PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940575

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940575

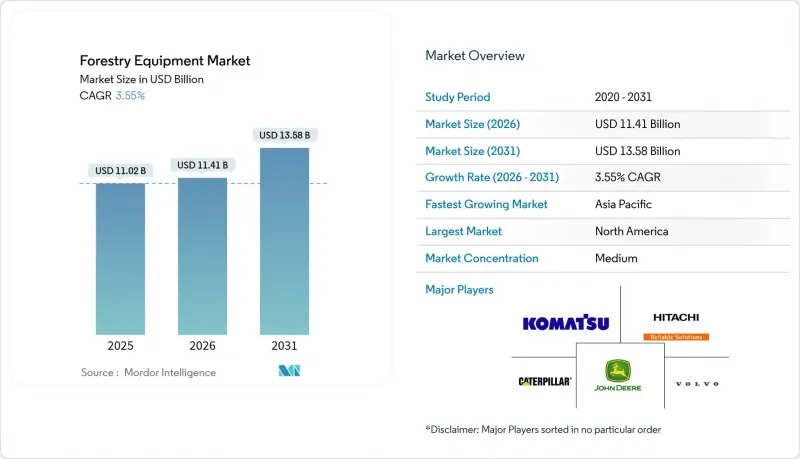

Forestry Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The forestry equipment market was valued at USD 11.02 billion in 2025 and estimated to grow from USD 11.41 billion in 2026 to reach USD 13.58 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031).

Demand centers on mechanized selective-logging machinery, precision forestry platforms, and post-wildfire salvage systems that raise productivity while adhering to stricter sustainability mandates. North American operators drive unit sales through fleet renewal programs, whereas Asia-Pacific buyers prioritize first-time mechanization coupled with government incentives for sustainable forestry. Electric and hybrid powertrains are moving from pilot tests to early commercial deployment as battery density improves in cold-weather conditions, though diesel remains indispensable for deep-forest tasks. Persistent shortages of skilled equipment operators, elevated financing costs, and timber-price volatility temper an otherwise steady outlook.

Global Forestry Equipment Market Trends and Insights

Rising Demand for Mechanised Selective Logging

Selective harvesting standards embedded in the 2024 U.S. National Forest Management Guidelines now cover 70% of federal timber sales, prompting rapid specification upgrades for harvester heads and control software. Manufacturers have responded with dual-boom designs that enable simultaneous felling and processing, allowing contractors to capture premium-grade stems with 25-30% higher per-acre revenues. Europe mirrors this pattern as private landowners monetize certified sustainable timber for premium export contracts. Training programs sponsored by equipment OEMs shorten learning curves, broadening the addressable contractor base. Regional logging cooperatives pool capital to acquire advanced feller-bunchers, enhancing utilization while easing financing hurdles.

Increasing Adoption of Electric and Hybrid Forestry Machinery

Battery-electric platforms transitioned from demonstration to early commercialization in 2025 after British Columbia's diesel-electric logging truck prototype cut fuel use by 40% without payload penalties. Cold-climate field trials in Finland and Sweden validated lithium-ion systems down to -20 °C, alleviating one of the biggest adoption barriers. Government climate funds offset up to 30% of purchase prices for zero-emission machines across the European Union, accelerating order books for forwarders, harvesters, and charging trailers. Hybrid drivetrains offer a practical bridge solution, delivering 15-25% fuel savings on skidders that work far from grid-tied chargers. Infrastructure build-outs along forest service roads remain the next bottleneck, spurring public-private partnerships to install fast chargers at log-sorting yards.

High Upfront Capital Expenditure for Advanced Machines

Modern harvesters retail between USD 800,000 and USD 1.2 million, triple the cost of conventional machines while offering incremental productivity gains in some operations. Elevated interest rates since 2024 magnify financing burdens, prompting smaller contractors to delay purchases or exit the business. Rental fleets bridge the gap with flexible pay-per-use terms, expanding at 4.27% CAGR as reported by multiple OEM finance arms. Leasing firms bundle maintenance, telematics, and operator training, lowering total cost of ownership but compressing dealer margins. Equipment makers introduce stripped-down "value" lines to broaden the sales funnel, though these models still depend on scale economies to remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Global Biomass and Bioenergy Projects

- Government Incentives for Precision and Sustainable Forestry

- Shortage of Skilled Heavy-Equipment Operators in Rural Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Felling equipment generated 36.12% of the forestry equipment market share in 2025, underscoring its central role in reducing manual chain-saw labor and mitigating safety risks. High-capacity harvesters equipped with GPS and selective-cutting algorithms now capture stems with centimeter-level precision, improving stand quality and log recovery rates. Chainsaws remain indispensable for specialty cuts and steep-slope terrain, but their volumes plateau as contractors switch to mechanized alternatives for core production.

Longevity gains in harvester heads, achieved through carbide-tipped saw bars and predictive maintenance analytics, extend component life cycles by up to 15%. Forward-integrated equipment suites combine feller-bunchers with on-board de-limbing, enabling single-operator workflows that increase productivity per shift. OEMs collaborate with software firms to overlay digital stand maps onto cab displays, guiding operators on which trees to remove for optimal residual growth. Other forestry equipment, while commanding a smaller revenue base, is forecast to grow at 4.18% CAGR through 2031 as contractors diversify into land clearing, biomass harvesting, and wildfire mitigation. Mulchers with interchangeable heads process underbrush for fuel-reduction projects, while purpose-built loaders serve biomass terminals that demand high cycle counts. Innovation in modular attachments-such as quick-coupler stump grinders-broadens machine versatility, lowering ownership costs and encouraging adoption even among smaller fleets. Integrated measurement sensors embedded in grapples record log diameter and moisture, feeding data directly into mill planning systems and raising downstream efficiency.

Diesel-powered platforms retained 61.78% of the forestry equipment market size in 2025 due to ubiquitous refueling infrastructure and unmatched torque for steep terrain hauling. Tier-4-F engines improved particulate performance, but operators still face stricter carbon accountability in export-oriented supply chains. Fuel-tracking telematics reveal 8-10% savings after driver-behavior coaching, allowing fleets to temper rising diesel expenses without swapping powertrains.

Electric-powered machinery marks the fastest-growing line at 4.32% CAGR through 2031 as battery chemistries deliver higher energy density with reduced cold-weather degradation. Mid-harvest fast-charging trailers fitted with solar-plus-diesel hybrid gensets enable partial recharging during scheduled maintenance windows, minimizing downtime. Early adopters report 25% lower operating costs where grid power is available at staging yards. Hybrid machines continue to bridge the gap, capturing regenerative energy on downhill skids and powering auxiliary hydraulics electrically. Petrol/oil units persist in handheld categories and remote fire-break operations where overall machine weights must remain minimal.

The Forestry Equipment Market Report is Segmented by Product Type (Felling Equipment, Extracting Equipment, and More), Power Source (Diesel-Powered, Petrol/Oil-Powered, and More), Application (Logging, Land Clearing, Forest Fire Management, and More), End-User (Commercial Logging Companies, Government Forestry Agencies, Rental Service Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.40% of 2025 revenue, anchored by extensive private timber holdings and mature mechanization practices. U.S. operators accelerated fleet modernization to comply with revised Selective Logging Standards, while Canadian contractors specified cold-weather packages that extend duty cycles in sub-zero regimes. Productivity analytics show utilization improvements of 10-12% across fleets that adopted AI-driven maintenance scheduling.

European demand remains steady as biomass expansion offsets plateauing sawlog volumes. Scandinavia leads precision-forestry adoption, integrating stand-level LiDAR data into machine control systems that raise recovery rates. Central European contractors invest in fuel-efficient hybrid skidders suited to mixed hardwood stands. Regulatory frameworks such as EU taxonomy classifications reinforce purchases of low-emission equipment, providing financing advantages to compliant buyers. Asia-Pacific is projected to log a 4.07% CAGR through 2031, driven by China's sustainable forestry program and Japan's ongoing post-disaster reconstruction commitments. Chinese provincial grants cover up to 40% of AI-enabled harvesters, spurring domestic OEMs to partner with global suppliers on control software. Australia's wildfire mitigation measures expand demand for brush-clearing mulchers and salvage harvesters. South America's plantation forestry growth boosts sales of high-throughput feller-bunchers, while reforestation commitments in Middle East and Africa begin moving from policy to procurement, opening new frontier markets for versatile multi-purpose machines.

- Deere & Company

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment AB

- Hitachi Construction Machinery Co. Ltd.

- Barko Hydraulics LLC

- HD Hyundai Infracore Co. Ltd.

- Kesla Oyj

- Ponsse Oyj

- Rottne Industri AB

- Eco Log Sweden AB

- AGCO Corporation

- Kubota Corporation

- Bell Equipment Limited

- Tigercat Industries Inc.

- CNH Industrial N.V.

- Husqvarna AB

- Doosan Bobcat Inc.

- SENNEBOGEN Maschinenfabrik GmbH

- Logset Oy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mechanised Selective Logging

- 4.2.2 Increasing Adoption of Electric and Hybrid Forestry Machinery

- 4.2.3 Expansion of global Biomass and Bioenergy Projects

- 4.2.4 Government Incentives for Precision and Sustainable Forestry

- 4.2.5 Integration of Telematics and AI-Enabled Fleet Optimisation

- 4.2.6 Increased Post-Wildfire Salvage Harvesting Needs

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Advanced Machines

- 4.3.2 Shortage of Skilled Heavy-Equipment Operators in Rural Areas

- 4.3.3 Limited Charging Infrastructure in Remote Forest Regions

- 4.3.4 Volatility of Global Timber Prices Impacting CAPEX Cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers/Consumers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors

- 4.10 Impact of COVID-19 on the Forestry Equipment Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Felling Equipment

- 5.1.1.1 Chainsaws

- 5.1.1.2 Harvesters

- 5.1.1.3 Feller Bunchers

- 5.1.2 Extracting Equipment

- 5.1.2.1 Forwarders

- 5.1.2.2 Skidders

- 5.1.2.3 Other Extracting Equipment

- 5.1.3 On-Site Processing Equipment

- 5.1.3.1 Chippers and Grinders

- 5.1.3.2 Delimbers and Slashers

- 5.1.3.3 Other On-Site Processing Equipment

- 5.1.4 Separately Sold Parts and Attachments

- 5.1.4.1 Saw Chain, Guide Bars, Discs, and Teeth

- 5.1.4.2 Harvesting and Other Cutting Heads

- 5.1.4.3 Other Separately Sold Parts and Attachments

- 5.1.5 Other Forestry Equipment

- 5.1.5.1 Loaders

- 5.1.5.2 Mulchers

- 5.1.5.3 Other Forestry Equipment

- 5.1.1 Felling Equipment

- 5.2 By Power Source

- 5.2.1 Diesel-Powered Equipment

- 5.2.2 Petrol / Oil-Powered Equipment

- 5.2.3 Electric-Powered Equipment

- 5.2.4 Hybrid-Powered Equipment

- 5.2.5 Other Power Source

- 5.3 By Application

- 5.3.1 Logging

- 5.3.2 Land Clearing

- 5.3.3 Forest Fire Management

- 5.3.4 Forest Road Construction

- 5.3.5 Biomass Harvesting

- 5.3.6 Other Application

- 5.4 By End-User

- 5.4.1 Commercial Logging Companies

- 5.4.2 Timberland Investment Managers

- 5.4.3 Government Forestry Agencies

- 5.4.4 Individual Contractors and Small Operators

- 5.4.5 Rental Service Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Caterpillar Inc.

- 6.4.3 Komatsu Ltd.

- 6.4.4 Volvo Construction Equipment AB

- 6.4.5 Hitachi Construction Machinery Co. Ltd.

- 6.4.6 Barko Hydraulics LLC

- 6.4.7 HD Hyundai Infracore Co. Ltd.

- 6.4.8 Kesla Oyj

- 6.4.9 Ponsse Oyj

- 6.4.10 Rottne Industri AB

- 6.4.11 Eco Log Sweden AB

- 6.4.12 AGCO Corporation

- 6.4.13 Kubota Corporation

- 6.4.14 Bell Equipment Limited

- 6.4.15 Tigercat Industries Inc.

- 6.4.16 CNH Industrial N.V.

- 6.4.17 Husqvarna AB

- 6.4.18 Doosan Bobcat Inc.

- 6.4.19 SENNEBOGEN Maschinenfabrik GmbH

- 6.4.20 Logset Oy

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment