PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940739

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940739

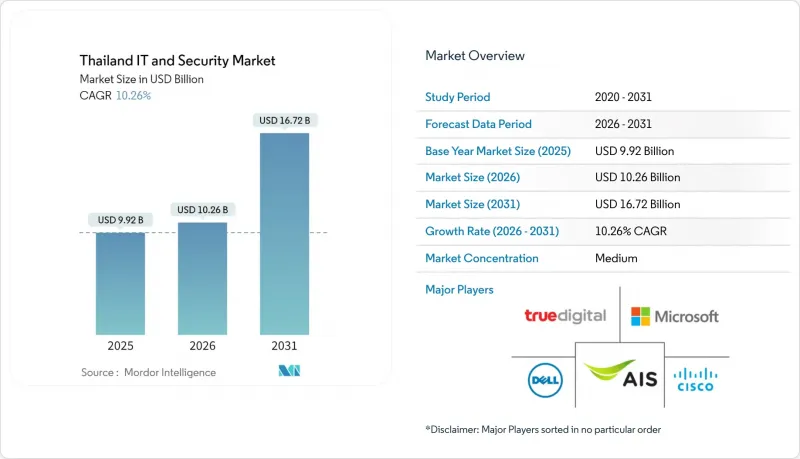

Thailand IT And Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Thailand IT and Security market was valued at USD 8.95 billion in 2025 and estimated to grow from USD 10.27 billion in 2026 to reach USD 20.44 billion by 2031, at a CAGR of 14.78% during the forecast period (2026-2031).

This surge reflects Thailand's positioning as ASEAN's digital-infrastructure hub, the public-sector cloud-first mandate, and sustained hyperscale data-center inflows that already top USD 8.5 billion. Robust 5G coverage of 95% of the population, a THB 1.5 billion national AI budget, and cross-border e-commerce flows energize adoption of edge-to-cloud architectures. Enterprise buyers increasingly favor managed services because the country lacks 30,000 cybersecurity professionals, while new data-protection rules elevate compliance spending. The DTAC heightens competitive intensity-True Corporation merger that reshapes network reach, and by U.S. cloud providers racing to localize availability zones. These forces converge to keep the Thailand IT and Security market on a double-digit growth path through the decade.

Thailand IT And Security Market Trends and Insights

Cloud-First Policy Accelerates Public-Sector Digital Transformation

The Digital Government Development Agency mandates cloud adoption across ministries, dissolving siloed procurement and creating scale for security, integration, and analytics services. Centralized frameworks anchored on ISO/IEC 27001 raise entry barriers for new vendors, while the National Cyber Security Agency's alliance with Google Cloud layers AI-driven threat detection onto government workloads. Local cloud regions address data-sovereignty concerns, bolstering the Thailand IT and Security market as agencies shift budget from hardware to managed platforms.

5G Infrastructure Enables Edge-Computing Proliferation

Advanced Info Service's 95% population coverage underpins low-latency applications in factories, hospitals, and logistics hubs. Manufacturing plants in the Eastern Economic Corridor now stream sensor data to cloud AI engines for real-time quality control, while True Corporation's "True CyberSafe" filters 100,000 risky links per day for mobile users. Telcos thus graduate from connectivity providers to edge-platform operators, deepening their stake in the Thailand IT and Security market.

Cyber-Security Talent Shortage Constrains Market Growth

Banks now pay senior analysts THB 1.8 million (USD 50,000) to secure scarce experts, yet demand still exceeds supply by 30,000 roles. SMEs cannot match wage inflation and therefore defer projects or outsource to MSSPs. Universities scramble to scale curricula, while talent migrates to higher-paying Singapore roles, subtracting momentum from the Thailand IT and Security market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Growth Drives Hyperscale Data-Center Demand

- Export Manufacturing Drives Enterprise Security Compliance

- SME Budget Fragmentation Delays Technology Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

YServices contributed 41.64% of 2025 revenue as enterprises chose managed SOC, threat-hunting, and integration offerings. The Thailand IT and Security market size for services is projected to climb at a 10.55% CAGR as talent scarcity persists. Telecom operators such as True Corporation bundle security with connectivity to upsell higher-margin offerings. Hardware revenues rise steadily on data-center and 5G network capex, but commoditization caps growth. Software, especially AI-assisted analytics, records the fastest run-rate because subscription models shift budgets from capex to opex.

The mix signals Thailand's evolution from hardware-centric builds to software-defined, service-oriented architectures. Specialized integrators tie legacy systems to cloud APIs, while vendors deliver automated playbooks that offset human shortfalls. This pivot keeps the Thailand IT and Security market efficient even as wage pressure mounts.

Cloud controlled 53.12% of the Thailand IT and Security market share in 2025, and sustained a 16.43% CAGR, indicating deepening adoption across verticals. Hyperscalers neutralize data-residency concerns by launching Thai regions, giving regulated banks confidence to migrate core workloads. On-premises persists in defense and critical infrastructure, but hybrid models gain favor as enterprises pair local control with elastic compute.

Cloud security capabilities now often surpass legacy firewalls, prompting risk-averse buyers to accelerate lift-and-shift roadmaps. Integration complexity fuels MSSP demand, while SD-WAN replaces MPLS to cut circuit costs. The Thailand IT and Security market size attached to hybrid deployments will widen as telcos push edge nodes to factories and hospitals.

The Thailand IT and Security Market Report is Segmented by Component (Hardware and Devices, Software, Services), Deployment Mode (On-Premises, Cloud, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Government and Defense, Manufacturing, Healthcare, Retail and E-Commerce, Energy and Utilities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Advanced Info Service Public Co. Ltd (AIS)

- True Digital Group Co. Ltd

- Dell Technologies Inc.

- Cisco Systems Inc.

- International Business Machines Corp. (IBM)

- Microsoft Corporation

- Hewlett Packard Enterprise Co.

- Fujitsu (Thailand) Co. Ltd

- Fortinet Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd

- Trend Micro Inc.

- Kaspersky Lab

- Samsung Electronics Co. Ltd

- Acer Inc.

- Lenovo Group Ltd

- G-Able Co. Ltd

- MFEC Public Co. Ltd

- Digital Government Development Agency (DGA)

- SIAMDATA Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first policy in Thai public sector

- 4.2.2 Acceleration of 5G rollout enabling edge-to-cloud use-cases

- 4.2.3 E-commerce boom driving hyperscale data-center build-outs

- 4.2.4 Board-level adoption of NIST CSF and ISO/IEC 27001 to meet export-market mandates

- 4.2.5 Rise of "Thailand PLUS" near-shoring by Japanese and US manufacturers

- 4.2.6 FinTech regulatory sandbox pushing open-API security spend

- 4.3 Market Restraints

- 4.3.1 Fragmented SME IT budget cycles

- 4.3.2 Shortage of 30,000 cyber-security professionals

- 4.3.3 Legacy MPLS contracts delaying cloud migration

- 4.3.4 High dependence on imported semiconductors amid Baht volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware and Devices

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Retail and E-commerce

- 5.4.6 Energy and Utilities

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials as available, Strategic information, Market rank/share, Products and services, Recent developments)

- 6.4.1 Advanced Info Service Public Co. Ltd (AIS)

- 6.4.2 True Digital Group Co. Ltd

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 International Business Machines Corp. (IBM)

- 6.4.6 Microsoft Corporation

- 6.4.7 Hewlett Packard Enterprise Co.

- 6.4.8 Fujitsu (Thailand) Co. Ltd

- 6.4.9 Fortinet Inc.

- 6.4.10 Palo Alto Networks Inc.

- 6.4.11 Check Point Software Technologies Ltd

- 6.4.12 Trend Micro Inc.

- 6.4.13 Kaspersky Lab

- 6.4.14 Samsung Electronics Co. Ltd

- 6.4.15 Acer Inc.

- 6.4.16 Lenovo Group Ltd

- 6.4.17 G-Able Co. Ltd

- 6.4.18 MFEC Public Co. Ltd

- 6.4.19 Digital Government Development Agency (DGA)

- 6.4.20 SIAMDATA Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment