercial stock by 2030 keeps demand resilient despite macroeconomic swings. U.S. state-level incentives for deep-energy retrofits feed a steady pipeline, and corporate decarbonization pledges extend momentum. South America follows with moderate uptake as economic cycles and currency volatility temper investment, yet urban centers such as Sao Paulo and Santiago adopt higher glazing standards that open opportunities for mid-tier performance films.

- 3M

- Armolan Greece

- Avery Dennison Corporation

- Eastman Chemical Company

- Erickson International, LLC

- Garware Hi-Tech Films.

- HYOSUNG CHEMICAL

- Johnson Window Films Inc.

- Lintec Corporation

- Madico

- Nexfil

- Rayno Window Film

- Saint-Gobain

- TORAY INDUSTRIES INC.

- WINTECH CO., LTD.

- XPEL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for safety and security films

- 4.2.2 Net-zero mandates driving energy-saving solar-control films

- 4.2.3 Rapid glazing replacement cycle in automotive aftermarket

- 4.2.4 Surge in data-centre facade retrofits for Infrared rejection

- 4.2.5 Insurance-premium rebates for hurricane-resistant films

- 4.3 Market Restraints

- 4.3.1 Technical and warranty issues during installation

- 4.3.2 Competition from electro-chromic smart glass

- 4.3.3 VOC-emission regulations limiting solvent-based adhesives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Solar-control and UV-blocking Films

- 5.1.2 Decorative Films

- 5.1.3 Safety and Security Films

- 5.1.4 Privacy Films

- 5.1.5 Insulating/Low-E Films

- 5.1.6 Others

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Marine

- 5.2.4 Aerospace

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Russia

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core segments, Financials, Strategic info, Market share, Products and Services, Recent developments)

- 6.4.1 3M

- 6.4.2 Armolan Greece

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Eastman Chemical Company

- 6.4.5 Erickson International, LLC

- 6.4.6 Garware Hi-Tech Films.

- 6.4.7 HYOSUNG CHEMICAL

- 6.4.8 Johnson Window Films Inc.

- 6.4.9 Lintec Corporation

- 6.4.10 Madico

- 6.4.11 Nexfil

- 6.4.12 Rayno Window Film

- 6.4.13 Saint-Gobain

- 6.4.14 TORAY INDUSTRIES INC.

- 6.4.15 WINTECH CO., LTD.

- 6.4.16 XPEL

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment