PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940834

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940834

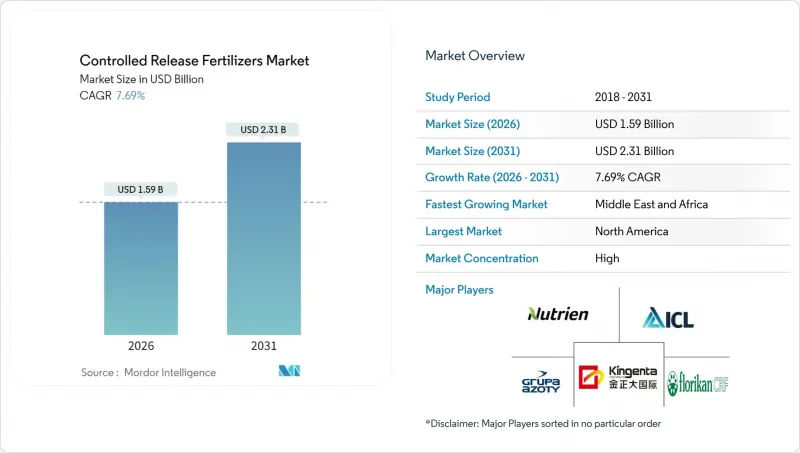

Controlled Release Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The controlled release fertilizers market size in 2026 is estimated at USD 1.59 billion, growing from 2025 value of USD 1.48 billion with 2031 projections showing USD 2.31 billion, growing at 7.69% CAGR over 2026-2031.

Adoption rides on precision nutrient management strategies that improve yield, curb nutrient loss, and align with tightening environmental regulations. Polymer-based coatings shape the technology landscape, while digital farming platforms create new value by linking real-time soil data with customized nutrient release schedules. Regional water scarcity pushes growers toward nutrient-efficient products, and government incentives accelerate uptake among large field-crop operations. Competitive intensity remains moderate, leaving room for innovators developing biodegradable coatings and data-driven decision tools.

Global Controlled Release Fertilizers Market Trends and Insights

Precision Agriculture Technology Integration

Variable-rate applicators now synchronize controlled release fertilizers with real-time soil nutrient maps, allowing growers to match coating thickness and release curves to micro-field conditions. Such orchestration reduces over- or under-fertilization events, boosts nutrient use efficiency, and extends product life cycles. Equipment makers bundle agronomic advisory and geospatial analytics, positioning controlled release fertilizers market participants in a broader digital ecosystem. Larger farms capture labor savings and environmental compliance credits, creating a reinforcing adoption loop that steadily expands the customer base.

Environmental Regulations and Sustainability Mandates Reshape Standards

Europe's Farm to Fork Strategy classifies controlled release products as preferred inputs for achieving nitrogen use-efficiency benchmarks above 80%. The 2024 biodegradability clause spurred a USD 200 million niche for coatings that safely decompose within 12-18 months, a trend now influencing labels in North America and emerging Asia. Compliance incentives, such as reduced buffer-zone requirements, lower the total cost of ownership relative to conventional fertilizers. Consequently, the controlled release fertilizers market is increasingly entwined with policy frameworks that reward measurable sustainability outcomes.

High Production Costs and Price Premium Barriers Constrain Penetration

Polymer-coated fertilizers typically sell at two to three times the price of conventional products, and coating resins track volatile petroleum input costs that swung 15-25% in 2024. Smallholders operating on tight margins hesitate to adopt even when lifetime savings appear favorable. Producers respond with localized blending plants to cut logistics costs and with pay-per-acre service models to alleviate upfront expenditure. These moves could soften the restraint once economies of scale mature.

Other drivers and restraints analyzed in the detailed report include:

- Water Scarcity and Irrigation Efficiency Requirements Accelerate Adoption

- Labor Cost Reduction and Application Convenience Transform Farm Operations

- Limited Farmer Awareness and Technical Knowledge Gaps Impede Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated products held 75.92% of the controlled release fertilizer market share in 2025 and contributed the bulk of the controlled release fertilizer market size growth, progressing at a 7.84% CAGR through 2031. Their popularity stems from precise nutrient-release kinetics that integrate seamlessly with variable-rate applicators. Continuous research is lowering coating thickness without compromising durability, improving cost ratios, and field performance. Biodegradable variants that decompose within 18 months now meet European Union standards, bringing new customer segments that formerly resisted polymer accumulation concerns.

Polymer-sulfur hybrids play a niche role where extended sulfur nutrition is critical, particularly in oilseed belts facing soil sulfur depletion. The combination lowers input counts by co-delivering macro- and secondary nutrients over synchronized timelines. Wax and resin coatings remain in value-oriented channels where tight budgets override the need for high-precision release. These categories together provide portfolio breadth that helps suppliers address diverse regional agronomic realities.

The Controlled Release Fertilizers Market Report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others), Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and Geography (Asia-Pacific, Europe, The Middle East and Africa, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

North America accounted for a 40.86% share of the controlled release fertilizers market in 2025, supported by advanced precision agriculture infrastructure and regulatory cost-share programs that subsidize nutrient-efficient inputs. In the United States, growers benefit from Environmental Protection Agency (EPA) watershed guidelines, which classify controlled release products as best-management practices eligible for compliance credits. In Canada, the Sustainable Agriculture Initiative allocated CAD 150 million (USD 111 million) to facilitate the conversion of conventional acres, accelerating adoption in prairie grain belts and horticultural clusters.

The Middle East and Africa markets are projected to grow at a fastest CAGR of 7.97% through 2031, driven by water scarcity, which increases interest in low-leach products. However, price sensitivity and limited advisory networks pose challenges to immediate volume growth. Latin America's large sugarcane and citrus holdings present emerging opportunities as regional distributors expand their portfolios by adding controlled release fertilizers lines.

The Asia-Pacific region is experiencing significant growth, driven by China's USD 2.3 billion precision agriculture stimulus and India's focus on nutrient-use efficiency to enhance national food security. Government initiatives in the region include bundling equipment loans, agronomist support, and discounts on controlled release fertilizers, which create demonstration plots to accelerate adoption. Europe's controlled release fertilizers market emphasizes compliance with the European Green Deal rather than volumetric expansion. Eco-scheme payments under the Common Agricultural Policy now reimburse up to 70% of incremental costs for proven nutrient-loss reductions, effectively offsetting the price premium for many arable farms.

- Ekompany International BV (DeltaChem)

- Grupa Azoty S.A. (Compo Expert)

- Haifa Group

- ICL Group Ltd

- Mivena BV

- Nutrien Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.

- New Mountain Capital (Florikan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision agriculture technology integration

- 4.5.2 Environmental regulations and sustainability mandates

- 4.5.3 Water scarcity and irrigation efficiency

- 4.5.4 Labor cost reduction and application convenience

- 4.5.5 Climate change adaptation and crop resilience

- 4.5.6 Food security and productivity optimization

- 4.6 Market Restraints

- 4.6.1 High production costs and price premium

- 4.6.2 Limited farmer awareness and technical gaps

- 4.6.3 Microparticle-shedding concerns triggering lobbying for coating traceability

- 4.6.4 Inflation-driven polymer cost spikes squeezing CRF producer margins

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 Bangladesh

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 Japan

- 5.3.1.7 Pakistan

- 5.3.1.8 Philippines

- 5.3.1.9 Thailand

- 5.3.1.10 Vietnam

- 5.3.1.11 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Netherlands

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 Ukraine

- 5.3.2.8 United Kingdom

- 5.3.2.9 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Nigeria

- 5.3.3.2 Saudi Arabia

- 5.3.3.3 South Africa

- 5.3.3.4 Turkey

- 5.3.3.5 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ekompany International BV (DeltaChem)

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 Mivena BV

- 6.4.6 Nutrien Ltd.

- 6.4.7 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.8 New Mountain Capital (Florikan)

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS