PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940622

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940622

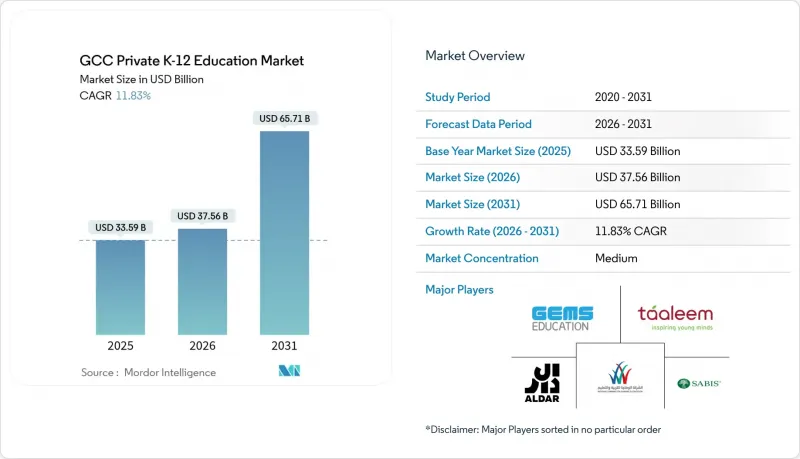

GCC Private K-12 Education - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The GCC Private K-12 Education Market was valued at USD 33.59 billion in 2025 and estimated to grow from USD 37.56 billion in 2026 to reach USD 65.71 billion by 2031, at a CAGR of 11.83% during the forecast period (2026-2031).

Sovereign-wealth expenditures exceeding USD 14.5 billion, alongside substantial government allocations prioritizing Saudi Arabia's public education sector, are driving robust double-digit growth. Additionally, the region-wide EdTech pipeline, projected to expand through 2028, further reinforces this upward trajectory . Expatriate inflows sustain demand; Dubai's 387,441 private-school students across 227 private schools represent a 6% annual enrolment rise, while Qatar now funds almost half of national students through vouchers that redirect public expenditure to private operators. Tuition premiumization accelerates as tier-1 campuses integrate AI teaching assistants, VR science suites, and university pathway programs that justify annual fees topping AED 200,000 (USD 54,400) .

GCC Private K-12 Education Market Trends and Insights

Government Reforms & Record-High Education Budgets

The Madaris marketplace in Saudi Arabia has significantly contributed to the expansion of private-school projects, driving an 86% year-on-year increase in newly issued education-investment licenses. This development highlights the strategic importance of education as a key component of the nation's infrastructure. Vision 2030 incorporates AI-focused curricula across all educational levels and allocates funding to academies for gifted students, thereby strengthening the framework for curricular advancements. The UAE matches ambition through its Education 33 agenda, which authorizes 100 new private schools and enlarges the education sector. Qatar channels its National Vision 2030 into eight PPP schools each year, preserving subsidy flows while outsourcing delivery risk to seasoned operators. Shared quality codes, such as UAE Federal Decree-Law 18/2020, ensure that fast growth does not dilute academic outcomes, drawing international capital into the GCC private K-12 education market.

Rapid Expatriate Inflow Boosting International-Curriculum Demand

Dubai's private-school community grew 6% in AY 2024-25 to 387,441 students across 227 private schools and now hosts international-school learners across the UAE. Qatar's 334 private schools teach 72% of expatriate children, turning curriculum diversification into a strategic imperative. South-Asian inflows lift CBSE enrolment while French nationals push Lycee models, and IB uptake rises as globally mobile families seek university portability, collectively widening the GCC private K-12 education market. Liberalized long-term visas convert transient workers into permanent education consumers who commit to multi-year fee cycles, stabilizing demand even during macro shocks. Established international chains that hold multiple accreditations gain a moat because new entrants need several years to secure the same certifications, reinforcing consolidation in the GCC private K-12 education market.

Chronic Shortage of Qualified Teachers

UAE schools have announced 900 job vacancies for the 2025 academic year and forecast an increased demand for teachers by 2030. However, visa limitations and intensified global competition are constraining the talent pool . KHDA stipulates bachelor's degrees, safeguarding certificates, and English-proficiency scores, eliminating quick-hire routes and driving wage inflation that compresses mid-market margins in the GCC private K-12 education market. Saudi AI-curriculum rollouts intensify demand for STEM specialists, fostering consortium recruitment initiatives in the UK and Australia that raise acquisition costs. Operators respond by founding in-house teacher academies, tying career progression to retention, and leveraging AI grading tools to cut administrative load, but execution lag could still trim near-term capacity expansion across the GCC private K-12 education market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Disposable Incomes Enabling Premium Tuition Fees

- EdTech Adoption Elevating Learning Outcomes

- Escalating Land & Construction Costs for Campuses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kindergarten captured 12.14% CAGR through 2031, outpacing every other tier, even though primary holds the largest 44.25% revenue share within the GCC Private K-12 Education market. The UAE's early-childhood enrolment experienced significant growth following the attainment of 99.2% access to organized education for four-year-olds. Similarly, Saudi Arabia's enrolment expansion was driven by subsidies introduced under the Vision 2030 framework. Operators monetize preschool demand by offering wrap-around care, bilingual immersion, and AI-enabled phonics modules that raise parent stickiness. Because brand loyalty takes shape before age six, a healthy kindergarten pipeline stabilizes lifetime revenue and positions operators to cross-sell primary and secondary seats, anchoring cash-flow visibility in the GCC private K-12 education market.

Primary maintains the top spot because enrolment bulges begin at Grade 1, and decisions made here often lock students for 12 years. International curricula differentiation becomes most pronounced in elementary grades, prompting schools to layer enrichment clubs, coding sessions, and language electives that command incremental fees. However, premium oversubscription in Dubai and Abu Dhabi pushes new entrants toward mid-market suburban campuses, balancing price points with operational upside. Secondary programs remain capacity-constrained yet lucrative: Advanced Placement, IB Diploma, and university counselling packages bolster fees, with boarding models like Swiss International Scientific School Dubai extending share of wallet. The segmented revenue stack thus diversifies risk across economic cycles, preserving resilience for the GCC private K-12 education market.

The GCC Private K-12 Education Market is Segmented by Source of Revenue (Kindergarten, Primary, and More), by Curriculum (American, British, and More), by Nationality (Expat Students and Local Students), and Country (Saudi Arabia, United Arab Emirates, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- GEMS Education

- Taaleem

- Aldar Education

- National Company for Learning & Education

- SABIS Educational Services

- Al-Jazeera Academy

- British International School of Jeddah

- International Schools Group

- Dubai International Academy

- Nord Anglia Education

- Cognita Schools

- Aldenham Education

- Al Darajah Schools

- Wesgreen International School

- Britus Education

- Al Injaz Private School

- Azzan Bin Qais International School

- Muscat International Schools

- Nadeen International School

- The International School of Choueifat

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government reforms & record-high education budgets

- 4.2.2 Rapid expatriate inflow boosting international-curriculum demand

- 4.2.3 Rising disposable incomes enabling premium tuition fees

- 4.2.4 EdTech adoption elevating learning outcomes

- 4.2.5 PPP school-infrastructure wave unlocking private capital

- 4.2.6 Sharia-compliant financing widening investor pool

- 4.3 Market Restraints

- 4.3.1 Chronic shortage of qualified teachers

- 4.3.2 Escalating land & construction costs for campuses

- 4.3.3 Tuition-fee caps squeezing margins

- 4.3.4 Premium-school saturation in Dubai & Abu Dhabi

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Government Spending & Funding Analysis

- 4.9 COVID-19 Impact Assessment

5 Market Size & Growth Forecasts

- 5.1 By Source of Revenue

- 5.1.1 Kindergarten

- 5.1.2 Primary

- 5.1.3 Intermediary

- 5.1.4 Secondary

- 5.2 By Curriculum

- 5.2.1 American

- 5.2.2 British

- 5.2.3 Arabic

- 5.2.4 CBSE

- 5.2.5 Other

- 5.3 By Nationality

- 5.3.1 Expat Students

- 5.3.2 Local Students

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Oman

- 5.4.5 Bahrain

- 5.4.6 Kuwait

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 GEMS Education

- 6.4.2 Taaleem

- 6.4.3 Aldar Education

- 6.4.4 National Company for Learning & Education

- 6.4.5 SABIS Educational Services

- 6.4.6 Al-Jazeera Academy

- 6.4.7 British International School of Jeddah

- 6.4.8 International Schools Group

- 6.4.9 Dubai International Academy

- 6.4.10 Nord Anglia Education

- 6.4.11 Cognita Schools

- 6.4.12 Aldenham Education

- 6.4.13 Al Darajah Schools

- 6.4.14 Wesgreen International School

- 6.4.15 Britus Education

- 6.4.16 Al Injaz Private School

- 6.4.17 Azzan Bin Qais International School

- 6.4.18 Muscat International Schools

- 6.4.19 Nadeen International School

- 6.4.20 The International School of Choueifat

7 Market Opportunities & Future Outlook

- 7.1 Mid-market bilingual schools for Saudi & Emirati nationals

- 7.2 AI-driven personalized learning platforms for private operators