PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940901

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940901

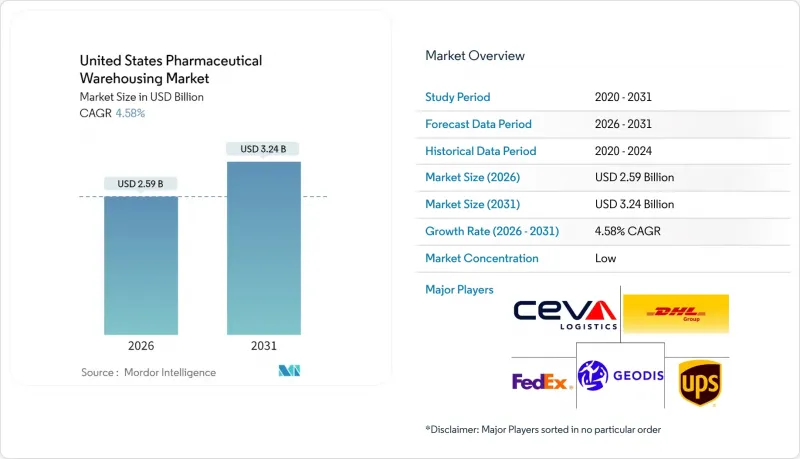

United States Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Pharmaceutical Warehousing Market is expected to grow from USD 2.48 billion in 2025 to USD 2.59 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 4.58% CAGR over 2026-2031.

Rising biologics output, full enforcement of the DSCSA serialization rule, and surging e-commerce fulfillment volumes are channeling new capital into temperature-controlled infrastructure and automation. Cell and gene therapy pipelines are adding ultra-low temperature requirements that lift revenue per square foot, while secure track-and-trace systems mandated by 21 CFR 211.142 are reshaping warehouse IT budgets. Cost headwinds energy, real estate and specialized labor remain pronounced, yet continuous investment in robotics, IoT sensors and green cold-chain designs is improving operating leverage. Intensifying consolidation among third-party logistics (3PL) leaders aims to capture higher-margin healthcare contracts and defend share against vertically integrating manufacturers and health-system operators.

United States Pharmaceutical Warehousing Market Trends and Insights

Robust Growth of U.S. Pharmaceutical Output

Annual capital spending of USD 160 billion in 2025 up 15% from 2024 couples every USD 1 billion invested with 2.3 million sq ft of extra warehouse need. Biologics represent 44% of new builds, prompting modular layouts that can flex with continuous-manufacturing schedules. FDA support for Advanced Manufacturing Technologies is accelerating real-time monitoring adoption, pushing facilities to embed redundant power and data systems. Decentralized production of cell therapies is spawning micro-warehouses near treatment centers, eroding the legacy hub-and-spoke network. These shifts collectively lift demand for secure, high-throughput storage nodes across the United States pharmaceutical warehousing market.

Expansion of Temperature-Controlled Storage Needs

Ultra-low requirements from mRNA vaccines (-80 °C) to cryogenic therapies (-196 °C) are now mainstream, raising energy use 20-30% above ambient operations rules under 21 CFR 600.15 mandate precise ranges, prompting IoT-enabled validations and alarm redundancies. Sustainability targets are spurring reusable shippers that cut fossil-fuel reliance 60%. Operators retrofit high-efficiency compressors and LED lighting to curb consumption, yet capital intensity remains a barrier for smaller entrants. Consequently, cold-chain capacity garners pricing power within the United States pharmaceutical warehousing market.

Stringent FDA cGMP & GDP Compliance Costs

Continuous temperature logging, electronic tracing and quarantine zones add 25% to 2025 compliance budgets. DSCSA serialization systems cost USD 0.5-2 million per facility, stretching small operators; 26% remain non-compliant post-stabilization. Penalties range from fines to criminal liability, accelerating consolidation. Documentation load drives demand for third-party specialists, yet shrinks margins for commodity storage. This regulatory burden dampens the growth curve of the United States pharmaceutical warehousing market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Biologics & Specialty-Drug Volumes

- Rapid B2B/B2C E-commerce Fulfillment Requirements

- Rising Energy and Real-Estate Costs for Cold Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Distribution and Inventory Management generated 45.32% of 2025 revenue, a testament to long-term contracts that stabilize cash flows within the United States pharmaceutical warehousing market. Value-added offerings-serialization, kitting and regulatory documentation-are scaling at a 5.72% CAGR as DSCSA enforcement tightens. Cloud-based WMS solutions now cover 90% of facilities, enhancing visibility and audit readiness.

Value-added services typically bill 25-40% above baseline rates, offsetting compliance overhead. Robotics-as-a-Service models lower entry barriers for mid-tier operators, supporting market fragmentation while bolstering efficiency. FDA 21 CFR 205.50 stipulates secure storage and handling, favoring providers that can turnkey compliance at scale. These dynamics reinforce storage as the anchor while upgrading service complexity across the United States pharmaceutical warehousing market.

Non-cold-chain sites still constitute 58.05% of the United States pharmaceutical warehousing market size, but cold-chain capacity is outpacing at a 6.01% CAGR through 2031. Chilled, frozen and ultra-low zones command rates 150-200% higher than ambient alternatives, compensating for energy drain.

Operators retrofit ambient structures with modular cool chambers to balance flexibility and capex. IoT sensors cut temperature excursion risk 60%, curbing USD 35 billion annual losses industry-wide temperature mandates create high compliance hurdles, shielding incumbents. As biologics pipelines swell, cold-chain share will progressively rise within the United States pharmaceutical warehousing market.

The United States Pharmaceutical Warehousing Market Report is Segmented by Service Type (Storage, Distribution and Inventory Management, and More), Warehouse Type (Cold-Chain Warehouse, Non-Cold-Chain Warehouse), Product Type (Prescription Drugs, and More), End User (Pharmaceutical Manufacturers, Healthcare Providers, Retail & Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service Inc.

- DHL Group

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Lineage Logistics

- Americold Logistics

- Cencora

- BioPharma Logistics

- Rhenus SE & Co. KG

- Kuehne + Nagel

- XPO Logistics

- KRC Logistics

- GXO Logistics

- MD Logistics

- Langham Logistics

- Crown LSP Group

- LifeScience Logistics

- Go Freight

- DSV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth of U.S. pharmaceutical output

- 4.2.2 Expansion of temperature-controlled (2-8 °C) storage needs

- 4.2.3 Surge in biologics and specialty-drug volumes

- 4.2.4 Rapid B2B/B2C e-commerce fulfillment requirements

- 4.2.5 DSCSA serialization deadline boosting secure warehousing

- 4.2.6 Urban micro-fulfillment hubs near key metros

- 4.3 Market Restraints

- 4.3.1 Stringent FDA cGMP and GDP compliance costs

- 4.3.2 Rising energy and real-estate costs for cold storage

- 4.3.3 Skilled-labor shortages in high-tech warehouses

- 4.3.4 Escalating cybersecurity / data-integrity risks (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (FDA, DSCSA, DEA, OSHA)

- 4.6 Technological Outlook (WMS, IoT, Automation, Robotics)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics and Pandemic on Warehousing

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.2 By Warehouse Type

- 5.2.1 Cold-Chain Warehouse

- 5.2.1.1 Chilled (0-5°C)

- 5.2.1.2 Frozen (-18-0°C)

- 5.2.1.3 Ambient

- 5.2.1.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.2.2 Non-Cold-Chain Warehouse

- 5.2.1 Cold-Chain Warehouse

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Specialty Medicine (non-biologic)

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Healthcare Providers

- 5.4.3 Retail and Pharmacies

- 5.4.4 Distributors and Wholesalers

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 United Parcel Service Inc.

- 6.4.2 DHL Group

- 6.4.3 FedEx Corp.

- 6.4.4 GEODIS SA

- 6.4.5 CEVA Logistics

- 6.4.6 Lineage Logistics

- 6.4.7 Americold Logistics

- 6.4.8 Cencora

- 6.4.9 BioPharma Logistics

- 6.4.10 Rhenus SE & Co. KG

- 6.4.11 Kuehne + Nagel

- 6.4.12 XPO Logistics

- 6.4.13 KRC Logistics

- 6.4.14 GXO Logistics

- 6.4.15 MD Logistics

- 6.4.16 Langham Logistics

- 6.4.17 Crown LSP Group

- 6.4.18 LifeScience Logistics

- 6.4.19 Go Freight

- 6.4.20 DSV

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment