PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939675

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939675

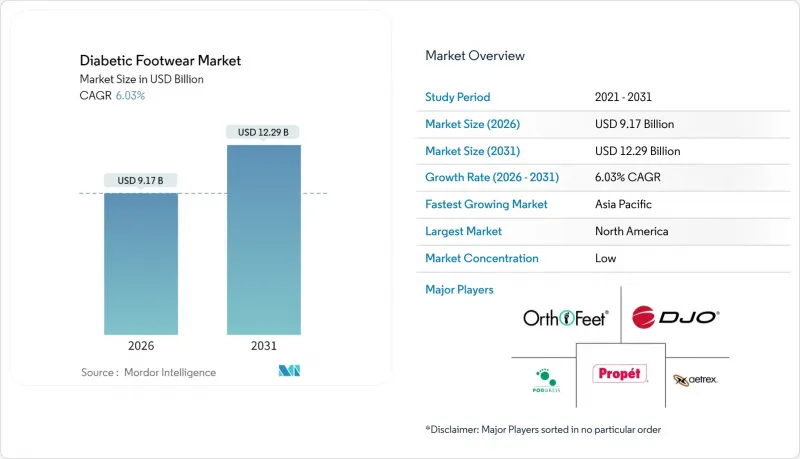

Diabetic Footwear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The global diabetic footwear market was valued at USD 8.65 billion in 2025 and estimated to grow from USD 9.17 billion in 2026 to reach USD 12.29 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031).

Surging diabetes prevalence, rapid advancements in smart-fit technologies, and an expanding reimbursement landscape for preventive care are driving the growth of the diabetic footwear market. Notably, while 15% of diabetics face foot ulcers in their lifetime, early prescription of protective shoes or insoles can prevent 85% of potential amputations. This highlights the critical role of diabetic footwear in reducing severe complications and improving patient outcomes. Industry frontrunners are not only adopting ISO 13485 quality systems and securing FDA Class I registrations to bolster brand trust, but they're also delving into mass customization and sensor integration. These innovations are transforming diabetic footwear from passive protective gear into connected medical devices capable of monitoring foot health in real-time. In a notable trend, insurers across Asia-Pacific and Latin America are incorporating therapeutic shoes into their value-based care packages, hinting at a sustained demand. This inclusion reflects a growing recognition of diabetic footwear as an essential component of preventive healthcare strategies. While competitive intensity remains moderate, it's on the rise. Athletic footwear behemoths are forging 3-D printing partnerships, enabling them to provide on-demand personalized insoles. This move is encroaching on the territory once dominated by specialized orthotic brands, signaling a shift in market dynamics and increasing competition.

Global Diabetic Footwear Market Trends and Insights

Rising global diabetic population

By 2045, the number of adults with diabetes worldwide is projected to surge from 538 million in 2021 to 783 million, translating to over 10 million potential new candidates for diabetic footwear each year. As the duration of diabetes increases, so do complications like neuropathy and peripheral vascular disease. This trend prompts clinicians to recommend protective footwear almost immediately after diagnosis. In India, projections indicate that by 2045, 134 million adults will be living with diabetes. This surge underscores the need for a comprehensive ecosystem for therapeutic shoes, encompassing scanning kiosks, trained pedorthists, and localized manufacturing. Hospitals across China, Saudi Arabia, and Brazil are proactively bundling therapeutic shoes into insurance-covered disease-management programs. This move aims to mitigate the average downstream amputation costs of USD 13,000 per ulcer episode in the U.S. Consequently, the diabetic footwear market benefits from a uniquely predictable demand curve, driven by demographic trends, setting it apart from many other orthopedic devices.

Growing awareness of diabetic foot issues

With clinical consensus asserting that 85% of diabetes-related amputations are preventable, footwear has transitioned from being an elective accessory to a crucial piece of medical equipment. Health systems are now advocating for annual foot examinations, and Medicare has taken a significant step by reimbursing eligible beneficiaries for one pair of therapeutic shoes and up to three pairs of insoles annually under HCPCS A5500. This policy has a direct impact, stimulating purchase volumes. Concurrently, smart insoles, embedded with pressure and temperature sensors, are revolutionizing patient care. They offer real-time alerts when ulcer risk thresholds are crossed, establishing data-driven feedback loops that bolster patient adherence. Furthermore, peer-reviewed studies highlight the efficacy of smart socks. Equipped with SpO2 sensors, they can detect micro-circulation changes up to 48 hours prior to tissue breakdown. This early detection provides clinicians with a crucial window to modify footwear or off-loading protocols. As knowledge disseminates through endocrinology clinics, community health workers, and digital coaches, the diabetic footwear market is witnessing a surge in informed buyers. These buyers increasingly perceive therapeutic shoes not just as footwear, but as a safeguard against major surgeries.

High price of certified diabetic footwear

Therapeutic shoes, priced between USD 200 and USD 600 per pair, command a significant premium compared to mass-market sneakers, which sell for under USD 80. These shoes are specifically designed to address medical needs, such as accommodating foot deformities or preventing complications in diabetic patients. Manufacturers shoulder costs associated with Plastazote linings, extra-depth construction, and small-batch production, all of which are essential for ensuring the therapeutic efficacy of the footwear. Additionally, adhering to FDA design-control and ISO 13485 documentation requirements further inflates overheads, as these standards ensure product safety and quality. In low-income markets, insurance typically covers only up to 30% of the invoice, leaving patients to shoulder the remainder, which can be a significant financial burden. Price resistance is evident: distributor surveys indicate that a 10% price increase can lead to an 18% drop in unit sales in Southeast Asia. This resistance highlights the sensitivity of these markets to price changes, which can hinder broader adoption. Without economies of scale or innovative materials to drive down prices, the diabetic footwear market may face challenges in gaining traction outside of developed economies, where higher disposable incomes and better insurance coverage make these products more accessible.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of online specialty retail

- Rapid growth in geriatric population

- Proliferation of counterfeit/low-quality products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By the end of 2025, shoes dominated the diabetic footwear market, making up 52.01% of total sales. Their popularity stems from their adaptability in cooler regions, where full-coverage designs are essential for winter protection and formal occasions. Demand remains robust in professional settings, as patients navigate the balance between clinical needs and aesthetic appeal. Shoes provide crucial structural support for advanced foot deformities and neuropathy, underscoring their importance for high-risk populations. Manufacturers are pouring investments into material innovations, merging lightweight uppers with rigid soles to boost comfort without sacrificing off-loading efficiency. The addition of Bluetooth-enabled pressure sensors is solidifying shoes' status as the gold standard in connected diabetic care, fostering data-rich ecosystems beneficial for both patients and clinicians in long-term management.

Meanwhile, sandals are poised for the swiftest growth, with a projected CAGR of 7.10% through 2031. This surge is evident in tropical and subtropical regions, where patients prioritize breathability alongside therapeutic benefits. Clinical research increasingly supports open-toe designs, indicating that when used with custom insoles, sandals match shoes in off-loading plantar pressure. Innovations like antimicrobial footbeds are driving adoption by mitigating moisture-related infections. The segment is also witnessing advancements, with second-generation 3D printers crafting lightweight TPU midsoles that shed up to 25% of their weight while maintaining essential stiffness. As sandals approach the milestone of USD 2.07 billion by 2031, they're transitioning from mere seasonal options to primary diabetic solutions, thanks to collaborative efforts between global brands and local OEMs harnessing cloud-based gait analytics.

The Diabetic Footwear Market Report is Segmented by Product Type (Shoes, Sandals, Slippers), End User (Men, Women), Distribution Channel (Offline Retail Stores, Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America dominated the diabetic footwear market, capturing a 39.30% revenue share. This was bolstered by the HCPCS A5500 coverage, which reimburses up to USD 150 per pair, along with three sets of insoles each year. With a density of over one certified pedorthist for every 35,000 residents, high-risk patients enjoy enhanced access. Domestic players like Viant Medical not only cater to local demands from their ISO 13485 certified plants but also export to Europe and the Middle East. Furthermore, digital startups in the region are at the forefront, developing AI-driven fit engines. These engines interface securely with EHR systems, enabling clinicians to monitor pressure data over time and validate future prescriptions.

Asia-Pacific is on a rapid ascent, boasting an 7.95% CAGR projected through 2031. In India, China, and Indonesia, urbanization, dietary shifts, and an aging populace are driving a surge in diabetes cases. In response, governments are rolling out disease-management initiatives, offering foot screening vouchers and subsidized footwear. Highlighting regional innovation, Singapore's CFOOT is teaming up with Nanyang Technological University to develop algorithms that customize lasts for Asian foot shapes. Meanwhile, local manufacturing hubs are emerging in Vietnam and Malaysia, aiming to streamline supply chains and sidestep import duties. This expansion not only broadens the market's reach but also reduces retail prices by as much as 12%.

Europe experiences steady growth, bolstered by a stringent regulatory framework and publicly funded preventive measures. The continent hosts primary suppliers of Plastazote and memory foams, crucial for off-loading midsoles, ensuring a secure supply chain. Meanwhile, Latin America and the Middle East and Africa are carving out their niches. In a significant move, Brazil's SUS health system included diabetic footwear in its 2024 essential-device list, a decision poised to boost local sales by 400,000 pairs each year. In the Gulf Cooperation Council states, as affluence rises, so does the appetite for premium smart sandals. These innovative sandals not only offer comfort but also gather plantar pressure data, relaying it to cloud dashboards for physician analysis. With supply chains evolving, the diabetic footwear market is set to flourish in these regions, adapting its product offerings to local preferences.

- Aetrex Worldwide Inc.

- Orthofeet Inc.

- DJO Global Inc. (Dr. Comfort)

- Dr. Zen Products Inc.

- Drew Shoe Corporation

- Podartis srl

- Propet USA Inc.

- Hanger Inc.

- Biomotion Healthcare

- Pilgrim Shoes

- DARCO International Inc.

- Apex Foot Health Industries LLC

- Advance Diabetic Solutions

- Finn Comfort

- Medline Industries LP

- Hochste Healthcare Private Limited

- Gravity Defyer Corp.

- StepWise Health

- Atlantic Footcare Inc.

- Anodyne Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global diabetic population

- 4.2.2 Growing awareness of diabetic foot issues

- 4.2.3 Expansion of online specialty retail

- 4.2.4 Rapid growth in geriatric population

- 4.2.5 Mass-customization via 3-D printing

- 4.2.6 Emerging reimbursement in developing markets

- 4.3 Market Restraints

- 4.3.1 High price of certified diabetic footwear

- 4.3.2 Proliferation of counterfeit/low-quality products

- 4.3.3 Absence of global prescription standards

- 4.3.4 Supply-chain dependence on specialized foams

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Shoes

- 5.1.2 Sandals

- 5.1.3 Slippers

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.3 By Distribution Channel

- 5.3.1 Offline Retail Stores

- 5.3.2 Online Retail Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aetrex Worldwide Inc.

- 6.4.2 Orthofeet Inc.

- 6.4.3 DJO Global Inc. (Dr. Comfort)

- 6.4.4 Dr. Zen Products Inc.

- 6.4.5 Drew Shoe Corporation

- 6.4.6 Podartis srl

- 6.4.7 Propet USA Inc.

- 6.4.8 Hanger Inc.

- 6.4.9 Biomotion Healthcare

- 6.4.10 Pilgrim Shoes

- 6.4.11 DARCO International Inc.

- 6.4.12 Apex Foot Health Industries LLC

- 6.4.13 Advance Diabetic Solutions

- 6.4.14 Finn Comfort

- 6.4.15 Medline Industries LP

- 6.4.16 Hochste Healthcare Private Limited

- 6.4.17 Gravity Defyer Corp.

- 6.4.18 StepWise Health

- 6.4.19 Atlantic Footcare Inc.

- 6.4.20 Anodyne Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK