PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939680

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939680

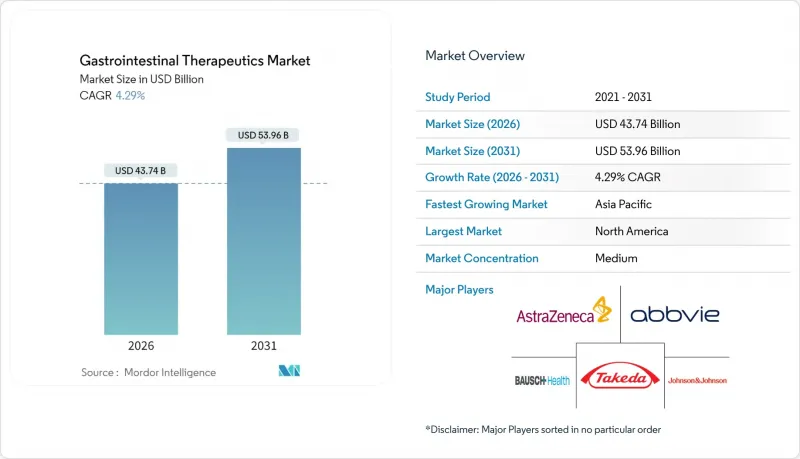

Gastrointestinal Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The gastrointestinal therapeutics market is expected to grow from USD 41.94 billion in 2025 to USD 43.74 billion in 2026 and is forecast to reach USD 53.96 billion by 2031 at 4.29% CAGR over 2026-2031.

Robust demand stems from a rising digestive-disease burden, widening adoption of biologics and biosimilars, and continuous investment in microbiome-based pipelines. Specialist shortages in many countries, especially rural regions, intensify reliance on telehealth and AI-guided diagnostic tools, while regulatory support for biosimilar interchangeability accelerates price competition. Companies that combine advanced drug platforms with digital health services strengthen market access, and large-volume subcutaneous delivery systems position injectables as a viable alternative to traditional oral therapies. Meanwhile, regional expansion in Asia-Pacific, driven by healthcare infrastructure upgrades and dietary westernization, offsets pricing pressure in North America and Europe, making the gastrointestinal therapeutics market an attractive long-term play for diversified portfolios.

Global Gastrointestinal Therapeutics Market Trends and Insights

Increasing Prevalence of GI Disorders

Colorectal-cancer screening age was lowered to 45 years in the United States, adding millions of procedures annually and amplifying demand for both diagnostics and follow-up therapeutics. Rising incidence of inflammatory bowel disease in rapidly urbanizing Asian populations underscores the need for advanced biologics that surpass acid-suppression drugs in efficacy. Expanded national screening programs in China and India funnel more patients into treatment pathways, and this earlier detection improves long-term therapeutic adherence. Government reimbursement for preventive colonoscopy further buttresses prescription volumes for antispasmodics and prokinetic agents. Collectively, these factors lift the gastrointestinal therapeutics market by enlarging the treated-patient pool and extending treatment durations.

Aging Population & Lifestyle Shifts

Japan already records 29.1% of its citizens aged >=65 years, and similar trajectories in Europe and North America increase chronic proton-pump-inhibitor use for reflux management. Sedentary behavior and processed-food consumption heighten functional gastrointestinal disorders, prompting broader uptake of prokinetics and microbiome modulators. Obesity magnifies gastroesophageal reflux disease prevalence, feeding sustained PPI prescriptions despite generic erosion. Lifestyle-induced stress links to irritable bowel syndrome, reinforcing demand for low-dose antidepressant adjuncts and antispasmodics. Overall, demographic and behavioral convergence lengthens therapy courses, driving stable revenue streams in the gastrointestinal therapeutics market.

High Biologic Therapy Costs

Annual biologic treatment can exceed USD 50,000, straining public and private payers that increasingly impose prior-authorization hurdles. Value-based contracts tie reimbursement to real-world outcomes, compelling manufacturers to fund post-marketing studies. Specialty pharmacies consolidate to negotiate steeper discounts, eroding gross margins yet expanding patient reach through copay-assistance programs. Emerging-market governments explore pooled procurement to lower unit prices, but constrained budgets delay biologic uptake compared with small-molecule alternatives. Although biosimilars promise relief, originators often counter with life-cycle-management strategies such as high-concentration formulations, prolonging price rigidity.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Biologics & Biosimilars

- Microbiome-Based Live Biotherapeutics Pipeline

- Limited Specialist Availability in Emerging Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Proton pump inhibitors remained the revenue anchor in 2025, holding 23.78% gastrointestinal therapeutics market share, underpinned by widespread management of gastroesophageal reflux disease and ulcer prophylaxis. Branded PPIs still command premiums in hospital formularies where rapid-acting IV formulations are required for acute bleeding, though generics dominate retail channels. The gastrointestinal therapeutics market size attributable to PPIs is expected to plateau as guideline revisions advocate step-down therapy to minimize long-term adverse effects. In parallel, the biologics segment captures incremental spend through anti-TNF agents, IL-12/23 inhibitors, and JAK inhibitors, but faces biosimilar erosion post-2025. Antibiotics, led by rifaximin, retain niche applications in hepatic encephalopathy and small-intestinal bacterial overgrowth, aided by label expansions.

Microbiome-based therapies comprise the fastest-growing drug class at a 4.33% CAGR, albeit from a low base, benefiting from VOWST's commercial traction and promising pipelines like SER-155 for immunocompromised hosts. Live biotherapeutic product standardization and scalable anaerobic manufacturing processes cut production costs, narrowing the price gap with conventional biologics. Pharma-food cross-sector collaborations, as exemplified by Nestle Health Science, infuse diet-adjacent capabilities such as prebiotic adjuncts that enhance colonization. Over the forecast period, the gastrointestinal therapeutics market size for microbiome products is expected to expand as payers accept real-world evidence of relapse reduction in recurrent C. difficile infection.

The Gastrointestinal Therapeutics Market Report is Segmented by Drug Class (Proton Pump Inhibitors, H2 Receptor Antagonists, and More), Disease Indication (GERD, Peptic Ulcer and More), Route of Administration (Oral, Injectable, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 38.61% of global revenue in 2025, propelled by high biologic penetration and supportive reimbursement environments despite pronounced specialist shortages across 69.3% of counties. Tele-gastroenterology networks and capsule endoscopy interpretation centers extend reach, but the backlog for elective colonoscopy still stretches clinician capacity. Biosimilar adoption accelerates after updated interchangeability rules, with payer formularies quickly prioritizing cost-saving options.

Asia-Pacific is the fastest-growing region at a 5.12% CAGR as aging demographics in China and India intersect with government insurance expansion. Urban dietary shifts drive ulcerative colitis and Crohn's disease incidence, steering investment toward biologics manufacturing facilities in Singapore and South Korea. Meanwhile, Japan's super-aged society sustains steady demand for PPIs and prokinetics, although strict HTA controls temper price inflation. Digital-health startups capitalize on smartphone penetration to deliver microbiome-tracking apps, integrating seamlessly with hospital EMR systems to guide personalized therapy.

Europe maintains a balanced outlook, with Germany, the United Kingdom, and France jointly accounting for more than half of regional sales. HTA bodies negotiate aggressive price caps, spurring rapid biosimilar uptake that broadens patient access yet compresses margins. Southern European countries are exploring outcome-based payment models for high-cost biologics, mirroring pilot programs in Scandinavia. In South America and the Middle East & Africa, Brazil and Saudi Arabia spearhead adoption of endoscopy capital equipment and biologics, leveraging public-private partnerships to upgrade hospital infrastructure. Nonetheless, payer fragmentation and import tariffs slow widespread uptake, keeping these regions at an earlier stage of the gastrointestinal therapeutics market development curve.

- Abbvie

- Takeda Pharmaceuticals

- Johnson & Johnson (Janssen Biotech, Inc.)

- Pfizer

- AstraZeneca

- Eli Lilly and Company

- Bristol-Myers Squibb

- Amgen

- GlaxoSmithKline

- Sanofi

- Novartis

- Ironwood Pharmaceuticals

- Dr. Falk Pharma GmbH

- Ferring Pharmaceuticals SA

- Eisai

- Merck

- Bayer

- Boehringer Ingelheim

- Gilead Sciences

- Theravance Biopharma, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing prevalence of GI disorders

- 4.2.2 Aging population & lifestyle shifts

- 4.2.3 Advancements in biologics & biosimilars

- 4.2.4 Expansion of minimally-invasive smart-pill tech

- 4.2.5 Microbiome-based live biotherapeutics pipeline

- 4.2.6 AI-guided drug-repurposing for orphan GI diseases

- 4.3 Market Restraints

- 4.3.1 High biologic therapy costs

- 4.3.2 Stringent reimbursement hurdles

- 4.3.3 Post-2026 patent cliffs driving price erosion

- 4.3.4 Limited specialist availability in emerging nations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Drug Class

- 5.1.1 Proton Pump Inhibitors (PPIs)

- 5.1.2 H2 Receptor Antagonists

- 5.1.3 Antacids & Alginates

- 5.1.4 Prokinetics

- 5.1.5 Laxatives

- 5.1.5.1 Bulk-forming

- 5.1.5.2 Osmotic

- 5.1.5.3 Stimulant

- 5.1.5.4 Lubricant/Emollient

- 5.1.6 Anti-emetics

- 5.1.6.1 5-HT3 Antagonists

- 5.1.6.2 NK1 Antagonists

- 5.1.6.3 Dopamine Antagonists

- 5.1.7 Antispasmodics

- 5.1.8 Biologics & Biosimilars

- 5.1.8.1 Anti-TNF Agents

- 5.1.8.2 Anti-integrin Agents

- 5.1.8.3 IL-12/23 Inhibitors

- 5.1.8.4 JAK Inhibitors (Small-molecule)

- 5.1.8.5 S1P Modulators

- 5.1.9 Antibiotics (e.g., Rifaximin)

- 5.1.10 GLP-2 & GLP-1 Analogues

- 5.1.11 Microbiome-based Therapeutics

- 5.1.12 Others (Bile-acid sequestrants, enzymes)

- 5.2 By Disease Indication

- 5.2.1 Gastro-esophageal Reflux Disease (GERD)

- 5.2.2 Peptic Ulcer Disease

- 5.2.3 Functional Dyspepsia

- 5.2.4 Irritable Bowel Syndrome (IBS)

- 5.2.5 Chronic Idiopathic Constipation (CIC)

- 5.2.6 Ulcerative Colitis

- 5.2.7 Crohn's Disease

- 5.2.8 Clostridioides difficile Infection

- 5.2.9 Short Bowel Syndrome

- 5.2.10 Gastrointestinal Cancer

- 5.2.11 GI Motility Disorders (e.g., Gastroparesis)

- 5.2.12 Others (Eosinophilic Esophagitis, etc.)

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.1.1 Immediate-release

- 5.3.1.2 Delayed / Enteric-coated

- 5.3.1.3 Extended-release

- 5.3.2 Injectable

- 5.3.2.1 Intravenous

- 5.3.2.2 Subcutaneous

- 5.3.3 Rectal

- 5.3.3.1 Suppositories

- 5.3.3.2 Foams / Enemas

- 5.3.4 Parenteral Infusion Pumps

- 5.3.5 Others (Transdermal, Intranasal)

- 5.3.1 Oral

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Specialty Clinics / Infusion Centers

- 5.4.5 Others (Homecare Settings)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Takeda Pharmaceutical Company Limited

- 6.3.3 Johnson & Johnson (Janssen Biotech, Inc.)

- 6.3.4 Pfizer Inc.

- 6.3.5 AstraZeneca plc

- 6.3.6 Eli Lilly and Company

- 6.3.7 Bristol Myers Squibb Company

- 6.3.8 Amgen Inc.

- 6.3.9 GlaxoSmithKline plc

- 6.3.10 Sanofi

- 6.3.11 Novartis AG

- 6.3.12 Ironwood Pharmaceuticals, Inc.

- 6.3.13 Dr. Falk Pharma GmbH

- 6.3.14 Ferring Pharmaceuticals SA

- 6.3.15 Eisai Co., Ltd.

- 6.3.16 Merck & Co., Inc.

- 6.3.17 Bayer AG

- 6.3.18 Boehringer Ingelheim International GmbH

- 6.3.19 Gilead Sciences, Inc.

- 6.3.20 Theravance Biopharma, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment