PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940784

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940784

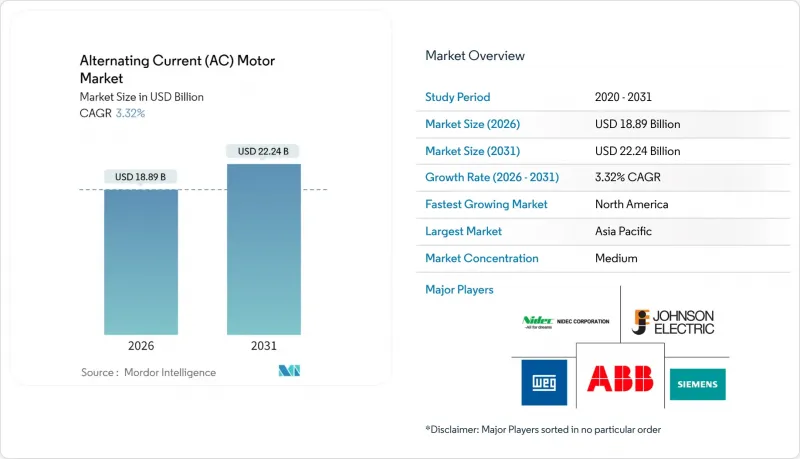

Alternating Current (AC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The alternating current motor market size in 2026 is estimated at USD 18.89 billion, growing from 2025 value of USD 18.29 billion with 2031 projections showing USD 22.24 billion, growing at 3.32% CAGR over 2026-2031.

This growth trajectory is shaped less by green-field capacity additions and more by efficiency-driven replacement cycles mandated by IE3 and IE4 regulations. Premium-efficiency design adoption is expanding across discrete manufacturing, renewable-energy, and HVAC segments, while automation programs in Asia and reshoring efforts in North America sustain baseline demand. Vendor strategies revolve around vertical integration in copper winding, electrical steel, and power electronics to buffer raw-material volatility and semiconductor shortages. Mature end-user sectors such as oil and gas continue to anchor revenues, yet faster growth is migrating toward water treatment, data centers, and wind-turbine auxiliaries, where lifetime energy savings justify premium pricing.

Global Alternating Current (AC) Motor Market Trends and Insights

Mandatory Energy-Efficiency Regulations Drive Premium Motor Adoption

IE3 has become the global compliance floor, and IE4 adoption is accelerating across Europe and the United States, effectively eliminating low-efficiency legacy models from procurement lists. Manufacturers are therefore retooling plants with automated lamination stamping and precision magnet-assembly lines to meet stricter loss limits. The shift burdens smaller regional firms that lack capital for new tooling, consolidating share with global incumbents. Procurement teams now evaluate motors on full-load efficiency at 75% and 50% duty points, which strengthens the value proposition of synchronous permanent-magnet designs. End-users capturing utility rebates for premium motors shorten payback periods to under two years, further reinforcing the regulatory push.

Industrial Automation Accelerates Mid-Range Motor Demand

Automotive, electronics, and logistics facilities are scaling collaborative robot fleets that rely on precision-controlled 1-100 kW motors. Servo-grade synchronous machines equipped with encoders deliver the sub-millimeter accuracy required in robotic welding, pick-and-place, and automated guided vehicles. Integrated drives and on-motor sensors enable torque-vector control, minimizing downtime. Regional incentives for smart factories in China, Japan, and Korea are pulling forward upgrade projects, while North American plants adopt similar architectures under reshoring schemes. Suppliers able to bundle drives, controllers, and analytics software capture premium margins.

Raw-Material Price Volatility Pressures Manufacturing Economics

Copper winding accounts for up to one-quarter of motor material cost, so London Metal Exchange price swings of 18% in 2024 drove quarterly margin compression among OEMs. Permanent-magnet grades of neodymium and dysprosium likewise spiked amid Chinese export policy uncertainty. Manufacturers adopted substitution tactics such as optimized slot fills, aluminum rotor cages, and ferrite-rich magnet compositions. Larger players hedge with multiyear supply contracts and proprietary magnet recycling programs.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Infrastructure Expands High-Power Motor Applications

- Commercial HVAC Modernization

- Premium Motor Cost Barriers in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Induction motors retained 69.12% share of the alternating current motor market in 2025 due to their rugged construction and low initial cost. Yet synchronous alternatives are projected at a 5.53% CAGR as permanent-magnet flux densities climb and controller prices fall. The alternating current motor market size for synchronous variants is therefore set to outpace replacements in the installed induction base.

Their premium efficiency appeals to energy-intensive plants, while built-in position feedback supports robotics and conveyor indexing. OEMs bundle synchronous machines with field-oriented drives that simplify commissioning. Although single-phase induction units remain dominant in residential air conditioners, multi-phase synchronous motors now permeate automotive paint shops and SMT lines. The alternating current motor market share gap between the two technologies is expected to narrow over the decade.

Low-voltage (<1 kV) machines delivered 60.88% revenue in 2025 across general manufacturing and HVAC. High-voltage (>11 kV) models, however, show the strongest 5.14% CAGR as wind farms and desalination plants demand multi-megawatt auxiliaries. The alternating current motor market size in high-voltage will therefore rise faster than the mid-voltage segment.

OEMs standardize compact stator slot designs to manage partial-discharge at high voltages, while epoxy-mica insulation systems extend lifetimes in damp offshore nacelles. Grid-code compliance further drives synchronous options with leading power-factor capability. EPC contractors in Brazil and Vietnam increasingly specify high-voltage motors to minimize current and cable losses across long cable runs, enlarging the alternating current motor market share for this class.

The Alternating Current (AC) Motor Market Report is Segmented by Motor Type (Induction AC Motors, and Synchronous AC Motors), Voltage Class (Low, Medium, and High Voltage), Power Rating (less Than 1 KW, 1-100 KW, 100-500 KW, and More), Efficiency Class (IE1-IE5), End-User Industry (Oil and Gas, Chemicals, Power Generation, Water Treatment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 44.10% of global revenue in 2025. China's high-tech manufacturing rebound spurred precision-motor imports, whereas India's renewable-energy rollout necessitated utility-scale drives for wind and solar assets. Southeast Asian countries such as Vietnam and Thailand are now localizing servo production lines, shrinking import lead times. Government subsidies covering up to 20% of premium-efficiency motor cost accelerate replacements in Korea and Japan.

South America is the fastest-growing region at 4.02% CAGR through 2031. Brazil channels National Development Bank funding toward industrial modernization, lifting orders for IE3-plus motors in petrochemical clusters. Argentina's RenovAr auctions foster wind-farm investment, triggering demand for >500 kW synchronous units. Currency volatility narrows capex windows, but OEMs with Mexican or Brazilian assembly plants hedge exchange-rate risks and secure volume contracts.

North America and Europe remain replacement-driven markets. U.S. reshoring incentives under the CHIPS and IRA acts stimulate greenfield factories requiring mid-range servo arrays. Canada's remote mining operations favor rugged high-power motors with ice-rated bearings. Europe's Ecodesign mandates drive IE4 upgrades across legacy plants. Scandinavian countries specify IE5 for district-heating pumps, while Germany's automotive sector integrates smart-motor plus drive packages, sustaining premium price points. Both regions compensate for slower unit growth with higher average selling prices, stabilizing alternating current motor market share among established brands.

- ABB Ltd.

- Siemens AG

- WEG Equipamentos Eletricos S.A.

- Nidec Corporation

- Johnson Electric Holdings Limited

- Yaskawa Electric Corporation

- Regal Rexnord Corporation

- Rockwell Automation, Inc.

- Franklin Electric Co., Inc.

- Bosch Rexroth AG

- Kirloskar Electric Company Ltd.

- SEVA-tec GmbH

- Toshiba Corporation

- Mitsubishi Electric Corporation

- TECO Electric & Machinery Co., Ltd.

- Leroy-Somer Holding (Nidec)

- ATB Austria Antriebstechnik AG

- Getriebebau NORD GmbH & Co. KG

- Oriental Motor Co., Ltd.

- Brook Crompton UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory energy-efficiency regulations (IE3/IE4)

- 4.2.2 Rapid industrial automation and robotics uptake

- 4.2.3 Expansion of renewable-energy assets (wind, solar)

- 4.2.4 HVAC/R build-out in commercial real estate

- 4.2.5 Rise of axial-flux PM AC motors in e-mobility

- 4.2.6 AI-enabled predictive-maintenance ecosystems

- 4.3 Market Restraints

- 4.3.1 Volatile copper and rare-earth metal prices

- 4.3.2 High upfront cost of premium-efficiency motors

- 4.3.3 Power-electronics (IGBT) supply-chain bottlenecks

- 4.3.4 End-of-life recycling and take-back compliance

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape and Standards

- 4.6 Technological Outlook (Edge and AI analytics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Induction AC Motors

- 5.1.1.1 Single-phase

- 5.1.1.2 Poly-phase

- 5.1.2 Synchronous AC Motors

- 5.1.2.1 DC-excited Rotor

- 5.1.2.2 Permanent-Magnet

- 5.1.2.3 Hysteresis

- 5.1.2.4 Reluctance

- 5.1.1 Induction AC Motors

- 5.2 By Voltage Class

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (>1-11 kV)

- 5.2.3 High Voltage (>11 kV)

- 5.3 By Power Rating

- 5.3.1 Less than 1 kW

- 5.3.2 1-100 kW

- 5.3.3 100-500 kW

- 5.3.4 Greater than 500 kW

- 5.4 By Efficiency Class

- 5.4.1 IE1 (Standard)

- 5.4.2 IE2 (High)

- 5.4.3 IE3 (Premium)

- 5.4.4 IE4 (Super-Premium)

- 5.4.5 IE5 (Ultra-Premium)

- 5.5 By End-user Industry

- 5.5.1 Oil and Gas

- 5.5.2 Chemicals and Petrochemicals

- 5.5.3 Power Generation

- 5.5.4 Water and Wastewater

- 5.5.5 Metals and Mining

- 5.5.6 Food and Beverage

- 5.5.7 Discrete Manufacturing

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Ranking Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 ABB Ltd.

- 6.5.2 Siemens AG

- 6.5.3 WEG Equipamentos Eletricos S.A.

- 6.5.4 Nidec Corporation

- 6.5.5 Johnson Electric Holdings Limited

- 6.5.6 Yaskawa Electric Corporation

- 6.5.7 Regal Rexnord Corporation

- 6.5.8 Rockwell Automation, Inc.

- 6.5.9 Franklin Electric Co., Inc.

- 6.5.10 Bosch Rexroth AG

- 6.5.11 Kirloskar Electric Company Ltd.

- 6.5.12 SEVA-tec GmbH

- 6.5.13 Toshiba Corporation

- 6.5.14 Mitsubishi Electric Corporation

- 6.5.15 TECO Electric & Machinery Co., Ltd.

- 6.5.16 Leroy-Somer Holding (Nidec)

- 6.5.17 ATB Austria Antriebstechnik AG

- 6.5.18 Getriebebau NORD GmbH & Co. KG

- 6.5.19 Oriental Motor Co., Ltd.

- 6.5.20 Brook Crompton UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment