PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940693

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940693

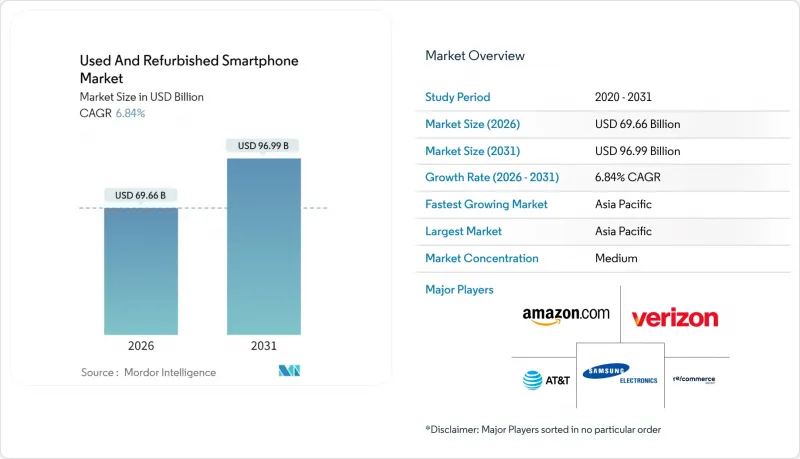

Used And Refurbished Smartphone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Used And Refurbished Smartphone market is expected to grow from USD 65.20 billion in 2025 to USD 69.66 billion in 2026 and is forecast to reach USD 96.99 billion by 2031 at 6.84% CAGR over 2026-2031.

In terms of shipment volume, the market is expected to grow from 315 million units in 2025 to 430 million units by 2030, at a CAGR of 6.42% during the forecast period (2025-2030). Asia-Pacific region buoyed by high new-device prices, growing OEM trade-in programs, and regulatory pressure to curb e-waste. Flagship devices priced above USD 1,300 push price-sensitive buyers toward certified alternatives, while 5G upgrade cycles recycle a steady flow of near-new handsets into the secondary channel. Online marketplaces have streamlined grading, warranty, and returns, shrinking the trust gap that once limited growth. Enterprises are joining consumers in device reuse to hit emissions goals and trim hardware budgets. Collectively, these forces position the used and refurbished smartphones market for resilient, broad-based expansion.

Global Used And Refurbished Smartphone Market Trends and Insights

Rising Smartphone Prices Narrow the Affordability Window

Flagship devices such as the iPhone 16 Pro Max list at USD 1,399.99, placing premium hardware beyond reach for many buyers . Certified units of the same model sell 30-40% lower, widening the value gap that fuels the used and refurbished smartphones market. In emerging economies, refurbished imports often represent the only financially viable path to 5G connectivity, turning price inflation into a structural growth catalyst.

OEM Certification Programs Reset Quality Expectations

Apple, Samsung, and other OEMs guarantee new batteries, cosmetic refurbishing, and full-year warranties, lifting consumer confidence and standardizing device grades. Financing from the European Investment Bank, EUR 17 million to Swappie in 2024, underscores investor belief in scale refurbishment models .

Consumer Concerns About Reliability Persist

Even with OEM guarantees, 65% of prospective buyers cite battery degradation and waterproofing loss as top worries, dampening adoption in first-time refurb markets . Educational campaigns and extended warranties remain essential to lower perceived risk.

Other drivers and restraints analyzed in the detailed report include:

- 5G Upgrade Waves Boost Supply Quality

- Online Marketplaces Remove Transaction Friction

- Counterfeit Components Undercut Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certified pre-owned units are accelerating at a 7.28% CAGR, while standard used phones still dominate volume at 60.85%. The used and refurbished smartphones market size for certified devices is lifted by automated testing solutions such as Phonecheck that complete diagnostics in two minutes. Increasingly, buyers equate OEM certification with near-new quality, enabling premium pricing.

Peer-to-peer resales remain popular for low-value handsets, yet stringent import laws and upcoming EU right-to-repair mandates are expected to push more trade through professional refurbishers. This structural shift narrows the quality gap and pushes value toward branded, warrantied inventory.

Online portals accounted for 38.22% of 2025 turnover, reflecting consumer preference for click-to-door convenience and transparent return policies. Carrier trade-in desks feed inventory pipelines; AT&T alone collected 12.5 million devices in 2024. OEM storefronts, though smaller, are the fastest-growing channel at 8.88% CAGR as brands monetize secondary demand directly while safeguarding user experience.

Physical retailers retain relevance for shoppers who value in-hand inspection, especially in emerging markets where digital payment penetration lags. Blended online-offline strategies, including kiosk-based instant payment options, are gaining traction to ease the transition.

The Used and Refurbished Smartphone Market Report is Segmented by Device Condition (Used, Refurbished/Certified Pre-Owned), Sales Channel (Online Marketplaces, Offline Retailers, and More), Price Band (< USD 100, USD 100-199, USD 200-399, and More), End User (Consumer/Individual, Business/Enterprise, Government/Institutional), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Shipments).

Geography Analysis

Asia-Pacific generated the largest share at 41.05% in 2025, reflecting deep mobile penetration and rapid 5G rollouts. Japan logged 3.15 million secondary sales in fiscal year 2024, up 15.5% year on year, aided by wide retail distribution and aggressive marketing of certified stock. China's e-commerce giants have added dedicated refurbished sections, accelerating mainstream acceptance.

India shows unmet demand constrained by supply gaps; unit volumes dipped 5-7% in 2025 despite Cashify posting INR 955 crore (USD 118 million) revenue, underscoring the importance of collection networks. Southeast Asia, with 20% annual smartphone growth, combines young demographics with rising data consumption, positioning the region for outsized share gains within the used and refurbished smartphones market.

North America leverages mature carrier programs, yet 70% of owners still retain retired devices, signaling latent supply. Corporate take-back schemes and right-to-repair laws could unlock additional flow. Europe benefits from the Ecodesign Directive, effective June 2025, which requires spare-parts availability for seven years, lowering refurbishment costs and enhancing device lifetimes.

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Back Market, Inc.

- Amazon.com, Inc.

- Recommerce Group

- Verizon Communications Inc.

- AT&T Inc.

- Best Buy Co., Inc.

- Alibaba Group Holding Ltd.

- Swappie Oy

- Cashify (Manak Waste Management Private Limited)

- Gazelle (ecoATM, LLC)

- Likewize Corp. (Brightstar Corp.)

- Trocafone, Inc.

- musicMagpie plc (Decluttr)

- FoneGiant Limited

- Reboxed Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising smartphone retail prices driving secondary-market demand

- 4.2.2 Expansion of online marketplaces enabling convenient transactions

- 4.2.3 OEM-led trade-in and certified refurbishment programs

- 4.2.4 Sustainability regulations and consumer eco-consciousness

- 4.2.5 5G-driven device replacement cycles increasing used-phone supply

- 4.2.6 Enterprise device-leasing models feeding high-grade inventory

- 4.3 Market Restraints

- 4.3.1 Consumer concerns around quality and warranties

- 4.3.2 Proliferation of counterfeit parts and grey-market sellers

- 4.3.3 Software security locks limiting refurb viability

- 4.3.4 Tightening e-waste import/export regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Distribution Channel Landscape (OEMs vs Third-Party Platforms)

- 4.8 Impact of 5G on Used and Refurbished Smartphones

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Intensity of Competitive Rivalry

- 4.9.5 Threat of Substitutes

- 4.10 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Condition

- 5.1.1 Used

- 5.1.2 Refurbished/Certified Pre-Owned

- 5.2 By Sales Channel

- 5.2.1 Online Marketplaces

- 5.2.2 Offline Retailers

- 5.2.3 Carrier/Operator Trade-In Programs

- 5.2.4 OEM Certified Refurbished Stores

- 5.2.5 Wholesale/B2B

- 5.3 By Price Band

- 5.3.1 < USD 100

- 5.3.2 USD 100-199

- 5.3.3 USD 200-399

- 5.3.4 USD 400-599

- 5.3.5 >= USD 600

- 5.4 By End User

- 5.4.1 Consumer/Individual

- 5.4.2 Business/Enterprise

- 5.4.3 Government/Institutional

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Back Market, Inc.

- 6.4.4 Amazon.com, Inc.

- 6.4.5 Recommerce Group

- 6.4.6 Verizon Communications Inc.

- 6.4.7 AT&T Inc.

- 6.4.8 Best Buy Co., Inc.

- 6.4.9 Alibaba Group Holding Ltd.

- 6.4.10 Swappie Oy

- 6.4.11 Cashify (Manak Waste Management Private Limited)

- 6.4.12 Gazelle (ecoATM, LLC)

- 6.4.13 Likewize Corp. (Brightstar Corp.)

- 6.4.14 Trocafone, Inc.

- 6.4.15 musicMagpie plc (Decluttr)

- 6.4.16 FoneGiant Limited

- 6.4.17 Reboxed Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment