PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940745

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940745

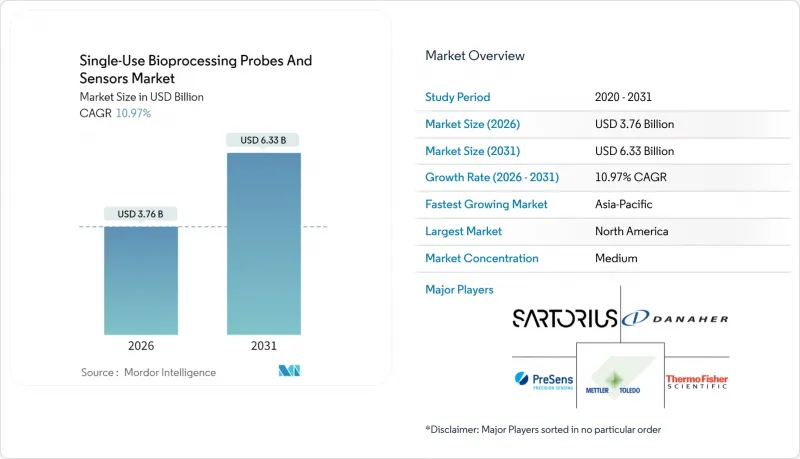

Single-Use Bioprocessing Probes And Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

single-use bioprocessing probes and sensors market size in 2026 is estimated at USD 3.76 billion, growing from 2025 value of USD 3.39 billion with 2031 projections showing USD 6.33 billion, growing at 10.97% CAGR over 2026-2031.

Expansion is underpinned by biopharmaceutical manufacturers moving from stainless-steel instruments to disposable monitoring solutions that lower contamination risk, shorten validation cycles, and trim capital budgets for green-field plants. Regulatory incentives set by the FDA's Advanced Manufacturing Technologies Designation Program are accelerating uptake of real-time analytics that meet Process Analytical Technology (PAT) requirements . Technological gains in thin-film printed electrodes and fluorescence-based optics are lowering the total cost of ownership and opening new use cases in continuous manufacturing. Meanwhile, supply-chain diversification and sustainability mandates are shaping material choices, especially for fluoropolymer components, and prompting R&D in recyclable or bio-based alternatives.

Global Single-Use Bioprocessing Probes And Sensors Market Trends and Insights

Commercial Advantages Over Stainless-Steel Probes & Sensors

Single-use designs remove cleaning and re-qualification steps, enabling contract manufacturing sites to switch batches without 48-72 hour sterilization downtime. FDA guidance issued in 2025 explicitly recognizes disposable sensors as an enabling technology for resilient production. Factory-calibrated products such as Mettler-Toledo's InSUS 310 deliver 30-month shelf life, thereby eliminating on-site calibration . Cost benefits resonate strongly in emerging markets where plants favor operational expenditure models. University research centers, including Oxford's BiPAD facility, have adopted similar platforms to accelerate translational studies .

CAPEX-Light Green-Field Biologics Capacity Buildouts in Asia & MENA

Modular single-use suites reduce up-front investment and speed regulatory approval in regions where biologics pipelines are expanding rapidly. Resilience's partnership with Mubadala to build the UAE's first GMP biologics site uses this approach to deliver pandemic-ready capacity without stainless-steel infrastructure. Cytiva earmarked USD 300 million of a broader USD 1.5 billion budget specifically for disposable systems to serve Asian customers, reinforcing the strategic weight of the single-use bioprocessing probes and sensors market in regional expansion plans. Biosimilar manufacturers in India, South Korea, and China leverage this flexibility to reduce time-to-market.

Plastic Waste Legislation Tightening in EU & California Raises Disposal-Cost Risk

California mandates 65% recycling of single-use plastic packaging by 2032, while EU circular-economy policies impose extended producer responsibility fees. Disposable sensor housings often employ multi-layer fluoropolymers that resist conventional recycling, driving higher disposal charges. Sensor makers are investigating polylactic-acid blends; however, durability and chemical resistance remain gaps for GMP use. Life-cycle studies point to a potential 39% CO2 reduction from optimized material choices, but the cost-benefit requires further validation.

Other drivers and restraints analyzed in the detailed report include:

- Decentralised Vaccine Manufacturing Hubs Require Modular SU Monitoring

- PAT Mandates in FDA & EMA Guidelines Accelerating Real-Time SU Sensor Adoption

- Supply Chain Dependence on Specialty Fluoropolymer Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

pH sensors accounted for 23.02% of 2025 revenue, making them the largest product category within the single-use bioprocessing probes and sensors market. Demand is rooted in regulatory expectations for tight pH control during mammalian cell culture. Hamilton's gamma-sterilized OneFerm line illustrates market preference for pre-calibrated glass electrodes that withstand 24-month storage. The segment is further supported by increased multi-batch manufacturing, where disposable probes prevent carry-over contamination and cut cleaning validation expenses.

Dissolved oxygen sensors are expected to grow with a CAGR of 14.62%. Dissolved oxygen and temperature sensors maintain steady uptake as essential process safeguards, while pressure and conductivity variants target niche purification and filtration steps. Intelligent Sensor Management software that predicts end-of-life parameters is being bundled across families of probes, reinforcing cross-selling opportunities. Continuous improvements ensure the single-use bioprocessing probes and sensors market retains high switching costs for established brands.

Electrochemical designs held a 36.21% share in 2025 and are set to grow at 11.92% annually as manufacturers endorse maintenance-free measurement. Fluorescence quenching for dissolved oxygen offers faster response and resists gamma-induced drift, addressing a core reliability concern.

