PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940776

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940776

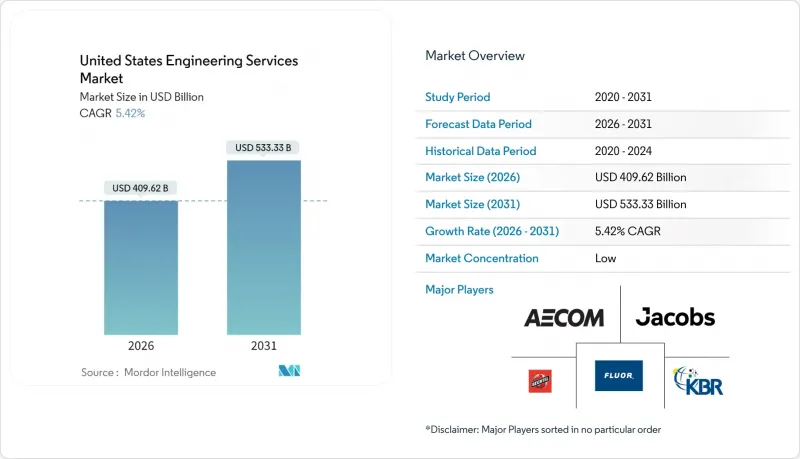

United States Engineering Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The U.S. engineering services market was valued at USD 388.56 billion in 2025 and estimated to grow from USD 409.62 billion in 2026 to reach USD 533.33 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031).

Accelerated federal infrastructure outlays under the Infrastructure Investment and Jobs Act, the CHIPS and Science Act's semiconductor incentives, and persistent defense-modernization budgets are sustaining a multi-year pipeline of complex projects that require deeper engineering expertise. Demand patterns are also being reshaped by manufacturing reshoring, grid-modernization imperatives, and the rapid commercialization of digital-twin workflows that cut rework and expand lifetime asset-management revenues. Competitive behavior is shifting toward acquisitions aimed at specialty capabilities-especially in clean-energy systems, advanced manufacturing, and AI-enabled design-while clients' cost pressures are encouraging integrated EPCM models. Regional demand is clustering around California, Texas, the Great Lakes corridor, and fast-growing Southeast metros where fiscal incentives, lower land costs, and pro-business regulation encourage sustained capital deployment.

United States Engineering Services Market Trends and Insights

Federal Infrastructure-Funding Boom Under 2021 IIJA

The USD 1.2 trillion IIJA marks the most aggressive federal commitment to physical assets since the Interstate Highway era, forcing agencies to hire external specialists for multi-disciplinary tasks that span geotechnical studies, resilient water systems, and intelligent-transportation networks. State DOTs have lifted consulting outlays by 35% since 2022, and Buy America clauses are compelling redesigns of supply chains, validation of domestic inputs, and extensive documentation, which add incremental fee layers for engineering consultants. Climate-resilience mandates embedded in funding guidelines are intensifying demand for risk-modeling, life-cycle cost analysis, and digital-twins that support asset hardening. These new compliance steps elongate schedules but expand revenue-per-project, expanding the U.S. engineering services market across all 50 states.

Accelerating Chip-Fab and Battery-Gigafactory Build-outs

Mega-fabs average USD 15-40 billion each, require ultra-pure utilities, class-10 to class-1 cleanrooms, and incorporate vibration isolation tolerances below two microns, driving premium bill rates that exceed traditional industrial projects by 20-30%. Intel's Ohio campus and TSMC's Arizona complex embed three-to-five-year engineering engagements, followed by long-term operations support contracts. Federal CHIPS incentives worth USD 52 billion de-risk these capital projects and underpin a multi-cycle orderbook for electrical, mechanical, process, and contamination-control specialists. Parallel battery-cell facilities from Tesla, GM, and Ford elevate opportunities in thermal-management, high-voltage design, and fire-suppression engineering, broadening total addressable revenues inside the U.S. engineering services market.

Volatile Steel and Concrete Input-Cost Pass-Through Risks

Steel prices fluctuated 25-40% annually during 2023-2025, while cement and ready-mix concrete rose 15-20%, squeezing project budgets and elevating risk of scope reduction. Fixed-price contracts thus expose firms to margin erosion and cause public-sector owners to delay bids, suppressing near-term billable hours in the U.S. engineering services market. Cost-plus agreements mitigate exposure yet face procurement hurdles. Escalation clauses and material indexes are gaining traction, but uncertainty still dampens CAPEX confidence, trimming the CAGR projection.

Other drivers and restraints analyzed in the detailed report include:

- Near-shoring of Manufacturing Lines to the U.S.

- Record-High Utility-Scale Solar and Wind Interconnection Queues

- Lengthy NEPA Environmental Reviews Delaying Starts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Civil engineering captured 34.88% of 2025 revenue, underscoring its pivotal role in the bridge rehabilitation, highway expansion, and resilient water systems funded by the IIJA. Projects such as California's high-speed rail and the Gateway Tunnel boosted demand for seismic retrofits, geotechnical modeling, and tunnel-boring oversight, ensuring a steady backlog that underpins the U.S. engineering services market. The segment benefits from increasing design-life requirements and climate-resilience standards that extend scoping phases and raise billable complexity.

Mechanical engineering is the fastest-advancing discipline due to semiconductor fabs, battery plants, and hyperscale data centers that require cleanroom HVAC, high-density thermal-management, and robotics integration. Electrical engineering demand is equally brisk, spurred by grid-modernization and EV charging corridors, pulling in relay-protection, medium-voltage design, and smart-meter analytics services. Environmental engineering has expanded beyond remediation into climate-risk modeling, carbon-capture systems, and ESG compliance, adding premium services that tack onto standard civil scopes. Chemical engineering remains a niche yet lucrative field for semiconductor etching processes, advanced pharmaceutical lines, and specialty materials, lifting average hourly rates across the U.S. engineering services market.

Consulting and design captured 17.76% of market revenue in 2025, driven by owners' desire for front-end expertise in BIM coordination, supply-chain localization, and resiliency planning. Digital-first delivery, including cloud-hosted common data environments and AI-assisted code checks, is reducing rework and shifting value upstream, reinforcing the segment's lead position in the U.S. engineering services market.

Process-and-plant engineering recorded outsized growth through mega-fab and gigafactory projects, where ultra-pure water, inert-gas systems, and robotic line-balancing demand deep specialty knowledge. Automation and digital-engineering services represent the highest CAGR outlook in the segment, linking sensor integration, edge analytics, and digital-twins that monetize post-commissioning optimization. Asset-management services are evolving into performance-based, data-subscription models that generate recurring cash flows, stabilizing top-line trajectories across the U.S. engineering services industry.

The United States Engineering Services Market Report is Segmented by Application (Civil, Mechanical, and More), Service Type (Consulting and Design, Process and Plant Engineering, and More), End-User Industry (Construction and Infrastructure, Oil and Gas, and More), Engagement Model (In-House, Outsourced / EPCM). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AECOM

- Jacobs Engineering Group

- Bechtel Corporation

- Fluor Corporation

- KBR Inc.

- HDR Inc.

- Terracon

- Black and Veatch

- Jensen Hughes

- ECS Group of Companies

- WSP USA

- Tetra Tech

- STV Group

- Arup (US)

- Gannett Fleming

- Burns and McDonnell

- HNTB Corporation

- Parsons Corporation

- Louis Berger (WSP)

- AtkinsRealis (U.S.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Infrastructure-Funding Boom under 2021 IIJA

- 4.2.2 Accelerating Chip Fabs and Battery Gigafactory Build-outs

- 4.2.3 Near-shoring of Manufacturing Lines to the U.S.

- 4.2.4 Record-High Utility-Scale Solar and Wind Interconnection Queues

- 4.2.5 Defense Modernization (AUKUS, NGAD) Driving Specialized Design

- 4.2.6 AI-Enabled Digital-Twin Adoption Cutting Re-work

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Concrete Input-Cost Pass-Through Risks

- 4.3.2 Lengthy NEPA Environmental Reviews Delaying Starts

- 4.3.3 Skilled-Labor Shortages Inflating Billing Rates

- 4.3.4 State-by-State Licensing Variances Hindering Scale

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Comparative Analysis: In-house vs Outsourced Engineering

- 4.8 Vendor Service Innovation Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Civil

- 5.1.2 Mechanical

- 5.1.3 Electrical

- 5.1.4 Environmental

- 5.1.5 Chemical

- 5.2 By Service Type

- 5.2.1 Consulting and Design

- 5.2.2 Process and Plant Engineering

- 5.2.3 Product Engineering and Prototyping

- 5.2.4 Automation / Digital Engineering

- 5.2.5 Asset Management and OandM

- 5.3 By End-user Industry

- 5.3.1 Construction and Infrastructure

- 5.3.2 Oil and Gas

- 5.3.3 Manufacturing

- 5.3.4 Utilities (Power, Water)

- 5.3.5 Transportation (Rail, Airports, Ports)

- 5.3.6 Telecommunications and Data Centers

- 5.3.7 Healthcare Facilities

- 5.4 By Engagement Model

- 5.4.1 In-house

- 5.4.2 Outsourced / EPCM

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 AECOM

- 6.4.2 Jacobs Engineering Group

- 6.4.3 Bechtel Corporation

- 6.4.4 Fluor Corporation

- 6.4.5 KBR Inc.

- 6.4.6 HDR Inc.

- 6.4.7 Terracon

- 6.4.8 Black and Veatch

- 6.4.9 Jensen Hughes

- 6.4.10 ECS Group of Companies

- 6.4.11 WSP USA

- 6.4.12 Tetra Tech

- 6.4.13 STV Group

- 6.4.14 Arup (US)

- 6.4.15 Gannett Fleming

- 6.4.16 Burns and McDonnell

- 6.4.17 HNTB Corporation

- 6.4.18 Parsons Corporation

- 6.4.19 Louis Berger (WSP)

- 6.4.20 AtkinsRealis (U.S.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment