PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034967

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034967

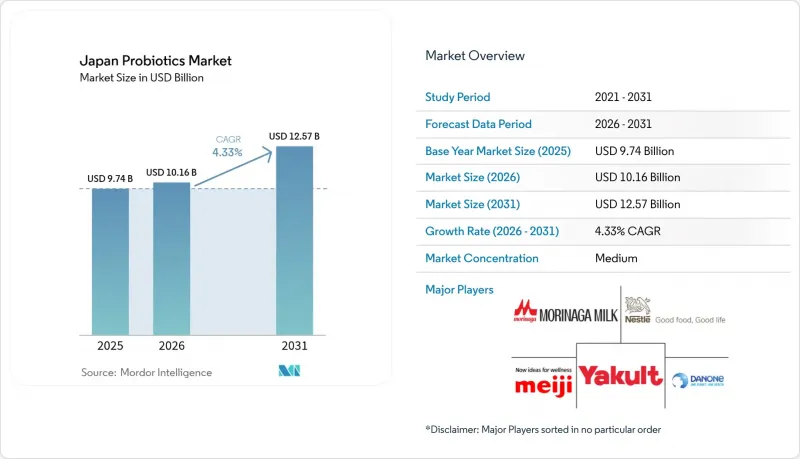

Japan Probiotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan probiotics market size was valued at USD 9.74 billion in 2025 and estimated to grow from USD 10.16 billion in 2026 to reach USD 12.57 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

A super-aged population, faster Foods with Function Claims (FFC) approvals, and broad cultural acceptance of fermented foods are steering demand toward daily gut and immune maintenance. Supermarkets still anchor volume, yet online retail subscriptions and vending machine launches are broadening their reach to younger, mobile consumers. Scale players are bolstering factory capacity, direct-to-consumer networks, and proprietary strains to protect share while smaller entrants find room in postbiotic niches. Rising compliance costs following the 2025 FFC labeling proposal and the 2024 Beni-koji recall favor manufacturers that can document strain traceability, clinical validation, and adherence to Good Manufacturing Practice.

Japan Probiotics Market Trends and Insights

Age-driven focus on preventive gut and immune health

Nearly 29.3% of Japan's residents are now aged 65 or older, prompting a shift in policy from treating illness to preventing it through a balanced diet. The Health Japan 21 program encourages a higher intake of dietary fiber and fermented products, incorporating probiotics into government-endorsed lifestyle guidance. Yakult's capacity expansion added 2.85 million bottles per day in January 2024 to supply contracts with municipal health centers that distribute probiotic drinks to seniors. Meiji followed in October 2025 with the world's first HbA1c-lowering yogurt, targeting 10 million pre-diabetic adults and underscoring that probiotics are moving closer to clinical nutrition. Physicians now prescribe functional foods identified during mandatory Specific Health Checkups, pushing the Japan probiotics market deeper into the healthcare continuum.

Expansion of FFC/FOSHU health-claim approvals

The Foods with Function Claims (FFC) system, launched in 2015, overtook FOSHU in market value by 2020, reaching JPY 546 billion (USD 3.6 billion) by 2022 with 1,412 product registrations in its first three years, allowing manufacturers to self-certify using existing literature and cut time-to-market from 24 months to 60 days. This fueled condition-specific probiotic products like Kirin's iMUSE line, which earned JPY 20 billion (USD 133 million) in 2024 across 59 products from 16 partners without costly clinical trials. Regulatory tightening looms with the Consumer Affairs Agency's 2025 Proposal 235080082 on adverse-event reporting and labeling, while the 2024 Beni-koji contamination accelerated GMP adoption, raising costs for new entrants. Domestic FFC validation is also enabling exports, as seen with Morinaga's July 2024 M-63 strain registration in China.

Strain stability and shelf-life challenges

Maintaining viable probiotic cell counts through manufacturing, distribution, and retail remains a technical bottleneck, with studies showing losses of 0.02-0.13 log CFU per day under typical conditions. Yakult's 5.5-day and Activia's 11.3-day distribution dwell times require initial counts of 7.5-9.0 log CFU/g, which raises costs and limits formulation flexibility. Additionally, temperature excursions, especially in humid Japanese summers, further threaten viability. Morinaga's bifidobacteria powder technology stabilizes strains for ambient distribution but demands expensive spray-drying infrastructure. Postbiotics, such as Kirin's LC-Plasma and Asahi's CP2305, avoid viability issues but sacrifice the live-microbe narrative. The lack of standardized viability testing regulations adds compliance uncertainty, complicating cross-border trade and eroding consumer trust.

Other drivers and restraints analyzed in the detailed report include:

- Rising health consciousness among consumers

- Strong cultural acceptance of fermented foods

- Limited consumer awareness of advanced probiotic strains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, functional food and beverages captured 61.85% of the Japan probiotics market share, a testament to the national preference for health benefits delivered through everyday meals. Supplements, growing at a 6.35% CAGR to 2031, reflect consumer appetite for precise dosing and physician-advised interventions. Yakult's plant-based factory, opened in October 2024, expands the functional beverage appeal to lactose-intolerant and vegan shoppers. Meiji's SAVAS Milk Protein yogurt layers sports nutrition onto fermented dairy, proving that hybrid products can defend the dominant food format from supplement encroachment. Still, premium capsules like Otsuka's equol-producing Lactococcus 20-92 command pharmacy pricing that functional foods rarely achieve, illustrating a bifurcated value pool within the Japanese probiotics market size.

Second-generation formats are reshaping each side of the ledger. Postbiotic teas and probiotic chocolates allow for ambient shelving, unlocking vending machines and confection aisles that were once off-limits to chilled yogurt. Meanwhile, clinical-strength HbA1c-lowering yogurts and bone-density ice creams blur boundaries between meal and medicine, expanding what consumers accept as "food." These continuous format innovations reinforce the perception that the Japan probiotics market is less a static category and more a technology platform for condition-specific nutrition.

The Japan Probiotics Market Report is Segmented by Type (Functional Food and Beverage, Dietary Supplements, Animal Feed, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Other Distribution Channel). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Yakult Honsha Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- Meiji Co., Ltd.

- Megmilk Snow Brand Co., Ltd.

- Asahi Group Holdings (Calpis brand)

- Kirin Holdings Co., Ltd.

- Nissin Foods Holdings Co., Ltd.

- Groupe Danone SA

- Nestle S.A.

- Otsuka Pharmaceutical Co., Ltd.

- Shiseido Co., Ltd. (Inner Beauty)

- Amway Japan GK

- NOW Health Group

- General Mills Inc.

- BioGaia AB

- Probi AB

- Glac Biotech Co., Ltd.

- Lifeway Foods, Inc.

- DHC Corporation

- Nihon Kefia Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Age-driven focus on preventive gut and immune health

- 4.2.2 Expansion of FFC/FOSHU health-claim approvals

- 4.2.3 Rising health consciousness among consumers

- 4.2.4 Strong cultural acceptance of fermented foods

- 4.2.5 Expansion of functional and fortified food categories

- 4.2.6 Innovations in probiotic strains tailored to Japanese consumers

- 4.3 Market Restraints

- 4.3.1 Strain Stability and shelf-life challenges

- 4.3.2 Limited consumer awareness of advanced probiotic strains

- 4.3.3 Shelf-life and cold-chain cost pressures

- 4.3.4 Strict regulatory compliance for health claims

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape (FFC/FOSHU/FNFC)

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Functional Food and Beverage

- 5.1.2 Dietary Supplements

- 5.1.3 Animal Feed

- 5.1.4 Others

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Specialty Stores (Pharmacies/Health Stores)

- 5.2.4 Online Retail

- 5.2.5 Other Distribution Channel

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Yakult Honsha Co., Ltd.

- 6.4.2 Morinaga Milk Industry Co., Ltd.

- 6.4.3 Meiji Co., Ltd.

- 6.4.4 Megmilk Snow Brand Co., Ltd.

- 6.4.5 Asahi Group Holdings (Calpis brand)

- 6.4.6 Kirin Holdings Co., Ltd.

- 6.4.7 Nissin Foods Holdings Co., Ltd.

- 6.4.8 Groupe Danone SA

- 6.4.9 Nestle S.A.

- 6.4.10 Otsuka Pharmaceutical Co., Ltd.

- 6.4.11 Shiseido Co., Ltd. (Inner Beauty)

- 6.4.12 Amway Japan GK

- 6.4.13 NOW Health Group

- 6.4.14 General Mills Inc.

- 6.4.15 BioGaia AB

- 6.4.16 Probi AB

- 6.4.17 Glac Biotech Co., Ltd.

- 6.4.18 Lifeway Foods, Inc.

- 6.4.19 DHC Corporation

- 6.4.20 Nihon Kefia Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS