PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940636

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940636

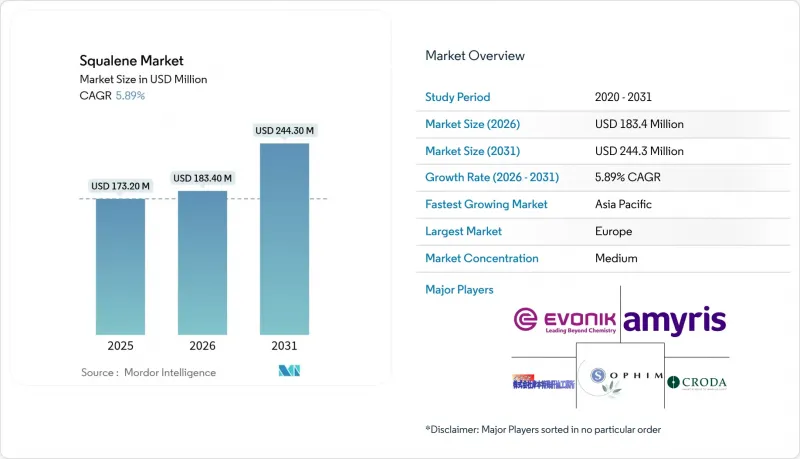

Squalene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Squalene market is expected to grow from USD 173.20 Million in 2025 to USD 183.4 Million in 2026 and is forecast to reach USD 244.3 Million by 2031 at 5.89% CAGR over 2026-2031.

Demand accelerates as regulators discourage shark-derived inputs and premium skincare brands embed plant-based alternatives that enhance ultraviolet (UV) protection and collagen biosynthesis. Pharmaceutical pipelines add another growth layer by specifying high-purity squalene for vaccine adjuvants and lipid nanoparticle delivery, while precision-fermentation producers unlock scalable synthetic routes that bypass agricultural limits. Europe's mature sustainability codes and Asia-Pacific's expanding middle class jointly shape the competitive playbook, prompting incumbents to secure green upstream partnerships and smaller biotech entrants to commercialize fermentation know-how.

Global Squalene Market Trends and Insights

Surging Demand for Plant-derived Squalene in Premium Skincare

Plant-derived squalene meets consumer requests for clean, multifunctional actives that protect against ultraviolet A (UVA)-induced oxidative stress and stimulate collagen formation . Asian beauty brands highlight the ingredient's non-comedogenic profile, dovetailing with a regional move toward skin-barrier health. European firms scale olive-oil and amaranth supply streams, converting agricultural by-products into high-purity inputs. Positioning strategies are reinforced by labels that trace origin and carbon savings, building trust among Generation Z (Gen Z) buyers who scrutinize ingredient sourcing. Product formulators now incorporate squalene concentrations as low as 0.005% to improve texture without compromising stability, anchoring the squalene market in premium price tiers.

Rapid Adoption in Vaccine Adjuvants & Lipid-nanoparticle Drugs

Clinical data show that squalene-based emulsions outperform mineral oil comparators in antibody titers, prompting national stockpiles to specify GMP-grade supply. The modality proved vital during COVID-19, when scalable lipid carriers were needed for messenger Ribonucleic Acid (mRNA) vaccines. Croda's multi-year contract with Amyris secures biotechnology-derived material that satisfies stringent pharmacopeial limits while eliminating marine sourcing risk. Oncology pipelines that hinge on lipid nanoparticles for targeted delivery further enlarge high-margin demand, explaining why GMP-grade volumes grow faster than cosmetic grades in the squalene market.

Ethical & Regulatory Bans on Shark-derived Sourcing

The BLOOM Association estimates that 3 million deep-sea sharks are slaughtered annually for squalene extraction, sparking import restrictions and labelling mandates in the European Union . North America applies similar scrutiny via Lacey-Act enforcement, forcing brand owners to certify non-animal origins. The immediate effect is a squeeze on legacy supply chains that had relied on low-cost marine oil. Transition costs weigh on smaller formulators, although the policy accelerates market share gains for vegetable and biosynthetic streams in the squalene market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Fermentation & Synthetic-biology Production

- Expansion of Sustainable-beauty Standards Across Asia-Pacific (APAC)

- Climate-driven Volatility in Olive-oil Based Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vegetable derivatives led with 37.78% of the Squalene market size in 2025 and are forecast to expand at 6.72% CAGR through 2031. The leadership stems from upgrades in olive oil pomace extraction, amaranth seed processing, and sugarcane farnesene hydrogenation that displace shark liver oil altogether. Amaranth-based PhytoSquene satisfies European Pharmacopoeia purity while remaining free of animal-origin contaminants, giving formulators an immediate compliance route. Though still modest, biosynthetic volumes rise quickest as precision fermentation eliminates crop-yield swings and shortens lead times.

Animal-source barrels continue to contract as consumer sentiment and customs codes turn unfavourable. Other minor feedstocks, such as wheat germ and rice bran oils, address specific regional supply gaps but lack the scalability of olive or cane pathways. Overall, plant and biosynthetic inputs reshape the competitive map, lowering entry barriers and broadening the geographic footprint of the squalene market.

The Squalene Market Report is Segmented by Source (Animal Source, Vegetable Source, Biosynthetic, and Other Sources), Purity Grade (Cosmetic Grade, Pharmaceutical GMP Grade, and Food Grade), End-User Industry (Cosmetics, Pharmaceuticals, Food, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe's 41.60% share of the Squalene market size in 2025 reflects a combination of stringent sustainability directives and advanced personal-care manufacturing ecosystems. Regulatory bodies restrict shark inputs while encouraging traceable plant or biosynthetic origins, pushing formulators toward certifications that enhance brand equity. Olive oil by-products remain key, but climate variability prompts investment in amaranth and cane pathways. Biopharma clusters in Germany and France raise GMP-grade demand, and collaborative funding, such as L'Oreal's EUR 35 million injection into a regional fermentation hub, cements supply security.

Asia-Pacific is the fastest-growing region at a projected 6.55% CAGR to 2031. Rising disposable incomes in China, Japan, and South Korea stimulate premium skin-care consumption that integrates squalene for barrier-repair and anti-aging benefits. Ministry of Health, Labor and Welfare (MHLW)'s ingredient-positive list encourages local brands to phase out marine-derived material, and social-commerce platforms amplify consumer scrutiny of clean sourcing. Replacement of shark squalene, documented at 53% prevalence in 2024, presents immediate upside for plant and biosynthetic variants. Regional contract manufacturers already retrofit lines to handle vegetable inputs, further entrenching the growth outlook of the squalene market.

North America combines biotechnology innovation with policy support that favours domestic biomanufacturing. Precision-fermentation ventures concentrate around the San Francisco Bay Area and Boston, supplying both cosmetic and vaccine-ready grades. United States Environmental Protection Agency (EPA)'s low-priority listing of squalene under Toxic Substances Control Act (TSCA) lowers regulatory friction, while the White House bioeconomy agenda channels grants toward scale-up infrastructure. South America and the Middle East & Africa contribute modest but rising volumes as knowledge of sustainable beauty penetrates local markets and as sugarcane resources in Brazil create potential feedstock synergies. Collectively, regional demand convergence reinforces the global expansion path of the squalene market.

- Aasha Biochem

- Amyris

- Arista Industries, Inc.

- Croda International Plc

- EFP Biotek

- Evonik Industries AG

- GIHI CHEMICALS CO., LIMITED

- Kishimoto Special Liver Oil Co., Ltd.

- KURARAY CO., LTD.

- Oleicfat SL

- ROELMI HPC

- SeaDragon

- Seppic

- Sophim

- Unilong Industry Co., Ltd.

- Vestan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Plant-derived Squalene in Premium Skincare

- 4.2.2 Rapid Adoption in Vaccine Adjuvants & Lipid-nanoparticle Drugs

- 4.2.3 Shift Toward Fermentation & Synthetic-biology Production

- 4.2.4 Expansion of Sustainable-beauty Standards Across Asia-Pacific (APAC)

- 4.2.5 Emerging Oncology Nano-delivery Pipelines Using High-purity Squalene

- 4.3 Market Restraints

- 4.3.1 Ethical & Regulatory Bans on Shark-derived Sourcing

- 4.3.2 Climate-driven Volatility in Olive-oil Based Feedstock Prices

- 4.3.3 Fermentation Capacity Bottlenecks for Farnesene

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Source

- 5.1.1 Animal Source

- 5.1.2 Vegetable Source

- 5.1.3 Biosynthetic

- 5.1.4 Other Sources

- 5.2 By Purity Grade

- 5.2.1 Cosmetic Grade

- 5.2.2 Pharmaceutical (GMP) Grade

- 5.2.3 Food Grade

- 5.3 By End-User Industry

- 5.3.1 Cosmetics

- 5.3.2 Pharmaceuticals

- 5.3.3 Food

- 5.3.4 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 Nigeria

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aasha Biochem

- 6.4.2 Amyris

- 6.4.3 Arista Industries, Inc.

- 6.4.4 Croda International Plc

- 6.4.5 EFP Biotek

- 6.4.6 Evonik Industries AG

- 6.4.7 GIHI CHEMICALS CO., LIMITED

- 6.4.8 Kishimoto Special Liver Oil Co., Ltd.

- 6.4.9 KURARAY CO., LTD.

- 6.4.10 Oleicfat SL

- 6.4.11 ROELMI HPC

- 6.4.12 SeaDragon

- 6.4.13 Seppic

- 6.4.14 Sophim

- 6.4.15 Unilong Industry Co., Ltd.

- 6.4.16 Vestan

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Microbial Strains for Improved Productivity and Yields of Squalene