PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939751

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939751

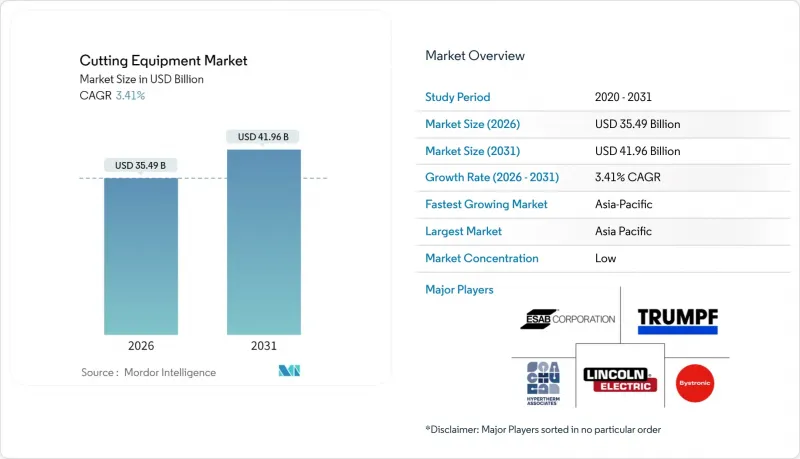

Cutting Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cutting equipment market was valued at USD 34.32 billion in 2025 and estimated to grow from USD 35.49 billion in 2026 to reach USD 41.96 billion by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

Ongoing investments in fiber laser systems, rising automation adoption, and widening material portfolios sustain steady growth even as the marketplace matures. Fiber laser technology already leads the laser segment with a 45.65% share in 2024, and ultrasonic plus AI-enabled systems are broadening the competitive set. Asia-Pacific's manufacturing surge underpins nearly half the global demand, while electrification in automotive and precision needs in electronics pull advanced machinery spending. At the same time, high capital intensity and gaps in skilled labor temper expansion, pushing suppliers toward turnkey, software-rich, and energy-efficient offerings to defend margins and unlock replacement demand.

Global Cutting Equipment Market Trends and Insights

Precision-Critical Fabrication in EV/ICE Automotive & Aerospace

Design tolerances for EV battery housings and next-generation aerospace parts now fall below a millimeter, forcing plants to adopt lasers, water-jets, and ultrasonics that avoid heat-affected distortion. ANDRITZ Schuler's Laser Blanking Line cuts high-strength steel at 45 parts per minute and trims raw-material waste by 17% through intelligent nesting. Similar precision requirements extend to composite recycling, where reclaimed wind-turbine fibers must remain intact to meet mechanical thresholds for reuse. Demand for mixed-material body structures amplifies the need for adaptive cutting parameters and in-line quality control, pushing vendors to embed vision systems and AI analytics within every workstation. As a result, high-specification machinery sees durable replacement demand even in mature plants.

Industry 4.0 Driven CNC/Robotic Automation Surge

Manufacturers increasingly link cutting machines into sensor-rich cells that self-diagnose wear, schedule service, and share production data across the factory network. TRUMPF's TruMatic 5000 couples punch-laser tech with SheetMaster handling to load, cut, and unload parts in one closed loop, shrinking idle time and labor input. Partnerships such as Miller Electric-Novarc apply AI to weld joints previously impossible to automate, easing skilled-worker shortages. Cyber-security solutions from Bystronic and NanoLock now guard connected lasers against ransomware breaches. Collectively, these innovations let plants run small, high-mix batches with fewer operators, reshaping cost structures and accelerating the diffusion of robotics into the cutting equipment market.

High Upfront Capital & Integration Costs

Smart lasers, robots, and storage towers demand not only machine purchase but also reinforced floors, power upgrades, and ERP links, all of which raise project budgets beyond many smaller shops. TRUMPF's fully automated cells illustrate the hurdle: the laser, punch head, and SheetMaster loader require synchronized software licenses and safety fencing that push payback periods past three years for low-volume users. Public-sector grants cover up to 50% of outlays, yet application cycles and matching-fund rules can defer purchase decisions. Meanwhile, compliance with ISO 12100 machine-safety norms mandates guarding and risk assessments that add further cost layers. Until prices taper or leasing models proliferate, capital intensity will cap penetration rates among SMEs.

Other drivers and restraints analyzed in the detailed report include:

- Manufacturing Capacity Boom Across APAC

- Post-Pandemic Cap-Ex Incentives for Energy-Efficient Fiber Lasers

- Global Shortage of Skilled CNC/CAM Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber lasers accounted for 45.12% of 2025 revenue, maintaining the largest slice of the cutting equipment market. Their high electrical-to-optical efficiency, lower service needs, and tight kerf widths suit both ferrous and non-ferrous metals. nLIGHT's Corona beam-shaping unit showcases the segment's pace, letting users toggle ring modes on the fly for thick or thin plates without optics swaps. CO2 platforms still survive in shops focused on thicker stainless edges, but incremental sales now gravitate toward fiber as ownership costs continue to compress.

Laser demand also benefits from tighter floor-space utilization, as single-head machines reach kilowatt ratings once reserved for large gantry systems. Over 2026-2031, ultrasonic and hybrid laser-plasma rigs are expected to post the fastest 4.98% CAGR, yet they start from a narrower base. Supplier roadmaps bundle AI vision, automated nozzle changeovers, and predictive lens cleaning, further cementing fiber's hold on the cutting equipment market.

Semi-automated setups held 42.06% of the cutting equipment market size in 2025, reflecting widespread use of shuttle tables, nesting software, and operator-assisted loading. Plants enjoy flexibility while trimming manpower, making semi-auto the entry point for many SMEs. Yet fully robotic cells, integrating gantry loaders and AGVs, look set for a 5.07% CAGR through 2031 as ISO 10218-2:2025 eases cobot adoption.

Return-on-investment improves when multiple peripheral tasks, such as deburring and part sorting, join the same work cell. TRUMPF's sensors check suction-cup vacuum in real time, avoiding crashed cuts and raising lights-out reliability. Meanwhile, low-cost cobots with 15 kg payloads now operate at under USD 30,000, putting unattended night shifts within reach for job shops. These trends point to automation's rising share of the cutting equipment market, even if human-in-the-loop workflows persist.

The Cutting Equipment Market Report is Segmented by Technology (Laser, Plasma, and More), by Automation Level (Manual, Semi-Automated, and Robotic/Fully-automated), by End-User Industry (Automotive, Aerospace & Defense, and More), by Material Type (Ferrous Metals, Non-Ferrous Metals, Composites, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 48.62% of 2025 revenue and is on course for a 4.31% CAGR to 2031, buoyed by capacity additions across China, India, and the ASEAN corridor. HSG Laser's USD 68.3 million Jinan campus exemplifies the scale, promising 10,000 high-power units per year and shortening lead times for local buyers. Policy push for EVs, aerospace, and shipbuilding funnels continuous orders, while domestic toolmakers extend overseas after-sales centers to support exports.

North America holds a robust installed base and benefits from fresh incentives that defray upgrade costs. The Department of Energy's USD 40 million grant pool in 2024 subsidized efficiency retrofits for 219 factories across 38 states, accelerating fiber laser adoption. In addition, the USD 750 million Advanced Energy Manufacturing and Recycling program earmarks funds for plant rehabs in coal-impacted regions, nudging metal shops toward cleaner, automated lines. Canada's automotive cluster and Mexico's near-shoring boom further lift regional demand.

Europe leverages precision-engineering heritage and regulatory heft to sustain sales, even amid slower macro growth. Bystronic's Intelligent Cutting Process autonomy kit, winner of the Swiss Technology Award, underscores R&D leadership in fully unattended lasers. Germany drives global standards through DIN committees, shaping ISO rules that favor high-spec safety architectures. EU environmental directives also spur investments in composite recycling plants, indirectly pulling orders for ultrasonics and water-jets. Secondary growth pockets appear in the Middle East, Africa, and South America, where infrastructure build-outs prompt first-time purchases of mid-range plasma and oxy-fuel machines.

- TRUMPF SE + Co. KG

- Lincoln Electric Holdings, Inc.

- ESAB Corp. (ex-Colfax)

- Bystronic AG

- Hypertherm Associates

- IPG Photonics Corp.

- Mitsubishi Electric / Mazak Optonics

- Han's Laser Technology

- Messer Cutting Systems

- Flow International

- OMAX Corp.

- KMT Waterjet Systems

- Amada Miyachi

- Kennametal Inc.

- DAIHEN Corp.

- Koike Aronson, Inc.

- GCE Group

- Linde plc (Cutting gases)

- Prima Power

- Struers (sample-prep niche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision-critical fabrication in EV/ICE automotive & aerospace

- 4.2.2 Industry 4.0 driven CNC/robotic automation surge

- 4.2.3 Manufacturing capacity boom across APAC

- 4.2.4 Post-pandemic cap-ex incentives for energy-efficient fiber lasers

- 4.2.5 Recycling of advanced composites requiring cold-cutting processes

- 4.2.6 Lightweight battery-housing demand in e-mobility platforms

- 4.3 Market Restraints

- 4.3.1 High upfront capital & integration costs

- 4.3.2 Global shortage of skilled CNC / CAM technicians

- 4.3.3 Supply-chain volatility for critical electronic & optical components

- 4.3.4 Garnet-abrasive scarcity disrupting water-jet OPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Global Manufacturing-Sector Snapshot

- 4.9 Metalworking Industry Snapshot

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Technology

- 5.1.1 Laser

- 5.1.1.1 Fiber

- 5.1.1.2 CO2

- 5.1.1.3 Solid-state / Other

- 5.1.2 Plasma

- 5.1.2.1 High-definition

- 5.1.2.2 Conventional

- 5.1.3 Water-Jet

- 5.1.3.1 Abrasive

- 5.1.3.2 Pure

- 5.1.4 Flame / Oxy-fuel

- 5.1.5 Ultrasonic & Emerging

- 5.1.1 Laser

- 5.2 By Automation Level

- 5.2.1 Manual

- 5.2.2 Semi-automated

- 5.2.3 Robotic / Fully-automated

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defense

- 5.3.3 Electrical & Electronics

- 5.3.4 Construction & Infrastructure

- 5.3.5 Metal-Fabrication Job Shops

- 5.3.6 Shipbuilding

- 5.3.7 Energy & Power

- 5.3.8 Others (Medical Devices, etc.)

- 5.4 By Material Type

- 5.4.1 Ferrous Metals

- 5.4.2 Non-Ferrous Metals

- 5.4.3 Composites

- 5.4.4 Glass/Ceramics/Stone

- 5.4.5 Others (Polymers/Plastics/Wood, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global overview, Core segments, Financials, Strategic info, Products, Recent developments)

- 6.4.1 TRUMPF SE + Co. KG

- 6.4.2 Lincoln Electric Holdings, Inc.

- 6.4.3 ESAB Corp. (ex-Colfax)

- 6.4.4 Bystronic AG

- 6.4.5 Hypertherm Associates

- 6.4.6 IPG Photonics Corp.

- 6.4.7 Mitsubishi Electric / Mazak Optonics

- 6.4.8 Han's Laser Technology

- 6.4.9 Messer Cutting Systems

- 6.4.10 Flow International

- 6.4.11 OMAX Corp.

- 6.4.12 KMT Waterjet Systems

- 6.4.13 Amada Miyachi

- 6.4.14 Kennametal Inc.

- 6.4.15 DAIHEN Corp.

- 6.4.16 Koike Aronson, Inc.

- 6.4.17 GCE Group

- 6.4.18 Linde plc (Cutting gases)

- 6.4.19 Prima Power

- 6.4.20 Struers (sample-prep niche)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment