PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940618

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940618

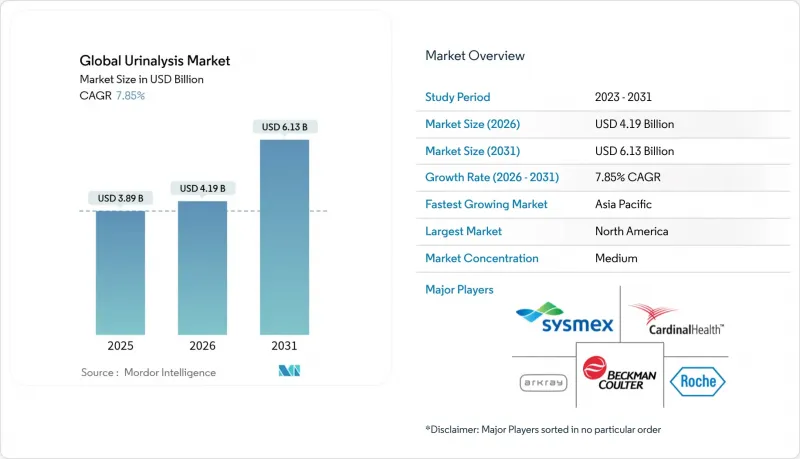

Global Urinalysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The urinalysis market is expected to grow from USD 3.89 billion in 2025 to USD 4.19 billion in 2026 and is forecast to reach USD 6.13 billion by 2031 at 7.85% CAGR over 2026-2031.

Rising chronic kidney and metabolic disease prevalence, point-of-care (POC) adoption, and AI-enabled automation collectively propel demand. Suppliers are layering Internet-of-Medical-Things (IoMT) connectivity onto mid- and high-throughput analyzers, allowing laboratories and clinicians to consolidate test data and speed clinical decisions. Home-based tele-diagnostic kits are also broadening access, while North American reimbursement stability underpins steady instrument placements. Asia-Pacific, meanwhile, benefits from government-funded diagnostic capacity expansion and growing disposable incomes.

Global Urinalysis Market Trends and Insights

Growing burden of chronic kidney & metabolic diseases

Chronic kidney disease (CKD) and diabetes drive sustained demand for routine testing, with kidney monitoring applications rising at a 10.24% CAGR to 2030. An estimated 537 million adults lived with diabetes in 2024, heightening the need for microalbumin and creatinine ratio checks that detect early nephropathy.Advanced biomarkers such as neutrophil gelatinase-associated lipocalin broaden the clinical utility of urinalysis, while AI-based risk-stratification models help clinicians tailor therapy and reduce hospital readmissions. Health systems spend more than USD 120 billion annually on CKD management in the United States, reinforcing preventive screening budgets. These patterns strengthen both recurrent consumable revenue and adoption of POC devices that fit chronic-care pathways.

Rising preference for point-of-care urinalysis

Emergency departments and urgent-care clinics increasingly rely on immediate dipstick or cartridge results to triage patients, shortening wait times and improving throughput. COVID-19 catalyzed telemedicine, and manufacturers responded with portable analyzers that transmit secure data to electronic health records. Siemens Healthineers added optical identification bands to its MULTISTIX strips, automating quality checks and reducing manual errors. Rural providers benefit most, as decentralized platforms fill gaps where central labs are distant. Value-based reimbursement further motivates providers to convert routine screens from laboratory-centric to bedside workflows, lifting the urinalysis market toward double-digit POC growth.

Stringent & heterogeneous regulatory frameworks

The 2024 FDA Laboratory Developed Tests rule mandates staged pre-market review and quality-system compliance, adding up to USD 3.56 billion in cumulative costs for diagnostics producers.China's updated Medical Device Regulation and India's marketing code similarly tighten oversight, compelling companies to budget for multi-jurisdiction submissions and audits. Harmonization with ISO 13485 by 2026 will improve global alignment yet raises near-term operating expense. Smaller firms may delay launches, trimming competitive intensity but also slowing innovation cadence within the urinalysis market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing incidence of urinary tract infections

- Technology leap: AI-enabled automated analyzers

- Shortage of trained laboratory personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables held 65.62% of the urinalysis market in 2025, anchored by high-volume reagent strip sales that create annuity-like revenue for suppliers. The instruments category, although smaller, is set for a 8.76% CAGR to 2031 as laboratories automate to counter workforce shortages and to align with stricter quality mandates. Roche's cobas u 601, for instance, processes 240 samples an hour while locking customers into proprietary strip technology, illustrating the razor-and-blade dynamic that tethers consumable pull-through to analyzer placements. Several mid-tier hospitals, deterred by upfront costs, favor semi-automated units that still reduce manual error without full capital investment.

Consumables continue to underpin supplier profitability because each patient sample requires new strips, controls, and cups, generating repeat orders that buffer cyclical instrument demand. The urinalysis market size for consumables is forecast to expand in line with rising diabetes screens and UTI prevalence, whereas instrument revenue grows faster from a smaller baseline. Bundled service agreements, including remote IoMT monitoring of analyzer performance, cement vendor-client relationships and sustain market visibility.

Biochemical assays accounted for 45.10% of total revenue in 2025 and are projected to climb 9.21% annually through 2031. They remain indispensable for glucose, protein, and ketone measurement in metabolic and renal assessments, ensuring recurrent strip usage per encounter. Mass-spectrometry-based proteomic extensions now detect thousands of urinary proteins, promising earlier disease signatures and personalized therapeutic monitoring.

Flow cytometry, although representing a smaller slice of the urinalysis market size today, is the fastest-growing modality due to its ability to automate cell counting and morphological classification. Laboratories facing microscopy bottlenecks choose flow systems to raise throughput and standardize reporting. Moreover, smartphone-based colorimetric readers fuse biochemical simplicity with digital analytics, broadening access in resource-constrained settings. The dual push from advanced lab platforms and consumer-grade readers multiplies test volumes and enriches data granularity.

The Urinalysis Market is Segmented by Product Type (Instruments [Automated Analyzer, and More], Consumables [Reagents & Kits, and More]), by Test Type (Biochemical, Sediment, and More), by Application (Disease Screening, Kidney Disease Monitoring, and More), by End User (Hospitals, Clinical Laboratories, and More), by Technology (Dipstick, Microscopy, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America held 38.85% of 2025 revenue and benefits from comprehensive insurance coverage, including a USD 8.57 specimen collection fee under Medicare's 2025 schedule. Hospitals deploy POC units in emergency departments to alleviate crowding, while Canada's single-payer framework favors cost-effective analyzers with low consumable burn rates. Mexico's middle-income growth and public-sector spending on diagnostics lift baseline test demand, particularly in peri-urban clinics. Data-privacy legislation such as HIPAA and the 2024 Cybersecurity Modernization Act emphasize secure analyzer connectivity, influencing procurement toward major brands with robust encryption.

Asia-Pacific is the fastest-growing region, posting an 10.72% CAGR to 2031. China funds large-scale diagnostic modernization, from county hospital upgrades to innovative concepts such as smart public toilets that analyze urine on site for a 20-yuan fee, expanding surveillance reach. Japan's senior population relies on home testing to manage chronic illnesses, while India's Make-in-India program stimulates local analyzer assembly that lowers cost of ownership. Southeast Asia leverages ASEAN harmonization to streamline approvals, prompting multinational suppliers to set up regional service hubs.

Europe maintains steady expansion as aging demographics raise chronic disease screening volumes. CE-marking alignment and EUDAMED database rollout simplify market entry for new analyzers. Germany and the United Kingdom pilot AI-assisted sediment imaging in public hospitals, while France reimburses home test kits under tele-consult rules. The Middle East invests oil revenues in tertiary-care centers stocked with high-throughput instruments, and South Africa anchors sub-Saharan distribution due to its relative regulatory clarity. South America offers moderate growth, led by Brazil's public-private diagnostic partnerships that extend urinalysis access beyond urban cores.

- Abbott Laboratories

- Acon Laboratories

- Arkray

- Beckton Dickinson

- Beckton Dickinson

- Bio-Rad Laboratories

- Cardinal Health

- Roche

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

- QuidelOrtho

- Mindray

- URIT Medical Electronic Co. Ltd.

- Randox Laboratories

- DiaSys Diagnostic Systems

- Clarity Diagnostics (Jant Pharmacal)

- Dirui Industrial Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing burden of chronic kidney & metabolic diseases

- 4.2.2 Rising preference for point-of-care (POC) urinalysis

- 4.2.3 Increasing incidence of urinary tract infections (UTIs)

- 4.2.4 Technology leap: AI-enabled automated analyzers

- 4.2.5 Integration with home-based tele-diagnostics kits

- 4.2.6 Adoption in personalized drug-monitoring programs

- 4.3 Market Restraints

- 4.3.1 Stringent & heterogeneous regulatory frameworks

- 4.3.2 Shortage of trained laboratory personnel

- 4.3.3 Reimbursement variability across major markets

- 4.3.4 Cyber-security risks in connected analyzers (IoMT)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.1.1 Automated Analyzer

- 5.1.1.2 Semi-automated Analyzer

- 5.1.1.3 Point-of-Care Analyzer

- 5.1.2 Consumables

- 5.1.2.1 Reagents & Kits

- 5.1.2.2 Dipsticks

- 5.1.2.3 Disposables

- 5.1.1 Instruments

- 5.2 By Test Type

- 5.2.1 Biochemical

- 5.2.2 Sediment

- 5.2.3 Pregnancy & Fertility

- 5.3 By Application

- 5.3.1 Disease Screening

- 5.3.2 Kidney Disease Monitoring

- 5.3.3 Pregnancy & Fertility

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinical Laboratories

- 5.4.3 Point-of-Care Settings

- 5.4.4 Home Healthcare

- 5.4.5 Others

- 5.5 By Technology

- 5.5.1 Dipstick

- 5.5.2 Microscopy

- 5.5.3 Flow Cytometry

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 ACON Laboratories Inc.

- 6.3.3 Arkray Inc.

- 6.3.4 Beckman Coulter Inc.

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 Bio-Rad Laboratories Inc.

- 6.3.7 Cardinal Health Inc.

- 6.3.8 Roche Diagnostics

- 6.3.9 Siemens Healthineers

- 6.3.10 Sysmex Corporation

- 6.3.11 Thermo Fisher Scientific Inc.

- 6.3.12 QuidelOrtho Corporation

- 6.3.13 Mindray Medical International Ltd.

- 6.3.14 URIT Medical Electronic Co. Ltd.

- 6.3.15 Randox Laboratories Ltd.

- 6.3.16 DiaSys Diagnostic Systems GmbH

- 6.3.17 Clarity Diagnostics (Jant Pharmacal)

- 6.3.18 Dirui Industrial Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment