PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940871

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940871

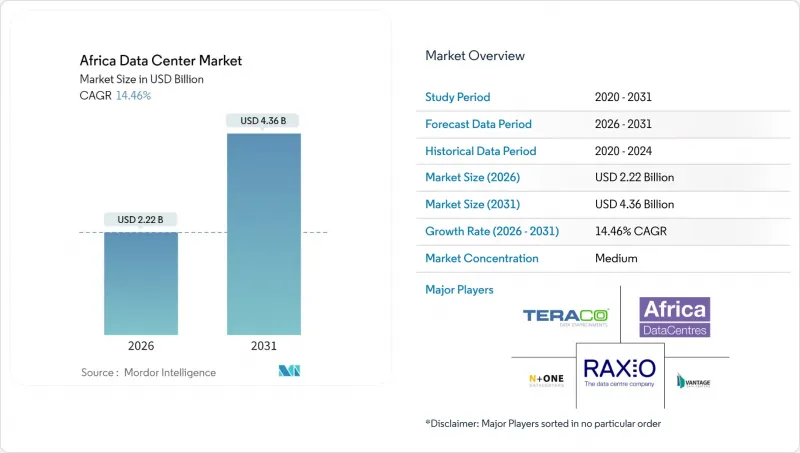

Africa Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Africa Data Center Market was valued at USD 1.94 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 4.36 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031).

In terms of IT load capacity, the market is expected to grow from 1.17 thousand megawatt in 2025 to 3.46 thousand megawatt by 2030, at a CAGR of 24.29% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. The surge reflects a strategic pivot by enterprises and governments toward sovereign hosting, backed by subsea cable additions, 5G rollouts, and assertive data-residency rules, all of which lower latency and improve compliance economics for early movers in the Africa data center market. The investment up-cycle accelerates because grid constraints, once a deterrent, now favor operators that can bundle renewable power and compliance expertise. Demand also benefits from cloud-first mandates, growing fintech ecosystems, and renewable-powered campuses that lower total cost of ownership. Competition centers on energy sourcing, skilled labor, and regulatory navigation rather than sheer floor space, driving mergers and partnerships that consolidate fragmented local capacity into region-spanning platforms across the Africa data center market.

Africa Data Center Market Trends and Insights

Spiralling Cloud-First Digital Transformation

Corporate cloud spending in Africa is growing 25-30% each year, forcing enterprises to blend international hyperscale capacity with local colocation for low-latency workloads. Government IT mandates that stipulate minimum local sourcing, such as Nigeria's 40% threshold, accelerate migrations from on-premise rooms to carrier-neutral facilities. Financial institutions process more than 60% of transactions via cloud-native cores, yet regulatory ceilings on offshore storage require compliant in-country infrastructure. This hybrid imperative elevates interconnection rich data centers that can knit public cloud nodes to enterprise cages without hair-pinning traffic through Europe or North America. The resulting demand spike benefits operators whose campuses incorporate dark fiber to multiple cloud on-ramps and who can offer audited data-protection controls sought by BFSI clients.

Government Data-Sovereignty Legislation

Nigeria's Data Protection Act 2023, South Africa's Protection of Personal Information Act, and Kenya's Data Protection Act collectively obligate sensitive data to remain within national borders. Multinationals categorised as Data Controllers of Major Importance must process personal records locally or risk penalties up to 2% of annual turnover, reshaping site-selection criteria from power price to legal compliance. Financial regulators stipulate that customer banking data reside domestically, guaranteeing a baseline load for Tier 3 and Tier 4 halls. Cross-border transfer restrictions fragment previously centralised architectures, compelling cloud providers to replicate zones across multiple African markets. Operators that can marshal legal, cybersecurity, and audit expertise alongside robust uptime become preferred partners as data-residency complexity deepens.

Chronic Grid Instability

Outside South Africa, grid reliability hovers below 60%, compelling facilities to size diesel plants for continuous rather than standby use. Nigerian sites budget diesel for weeks-long power gaps, elevating energy to 55-65% of operating expense compared with 35-45% in mature markets. Frequent genset cycling escalates maintenance and emissions, challenging sustainability narratives and limiting hyperscale commitment until renewables scale. South Africa's load-shedding schedule, although predictable, still obliges a 1:1 redundancy between grid and backup sources, doubling capital outlay for electrical infrastructure. Operators with captive solar, wind, or geothermal assets gain a structural cost edge as battery storage costs decline.

Other drivers and restraints analyzed in the detailed report include:

- Rapid 5G and National Backbone Fibre Projects

- Rising Subsea Cable Landings

- Limited Skilled Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large facilities commanded 30.92% of the Africa data center market size in 2025, evidencing customer preference for consolidated halls that streamline compliance audits and interconnection design. Economies of scale allow superior power usage efficiency, more fault-tolerant electrical topologies, and onsite renewable integration, lowering per-rack total cost of ownership. Enterprises facing stringent data-protection reviews prefer hosting critical workloads in campuses that can demonstrate ISO 27001 adherence and layered physical security, reducing due-diligence cycles. Moreover, capital availability from infrastructure funds enables large operators to pre-fit shells and delay internal build until anchor tenants sign, keeping utilisation aligned with demand spikes in the Africa data center market.

The growth trajectory remains steep, 24.12% CAGR, because greenfield megawatts under construction in Johannesburg, Lagos, and Nairobi pipeline directly into large-format halls. Medium-sized sites continue to appeal to regional enterprises that desire customised suites without megawatt-scale commitments. Small footprints, though still relevant for municipal e-government and branch office workloads, face upgrade pressure as regulations tighten uptime and security benchmarks. Massive and mega-scale builds, predominantly in South Africa, serve spill-over traffic from multinational cloud and content providers and act as landing pads for cross-continent interconnection fabrics.

Tier 3 halls made up 57.92% of the Africa data center market size in 2025, striking a pragmatic balance between redundancy and capital intensity. The 99.982% availability threshold satisfies most BFSI, telecom, and government procurement checklists while keeping project budgets within reach for local investors. Tier 3 certification also aligns with power-quality realities, as dual utility feeds or diverse substations remain impractical in many African metros. As a result, operators deploy N+1 topologies with modular power blocks that can evolve toward Tier 4 if grid resilience improves.

Tier 4 adoption is nevertheless accelerating at 24.05% CAGR, predominantly through hyperscale expansions that require concurrently maintainable systems and fault-tolerant electrical paths. Such facilities anchor regional cloud availability zones, attracting fintech and e-commerce platforms that need low-latency, in-country processing. Tier 1 and Tier 2 sites persist for content caching and disaster-recovery use cases but increasingly attract scrutiny from regulators, nudging owners to retrofit additional redundancy. The tier mix therefore mirrors a gradual up-shift in customer expectations as African digital economies mature.

The Africa Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Standard (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), End User Industry (BFSI, IT and ITES, E-Commerce, Media and Entertainment, and More), and Country (South Africa and More). The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Teraco Data Environments Proprietary Limited

- Medallion Communications Limited

- Africa Data Centers

- Paratus Group Holdings Limited

- Vantage Data Centers LLC

- Telecom Egypt

- Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- N+ONE Data Centers

- Open Access Data Centres Limited

- ONIX Data Centre Limited

- Icolo Data Centres Kenya Limited

- Interxion Holding N.V. (a Digital Realty company)

- Wana Corporate S.A. (INWI Business)

- Raxio Data Centre Holdings Pte. Ltd.

- MainOne Cable Company Limited (an Equinix company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of 5G and national backbone fibre projects

- 4.2.2 Spiralling cloud-first digital transformation among African enterprises

- 4.2.3 Rising subsea cable landings boosting international bandwidth supply

- 4.2.4 Government data-sovereignty legislation driving in-country hosting

- 4.2.5 Surging venture capital and infrastructure fund inflows into African data centers

- 4.2.6 Emergence of green hydrogen and renewable-powered campuses

- 4.3 Market Restraints

- 4.3.1 Chronic grid instability and reliance on diesel generators

- 4.3.2 Limited domestic skilled workforce for critical facility operations

- 4.3.3 High import tariffs and logistics costs for mission-critical equipment

- 4.3.4 Political and security risks in key growth corridors

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 South Africa

- 4.5.6.2 Israel

- 4.5.6.3 Nigeria

- 4.5.6.4 Rest of Africa

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MW)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Standard

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Israel

- 5.5.3 Nigeria

- 5.5.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Teraco Data Environments Proprietary Limited

- 6.4.2 Medallion Communications Limited

- 6.4.3 Africa Data Centers

- 6.4.4 Paratus Group Holdings Limited

- 6.4.5 Vantage Data Centers LLC

- 6.4.6 Telecom Egypt

- 6.4.7 Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- 6.4.8 N+ONE Data Centers

- 6.4.9 Open Access Data Centres Limited

- 6.4.10 ONIX Data Centre Limited

- 6.4.11 Icolo Data Centres Kenya Limited

- 6.4.12 Interxion Holding N.V. (a Digital Realty company)

- 6.4.13 Wana Corporate S.A. (INWI Business)

- 6.4.14 Raxio Data Centre Holdings Pte. Ltd.

- 6.4.15 MainOne Cable Company Limited (an Equinix company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment