PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940620

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940620

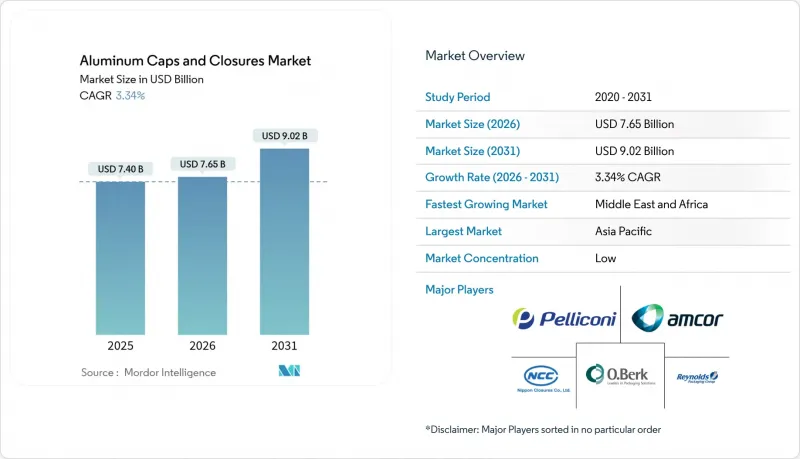

Aluminum Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The aluminium caps and closures market is expected to grow from USD 7.40 billion in 2025 to USD 7.65 billion in 2026 and is forecast to reach USD 9.02 billion by 2031 at 3.34% CAGR over 2026-2031.

Demand growth is paced, not explosive, because penetration in core beverage segments is mature; however, upgrades in premium spirits, biologics packaging, and EU sustainability rules continue to open profitable niches. Mandatory tethered-cap regulations in Europe, recycled-aluminium incentives in China, and a shift toward premium ready-to-drink offerings in North America are prompting brand owners to redesign closures with higher functional and aesthetic value. Volatility in London Metal Exchange (LME) pricing tightens converter margins, yet the push for infinitely recyclable materials still tilts preference toward aluminium over cork, steel, or plastic. Regional cost advantages particularly additional recycled capacity in Asia-Pacific are helping offset raw-material swings while keeping premium segments insulated from low-cost PET alternatives.

Global Aluminum Caps And Closures Market Trends and Insights

Rise of Premium RTD-Cocktail Aluminium Bottling in North America

Premium ready-to-drink cocktail brands introduced aluminium bottles throughout 2024 to signal upscale positioning while retaining recyclability. Several brands recorded 40-60% price premiums versus conventional cans, indicating consumers value tactile rigidity and re-close functionality. The barrier performance of aluminium protects botanical extracts from UV light and oxygen, supporting shelf life for spirit-based formulations. Brand collaborations with environmental non-profits reinforce sustainable credentials, creating a marketing halo that smaller steel or PET formats cannot match. The phenomenon is spilling into European travel-retail channels where single-serve spirits require tamper-evident yet elegant closures.

Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

Since July 2024, EU beverage bottles must feature tethered closures, sparking redesign activity across carbonated soft drink and water segments.Early consumer pushback against plastic tethered systems led premium water and juice brands to adopt aluminium screw-top variants with integrated hinge mechanisms. Because aluminium is infinitely recyclable and easily detached in material-recovery facilities, brand owners meet both tethered-cap rules and forthcoming 90% metal-collection targets. Multinationals are harmonizing pack formats across non-EU markets to avoid line-change complexity, magnifying near-term demand for value-added aluminium closures.

Volatile LME Aluminium Prices Compressing Converter Margins

Aluminium ingot reached USD 2,662 per ton in February 2025, swinging more than 15% within six months and squeezing converters that sell on long-term fixed contracts. Smaller closure firms without hedging programs face eroded margins, making them attractive acquisition targets for multinationals with advanced risk-management desks. Russian export uncertainty, elevated European smelting power costs, and new US container duties all amplify volatility. To stabilize supply, leading converters raise recycled content and explore alloy recipes with higher scrap tolerance, an approach aligned with carbon-reduction pledges yet requiring capital spend on upgraded annealing furnaces.

Other drivers and restraints analyzed in the detailed report include:

- Beverage-Grade Recycled Aluminium Capacity Expansions in China

- Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Screw caps retained dominance with 50.74% share in 2025 as they span beverages, condiments, and pharmaceuticals. That share equals USD 3.75 billion of the aluminium caps and closures market size in 2025, reflecting their proven sealing reliability. Easy-open ends, while smaller, are gaining fastest at a 6.38% CAGR through 2031 as consumers gravitate toward convenience features in canned coffee and ready meals. Continuous-thread ROPP variants secure traction in craft spirits because they reconcile tamper evidence with luxury visual cues. Crown corks hold relevance in traditional beer packaging, yet their growth is modest given the migration toward full-body slim cans. Lug, press-twist, and specialized flip-off designs serve tamper-sensitive food and pharma uses, illustrating the segmentation's shift from generalist to application-specific solutions.

Investment is flowing into die-cutting and scoring technologies that create safer, finger-friendly easy-open tabs, unlocking new mass channels like senior-nutrition beverages. Closure makers are also integrating laser-etched QR codes for trace-and-trace compliance without compromising decoration space. These embellishments carry higher unit economics, cushioning margins when raw-material costs rise. In contrast, standard screw-cap formats face commoditization, pressing manufacturers to differentiate through liner chemistry improvements that extend shelf life in aggressive-pH drinks.

Beverages commanded 46.02% share in 2025, equivalent to USD 3.41 billion of the aluminium caps and closures market. The segment covers still water, carbonated drinks, beer, wine, and premium spirits, each with nuanced closure needs. Premium alcohol producers elevate aluminium as a branding canvas, whereas carbonated soft-drink fillers chase lowest cost compliance to EU tethering. Pharmaceutical demand is expanding at a 6.76% CAGR, adding USD 284 million incremental value by 2031. Growth rests on biologic drug launches that specify flip-off tear-down seals to ensure sterile integrity. Food applications remain steady, propelled by gourmet oils and sauces pursuing metal lug caps for smooth pour control. Personal-care brands leverage aluminium's recyclability story to displace mixed-material lids, evidenced by high-profile deodorant launches in recyclable aluminium aerosols.

Cross-sector learning accelerates innovation: beverage can suppliers partner with personal-care companies to adapt internal varnishes for lotion compatibility, broadening addressable markets. Industrial chemical closures, though niche, benefit from aluminium's corrosion resistance when combined with specialty liners. The versatility across end-uses supports balanced portfolio exposure, hedging against cyclical dips in any one sector.

Aluminum Caps and Closures Market is Segmented by Cap Type (Screw Caps, Crown Cork, Lugs/Press Twist, and More), Application (Beverages, Food, Pharmaceutical, Cosmetics and Personal Care, and More), Neck Finish Diameter ( Less Than and Equal To 20mm, 21-30mm, and More), Distribution Channel (Direct Sales Channels, and Indirect Sales Channels) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 40.20% of global revenue in 2025, driven by China's prolific beverage output and India's packaged-goods expansion. Cost competitiveness improved after November 2024 when China abolished tariffs on imported recycled aluminium, enabling mills to supply coil at discounts versus primary metal. Japan and South Korea added a layer of technological sophistication, exporting closure presses and vision-inspection systems regionally. Southeast Asian demand benefitted from urbanization and Western quick-service restaurant chains insisting on tamper-proof lids, stimulating local cap conversion lines. India's standards upgrade mandating QR traceability for edible-oil packs nudged value share toward premium lug caps, attracting foreign joint ventures.

The Middle East and Africa represent the fastest-growing territory, forecast at 6.89% CAGR through 2031. Beverage investments in Nigeria and Kenya, plus desalinated bottled-water capacity in the Gulf, underpin volume. However, limited circular-economy infrastructure tempers aluminium caps and closures market penetration. Egypt's move to establish a dedicated food-grade recycling mill marks progress, yet widespread adoption awaits proof of economically viable collection streams. South Africa's established aluminium smelter base and port connectivity create export opportunities into landlocked neighbors.

Europe, though mature, remains pivotal because regulation steers global specifications. The July 2024 tethered-cap deadline forced fillers to redesign PET and aluminium containers simultaneously, generating engineering consulting revenue for closure specialists. Germany's mechanical-engineering cluster pioneered continuous-thread screw-top machines capable of 600 cpm with integrated torque monitoring, raising performance benchmarks. Italy's design houses customized embossing and color-shift inks for premium spirits, preserving perceived luxury even as closures migrate from cork to aluminium for sustainability reasons.

North America's market rides consumer migration to craft beverages and ready-to-drink cocktails packaged in resealable aluminium bottles. US tariff barriers imposed in April 2025 boosted domestic can-stock production, indirectly supporting closure coil producers by tightening local supply and encouraging reshoring. Mexico, a major beer exporter, toggles between aluminium and steel closure options to balance cost and supply risk, yet aluminium retains a foothold in premium bottle lines destined for European customers. South America, led by Brazil, invests in new beverage can lines that include in-house closure modules, shortening lead times.

- Amcor plc

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Guala Closures S.p.A

- Tecnocap Group

- Pelliconi and C. SpA

- Nippon Closures Co. Ltd

- Closure Systems International (CSI)

- Berlin Packaging LLC

- Bericap GmbH

- AptarGroup Inc.

- SKS Bottle and Packaging Inc.

- Hicap Closures Co. Ltd

- Federfin Tech SRL

- Rauh GmbH & Co.

- O.Berk Company

- The Cary Company

- Alutop SAS

- Shandong Lipeng Co. Ltd

- Idea Cap SRL

- Easy Open Lid Industry Corp. (Yiwu)

- RPC Group (PET Power)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of Premium RTD-Cocktail Aluminium Bottling in North America

- 4.2.2 Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

- 4.2.3 Beverage-Grade Recycled Aluminium Capacity Expansions in China

- 4.2.4 Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

- 4.2.5 Craft Spirits Migration from Cork to Aluminium ROPP in Europe

- 4.2.6 E-commerce Leakage-Testing Protocols Driving Lug Cap Adoption in India

- 4.3 Market Restraints

- 4.3.1 Volatile LME Aluminium Prices Compressing Converter Margins

- 4.3.2 Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

- 4.3.3 Tin-Free Steel Crown Cork Substitution in Mexican Beer

- 4.3.4 Limited Food-Grade Recycling Streams in Middle East

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cap Type

- 5.1.1 Screw Caps

- 5.1.2 Crown Cork

- 5.1.3 Lug / Press-Twist

- 5.1.4 Easy-Open End

- 5.1.5 Roll-On Pilfer Proof (ROPP)

- 5.1.6 Others (Flip-Off, Tear-Down)

- 5.2 By Application

- 5.2.1 Beverages

- 5.2.1.1 Alcoholic Beverages

- 5.2.1.2 Non-Alcoholic Beverages

- 5.2.2 Food

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Industrial and Household Chemicals

- 5.2.1 Beverages

- 5.3 By Neck Finish Diameter

- 5.3.1 Less than and Equal to 20 mm

- 5.3.2 21-30 mm

- 5.3.3 31-40 mm

- 5.3.4 More than 40 mm

- 5.4 By Distribution Channels

- 5.4.1 Direct Sales Channels

- 5.4.2 Indirect Sales Channels

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 Italy

- 5.5.2.4 United Kingdom

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor plc

- 6.4.2 Crown Holdings Inc.

- 6.4.3 Silgan Holdings Inc.

- 6.4.4 Guala Closures S.p.A

- 6.4.5 Tecnocap Group

- 6.4.6 Pelliconi and C. SpA

- 6.4.7 Nippon Closures Co. Ltd

- 6.4.8 Closure Systems International (CSI)

- 6.4.9 Berlin Packaging LLC

- 6.4.10 Bericap GmbH

- 6.4.11 AptarGroup Inc.

- 6.4.12 SKS Bottle and Packaging Inc.

- 6.4.13 Hicap Closures Co. Ltd

- 6.4.14 Federfin Tech SRL

- 6.4.15 Rauh GmbH & Co.

- 6.4.16 O.Berk Company

- 6.4.17 The Cary Company

- 6.4.18 Alutop SAS

- 6.4.19 Shandong Lipeng Co. Ltd

- 6.4.20 Idea Cap SRL

- 6.4.21 Easy Open Lid Industry Corp. (Yiwu)

- 6.4.22 RPC Group (PET Power)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment