PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940611

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940611

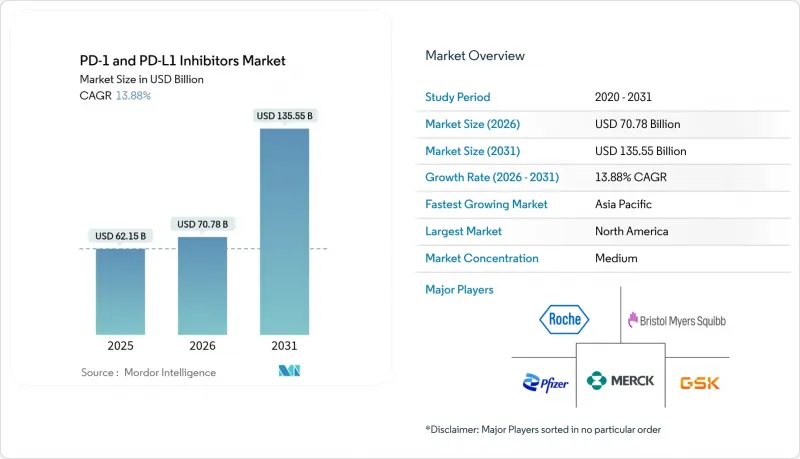

PD-1 And PD-L1 Inhibitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

PD-1 & PD-L1 inhibitors market size in 2026 is estimated at USD 70.78 billion, growing from 2025 value of USD 62.15 billion with 2031 projections showing USD 135.55 billion, growing at 13.88% CAGR over 2026-2031.

Growth rests on rapid regulatory approvals, unrelenting label-expansion spending and the arrival of bispecific constructs that extend immune-checkpoint utility across tumor types. The December 2024 FDA clearance of subcutaneous nivolumab validated novel delivery formats that can protect revenue streams after patent expiry. Combination strategies-particularly PD-1/VEGF and PD-1/CTLA-4 pairings-continue to post meaningful progression-free-survival gains, reinforcing prescriber confidence and underpinning premium pricing. Large payor systems in the United States and Europe still absorb high acquisition costs, yet China's volume-based procurement model exerts downward pricing pressure and forces multinationals to re-examine launch tactics in emerging economies. Digital pharmacies, tele-oncology channels and small-molecule oral entrants broaden patient access and reshape traditional infusion-center economics, creating additional growth vectors for the PD-1 & PD-L1 inhibitors market.

Global PD-1 And PD-L1 Inhibitors Market Trends and Insights

Explosive R&D spend on new-label expansion for blockbuster assets

Drug makers funnel record capital into post-marketing studies aimed at unlocking fresh indications for approved PD-1/PD-L1 agents. Merck alone sponsors more than 1,600 active trials with pembrolizumab, allowing the molecule to secure additional patient cohorts while maintaining favorable reimbursement status. FDA clearance in June 2024 for first-line therapy in primary advanced endometrial carcinoma lifted median progression-free survival from 6.5 to 11.1 months, reinforcing clinical value and elongating product lifecycles. European authorities echoed this momentum with a positive opinion for malignant pleural mesothelioma in November 2024, showing how global regulators lean on existing safety dossiers to shorten review times. Continuous label expansion defers biosimilar substitution, sustains premium pricing and amplifies the growth trajectory of the PD-1 & PD-L1 inhibitors market.

Faster U.S. FDA & NMPA real-time oncology reviews

Regulators now grant rolling submissions, surrogate-endpoint acceptances and real-time advisory meetings that compress development timelines. The December 2024 FDA nod for subcutaneous nivolumab moved from filing to approval inside ten months, underscoring rising agency agility. China's NMPA matched that speed by clearing 48 first-in-class cancer drugs during 2024, with checkpoint inhibitors representing the largest single therapeutic category. Conditional approvals awarded to ivonescimab after superior phase 3 data in non-small cell lung cancer underscore how priority review incentives reset competitive clocks. Accelerated cycles shorten payback windows, improve risk-adjusted net present value and strengthen capital inflows into the PD-1 & PD-L1 inhibitors market.

Escalating CAPEX in pivotal phase-III combination studies

Adaptive multi-arm trials demand expanded cohorts, extended follow-up and complex biomarker panels, driving per-patient outlays as high as USD 61,907. Sponsors running more than 100 concurrent pembrolizumab studies face cumulative budgets that challenge even blue-chip cash flows. Smaller biotech players encounter financing headwinds, slowing pipeline diversity. These economics shave 1.4 percentage points from forecast CAGR yet do not reverse overall market momentum.

Other drivers and restraints analyzed in the detailed report include:

- China's volume-based procurement favouring domestic PD-(L)1 makers

- Rise of bispecific / tri-specific antibodies entering late-phase trials

- Pending 2028 U.S. patent cliffs for Keytruda & Opdivo

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PD-1 inhibitors held 80.92% of 2025 revenue, equivalent to a USD 50.29 billion PD-1 & PD-L1 inhibitors market size. Their dominance stems from robust survival data across melanoma, lung, bladder and head-and-neck cancers. Comprehensive safety experience, guideline entrenchment and clinician familiarity reinforce prescribing inertia across oncology centers. Heavy trial investment secures ongoing first-line positioning and sustains double-digit expansion through new tumor types.

Growth momentum shifts toward PD-L1 molecules as developers exploit oral, heterodimeric and polymer-mimetic engineering. In vitro studies show iBodies maintain PD-L1 blockade potency while enhancing thermostability, foreshadowing lower cold-chain costs. ABSK043 and follow-on oral assets may shorten chair time, increase patient convenience and open distribution through retail and online pharmacies. These advantages underpin the 19.85% forecast CAGR for PD-L1 agents, gradually narrowing but not overturning PD-1 supremacy within the PD-1 & PD-L1 inhibitors market.

The PD-1 and PD-L1 Inhibitors Market Report is Segmented by Type of Inhibitors (PD-1 Inhibitors and PD-L1 Inhibitors), Application (Hodgkins Lymphoma, Kidney Cancer, Melanoma, Non-Small Cell Lung Cancer, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 46.90% of worldwide revenue in 2025 on the back of rapid innovation uptake, broad private insurance coverage and the FDA's global benchmarking role. Breakthrough designations for novel combinations such as petosemtamab plus pembrolizumab accelerate time to clinic and keep therapy standards shifting upward. Legislative shifts including Inflation Reduction Act price negotiations starting 2026 bring uncertainty to out-year margins but are unlikely to dampen near-term adoption given high unmet oncologic need.

Europe follows with mature yet price-sensitive dynamics. The EMA's joint-clinical-assessment rules effective 2025 harmonize evidence criteria, promising quicker cross-border availability although HTA agencies still scrutinize cost efficiency. Commercial access agreements for pembrolizumab in adjuvant NSCLC illustrate how manufacturers adapt discount schemes to satisfy NICE thresholds. Recent EMA approvals for Chinese-origin toripalimab and tislelizumab add competitive spice and demonstrate willingness to diversify the regional checkpoint arsenal.

Asia-Pacific is the fastest-growing contributor at 15.83% CAGR. China spearheads volume through NMPA reforms that cleared 228 new drugs in 2024, many involving PD-1/PD-L1 pathways. Domestic champions leverage price concessions to cement large-scale tenders and then springboard into ASEAN markets. Japan sustains stable growth as aging demographics drive cancer incidence, while Australia funds early adoption via national health insurance. Collectively, the region delivers both volume expansion and innovative pipeline contributions, reinforcing global momentum of the PD-1 & PD-L1 inhibitors market.

- Merck

- Bristol-Myers Squibb

- Roche

- AstraZeneca

- Sanofi

- Pfizer

- Regeneron Pharma Inc.

- GlaxoSmithKline

- Amgen

- Eli Lilly and Company

- Novartis

- BeiGene Ltd.

- Innovent Biologics

- Hengrui Medicine

- Akeso Inc.

- Henlius Biotech

- Seagen

- Shanghai Junshi Biosciences

- Arcus Biosciences

- Leap Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive R&D Spend On New-Label Expansion For Blockbuster Assets

- 4.2.2 Faster U.S. FDA & NMPA Real-Time Oncology Reviews

- 4.2.3 China's Volume-Based Procurement Favouring Domestic PD-(L)1 Makers

- 4.2.4 Rise Of Bispecific / Tri-Specific Antibodies Entering Late-Phase Trials

- 4.2.5 AI-Enabled Biomarker Discovery Improving Responder Rates

- 4.2.6 Point-Of-Care Companion-Diagnostic Advances Lowering Trial Attrition

- 4.3 Market Restraints

- 4.3.1 Escalating CAPEX In Pivotal Phase-III Combination Studies

- 4.3.2 Pending 2028 U.S. Patent Cliffs For Keytruda & Opdivo

- 4.3.3 Uneven Global Reimbursement; HTA Push-Back On Cost-To-Benefit

- 4.3.4 Emergent Small-Molecule PD-(L)1 Oral Entrants Cannibalising Mab Share

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Inhibitors

- 5.1.1 PD-1 Inhibitors

- 5.1.2 PD-L1 Inhibitors

- 5.2 By Application

- 5.2.1 Non-Small Cell Lung Cancer

- 5.2.2 Melanoma

- 5.2.3 Kidney Cancer

- 5.2.4 Hodgkin Lymphoma

- 5.2.5 Other Cancers

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Merck & Co.

- 6.3.2 Bristol-Myers Squibb

- 6.3.3 F. Hoffmann-La Roche AG

- 6.3.4 AstraZeneca PLC

- 6.3.5 Sanofi SA

- 6.3.6 Pfizer Inc.

- 6.3.7 Regeneron Pharma Inc.

- 6.3.8 GSK plc

- 6.3.9 Amgen Inc.

- 6.3.10 Eli Lilly and Co.

- 6.3.11 Novartis AG

- 6.3.12 BeiGene Ltd.

- 6.3.13 Innovent Biologics

- 6.3.14 Hengrui Medicine

- 6.3.15 Akeso Inc.

- 6.3.16 Henlius Biotech

- 6.3.17 Seagen Inc.

- 6.3.18 Shanghai Junshi Biosciences

- 6.3.19 Arcus Biosciences

- 6.3.20 Leap Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment