PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940635

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940635

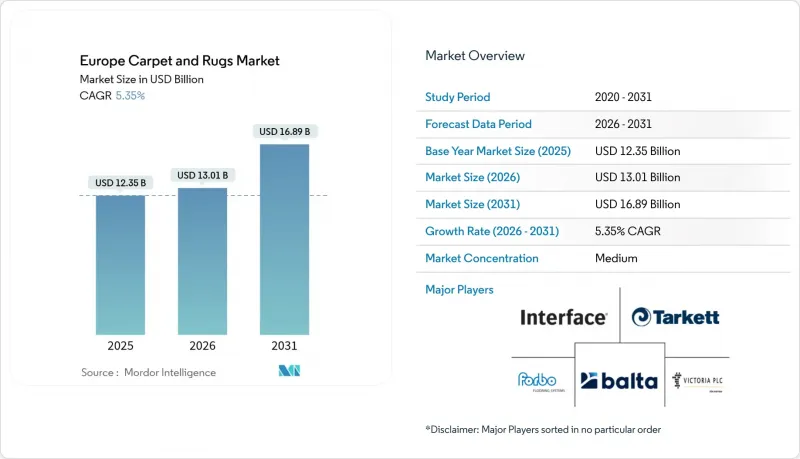

Europe Carpet And Rugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe carpet and rugs market is expected to grow from USD 12.35 billion in 2025 to USD 13.01 billion in 2026 and is forecast to reach USD 16.89 billion by 2031 at 5.35% CAGR over 2026-2031.

Recent growth reflects renovation spending in homes, a rebound in Mediterranean hospitality construction, and a regulatory pivot toward circular-economy flooring solutions. Advances in high-speed tufting and digital printing enable mass customization without eroding cost competitiveness, which helps soft flooring retain share against hard-surface alternatives. Recycled and bio-based fibers grow faster than conventional synthetics as the EU's Extended Producer Responsibility (EPR) rules reward materials with lower environmental footprints. Germany anchors regional demand through a dense manufacturing base and design heritage, while Spain leads growth as resort pipelines reopen and tourism strengthens. Competitive intensity remains moderate: scaled suppliers such as Tarkett, Interface, Balta Group, Victoria PLC, and Forbo balance price discipline with investment in closed-loop production and carbon-negative innovations.

Europe Carpet And Rugs Market Trends and Insights

Post-pandemic Residential Renovation Up-cycle

European homeowners continue to upgrade interiors after lifestyle shifts that began in 2020. Carpets appeal for warmth and sound absorption in hybrid work settings, which sustains premium price points. Limited new-housing supply pushes families to renovate rather than relocate, extending demand beyond the initial surge. The renovation cycle extends beyond immediate pandemic responses, as housing market constraints force homeowners to invest in existing properties rather than relocate. Carpet manufacturers are capitalizing through enhanced merchandising strategies that emphasize aspirational design elements and premium material compositions. The shift toward personalized home environments creates sustained demand for customizable carpet solutions that align with individual aesthetic preferences.

Hospitality Project Pipeline Revival Across Mediterranean Resorts

Deferred resort developments in Spain, Italy, and Greece return to construction schedules. Hilton alone opened 10 European resorts in 2024, adding more than 1,500 rooms that specify soft flooring for guest comfort and swift replacement cycles. Commercial buyers prefer carpet tiles that limit downtime when spots need substitution. This hospitality revival particularly benefits commercial carpet segments requiring enhanced durability and stain resistance for high-traffic applications. Resort operators prioritize modular carpet tile solutions that enable rapid maintenance and replacement cycles without disrupting guest experiences. The Mediterranean focus creates regional demand concentration in Spain, Italy, and Southern France, where tourism recovery drives sustained infrastructure investment.

Consumer Shift Toward Hard-surface Flooring

Minimalist aesthetics, easy cleaning routines, and allergy concerns encourage many households in Northern Europe to choose wood, stone, or luxury vinyl. In 2024, hard surfaces represented 60% of total flooring purchases, shrinking broadloom volumes. This trend reflects changing lifestyle preferences that prioritize easy maintenance and allergen reduction over traditional carpet benefits like warmth and acoustic comfort. The shift is most pronounced in residential applications, where 60% of flooring purchases now favor hard surfaces over soft alternatives. Carpet manufacturers are responding through hybrid product strategies that combine carpet comfort with hard-surface practicality, including waterproof carpet innovations and modular tile systems that enable selective replacement.

Other drivers and restraints analyzed in the detailed report include:

- Advances in High-speed Tufting & Digital-print Technologies

- EU Circular-economy Mandates Boosting Demand for Recycled-content Carpets

- Volatile Prices of Petroleum-based Synthetic Fibers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tufted constructions anchored 55.10% revenue in 2025 for the Europe carpet and rugs market, sustained by rapid production cycles and cost efficiency. Needle-punched carpets grow at 6.09% CAGR to 2031 as commercial buyers value robustness and stain resistance. Woven carpets keep a luxury niche, yet higher labor costs limit volume. Knotted products struggle under rising wages, though artisans preserve cultural value. Flat-weave and braided styles gain attention from design-forward consumers but stay a niche share.

Manufacturers deploy digital printers on tufted and needle-punched lines to release micro-collections with minimal inventory. That flexibility helps retain soft surface spend when consumers might otherwise migrate to hard floors. Production scalability secures competitive pricing that maintains category leadership despite mounting regulatory costs. Tufted carpet dominance stems from production scalability and cost competitiveness against alternative manufacturing methods, while maintaining aesthetic versatility through varied pile heights and textures that appeal to both residential and commercial applications.

Polypropylene remained the largest material, claiming 37.85% share of the Europe carpet and rugs market size in 2025, owing to stain resistance and moisture tolerance in hospitality and healthcare settings. Recycled and bio-based fibers, however, rise at an 8.41% CAGR through 2031 as EPR fees decline for eco-friendly content. Nylon keeps its premium status because of durability, but loses ground to improved PET. Wool and plant-based fibers address high-end applications where natural credentials carry price premiums.

The Europe carpet and rugs market rewards suppliers able to source post-consumer PET at scale and certify traceability. Investments in depolymerization and mechanical recycling expanded raw-material pools. Brands publicize lifecycle assessments that quantify reduced carbon footprints, which strengthen bids for public buildings subject to green-procurement rules. The material segmentation reflects industry transformation toward synthetic alternatives that can deliver natural fiber benefits through technological innovation rather than traditional material sourcing approaches.

The Europe Carpet and Rugs Market Report is Segmented by Product Type (Tufted, Woven, Needle-Punched, Knotted, Others), Material (Nylon, Polyester, Polypropylene, Wool, Other Natural Fibres, Recycled & Bio-Based), End User (Residential, Commercial), Distribution Channel (B2B, B2C), and Geography (UK, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Tarkett S.A.

- Interface Inc.

- Balta Group

- Victoria PLC

- Forbo Flooring Systems

- Mohawk Industries Inc. (IVC, Godfrey Hirst)

- Shaw Industries Group Inc.

- Beaulieu International Group

- Milliken & Company

- Oriental Weavers Group

- Brintons Carpets Ltd.

- Vorwerk Flooring

- Ege Carpets A/S

- Associated Weavers Europe

- Louis De Poortere

- Lano Carpets

- Abingdon Flooring

- Ragolle Rugs NV

- The Rug Company

- Fletco Carpets

- Cormar

- Cavalier

- Balsan

- Burmatex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hospitality Project Pipeline Revival Across Mediterranean Resorts

- 4.2.2 Advances In High-Speed Tufting & Digital-Print Technologies

- 4.2.3 Eu Circular-Economy Mandates Boosting Demand For Recycled-Content Carpets

- 4.2.4 Ai-Driven, On-Demand Design Customization Showcased At European Textile Fairs

- 4.2.5 Post-pandemic residential renovation up-cycle

- 4.2.6 Open-plan-office acoustic rules drive demand for sound-absorbing carpet tiles

- 4.3 Market Restraints

- 4.3.1 Consumer Shift Toward Hard-Surface Flooring

- 4.3.2 Volatile Prices Of Petroleum-Based Synthetic Fibres

- 4.3.3 Rising Compliance Cost Under Eu Eco-Design & Environmental Science And Pollution Research (Espr) Regulations

- 4.3.4 Loom-Operator & Craft-Skills Shortage In Traditional Weaving Clusters

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 4.8 Insights into Consumer Behaviour Analysis in the Market

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Tufted

- 5.1.2 Woven

- 5.1.3 Needle-Punched

- 5.1.4 Knotted / Hand-Knotted

- 5.1.5 Others (Flat-weave, Hooked, Braided)

- 5.2 By Material

- 5.2.1 Nylon

- 5.2.2 Polyester (PET & PTT)

- 5.2.3 Polypropylene

- 5.2.4 Wool

- 5.2.5 Other Natural Fibres (Jute, Sisal, Cotton, Silk)

- 5.2.6 Recycled & Bio-based Fibres

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality & Leisure

- 5.3.2.2 Corporate Offices

- 5.3.2.3 Retail

- 5.3.2.4 Healthcare & Educational Institutions

- 5.3.2.5 Other Commercial Facilities

- 5.4 By Distribution Channel

- 5.4.1 B2B/Direct from the Manufacturers

- 5.4.2 B2C/Retail

- 5.4.2.1 Home-Improvement & DIY Stores

- 5.4.2.2 Specialty Flooring Stores (includes exclusive brand outlets)

- 5.4.2.3 Furniture & Furnishing Stores

- 5.4.2.4 Online

- 5.4.2.5 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tarkett S.A.

- 6.4.2 Interface Inc.

- 6.4.3 Balta Group

- 6.4.4 Victoria PLC

- 6.4.5 Forbo Flooring Systems

- 6.4.6 Mohawk Industries Inc. (IVC, Godfrey Hirst)

- 6.4.7 Shaw Industries Group Inc.

- 6.4.8 Beaulieu International Group

- 6.4.9 Milliken & Company

- 6.4.10 Oriental Weavers Group

- 6.4.11 Brintons Carpets Ltd.

- 6.4.12 Vorwerk Flooring

- 6.4.13 Ege Carpets A/S

- 6.4.14 Associated Weavers Europe

- 6.4.15 Louis De Poortere

- 6.4.16 Lano Carpets

- 6.4.17 Abingdon Flooring

- 6.4.18 Ragolle Rugs NV

- 6.4.19 The Rug Company

- 6.4.20 Fletco Carpets

- 6.4.21 Cormar

- 6.4.22 Cavalier

- 6.4.23 Balsan

- 6.4.24 Burmatex

7 Market Opportunities & Future Outlook

- 7.1 Rising Demand For Artisanal And Handcrafted Carpets

- 7.2 Increasing Prevalence Of Technological Integration For Smart Carpets