Multi-wavelength probes integrate pH, oxygen, and biomass analytics into a single port, freeing headspace in compact bioreactors relevant to personalized therapy production. Capacitive and impedance sensors, while niche, provide label-free monitoring for advanced glycosylation profiling. Collectively, advances in optics will push the single-use bioprocessing probes and sensors market toward denser data capture that supports autonomous plant concepts.

The Single-Use Bioprocessing Probes and Sensors Market Report is Segmented by Type (pH Sensors, Dissolved Oxygen Sensors, and More), Sensor Technology (Electrochemical, Optical and Fluorescence, and More), Workflow (Upstream, Downstream), End User (Biopharmaceutical Manufacturers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.35% of 2025 revenue, buoyed by FDA leadership in advancing PAT and by Thermo Fisher's USD 2 billion domestic expansion program that reinforces local supply chains. Canada's biologics corridor in Quebec and Mexico's contract manufacturing clusters also contribute, leveraging NAFTA-facilitated trade for consumables. Early adoption of continuous manufacturing raises baseline sensor demand, keeping the region at the innovation forefront of the single-use bioprocessing probes and sensors market.

Europe ranks second and benefits from regulatory harmonization between EMA and FDA. Germany's equipment manufacturers supply high-precision optics, while the United Kingdom accelerates investment in cell and gene therapy infrastructure. Circular-economy directives are compelling R&D into recyclable housings, positioning the bloc as a test bed for sustainable single-use formats. Southern European countries capitalize on EU recovery funds to modernize legacy plants with disposable suites, cushioning growth prospects.

Asia-Pacific is the fastest-growing territory, expanding 12.05% per year through 2031. Chinese government incentives for domestic biologics and biosimilar production, combined with South Korea's 6,100 m2 Cytiva facility, underpin capacity expansion. Japan's mature regulatory framework demands high-end optical probes, while India's contract service providers favor cost-optimized packages. Australia and Singapore amplify demand through vibrant biotech ecosystems. Elsewhere, the UAE's tie-up with Resilience signals new Gulf involvement, and Brazil's formulation plants anchor Latin American uptake, collectively broadening the single-use bioprocessing probes and sensors market footprint.

- Thermo Fisher Scientific

- Sartorius

- Danaher

- Merck KGaA (MilliporeSigma)

- Pall

- PreSens Precision Sensing

- METTLER TOLEDO (Intelligent Sensor Solutions & PendoTECH)

- Hamilton Company

- Broadley-James

- Parker Hannifin

- Dover Corporation (Malema)

- Equflow BV

- Avantor

- Eppendorf

- Endress+Hauser Group

- Emerson Electric

- Finesse Solutions

- Flownamics Analytical

- Watson-Marlow Fluid Technology

- CerCell AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercial Advantages Over Stainless-Steel Probes & Sensors

- 4.2.2 CAPEX-Light Green-Field Biologics Capacity Buildouts in Asia & MENA

- 4.2.3 Decentralised Vaccine Manufacturing Hubs Require Modular SU Monitoring

- 4.2.4 PAT Mandates In FDA & EMA Guidelines Accelerating Real-Time SU Sensor Adoption

- 4.2.5 Integration Of Printable Thin-Film Sensor Chips Lowering BOM Cost Below Legacy Glass Probes

- 4.2.6 AI-Driven Continuous Bioprocessing Needs Multi-Parameter Single-Use Sensor Arrays

- 4.3 Market Restraints

- 4.3.1 Plastic Waste Legislation Tightening in EU & California Raises Disposal-Cost Risk

- 4.3.2 Supply Chain Dependence on Specialty Fluoropolymer Feedstocks

- 4.3.3 Calibration Drift in Gamma-Irradiated Optical Probes Limits Re-Use in Long Campaigns

- 4.3.4 Data-Integration Gaps with Legacy DCS/SCADA In Brown-Field Plants

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 pH Sensors

- 5.1.2 Dissolved Oxygen Sensors

- 5.1.3 Pressure Sensors

- 5.1.4 Temperature Sensors

- 5.1.5 Conductivity Sensors

- 5.1.6 Flow Meters & Sensors

- 5.1.7 Other Types

- 5.2 By Sensor Technology

- 5.2.1 Electrochemical

- 5.2.2 Optical and Fluorescence

- 5.2.3 MEMS-based Pressure & Temperature

- 5.2.4 Other Technologies

- 5.3 By Workflow

- 5.3.1 Upstream

- 5.3.2 Downstream

- 5.4 By End User

- 5.4.1 Biopharmaceutical Manufacturers

- 5.4.2 CMOs & CROs

- 5.4.3 Academic & Research Institutes

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Sartorius AG

- 6.3.3 Danaher Corporation (Cytiva)

- 6.3.4 Merck KGaA (MilliporeSigma)

- 6.3.5 Pall Corporation

- 6.3.6 PreSens Precision Sensing GmbH

- 6.3.7 METTLER TOLEDO (Intelligent Sensor Solutions & PendoTECH)

- 6.3.8 Hamilton Company

- 6.3.9 Broadley-James Corporation

- 6.3.10 Parker-Hannifin Corporation

- 6.3.11 Dover Corporation (Malema)

- 6.3.12 Equflow BV

- 6.3.13 Avantor, Inc.

- 6.3.14 Eppendorf AG

- 6.3.15 Endress+Hauser Group

- 6.3.16 Emerson Electric Co.

- 6.3.17 Finesse Solutions

- 6.3.18 Flownamics Analytical

- 6.3.19 Watson-Marlow Fluid Technology

- 6.3.20 CerCell AS

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment