PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034968

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034968

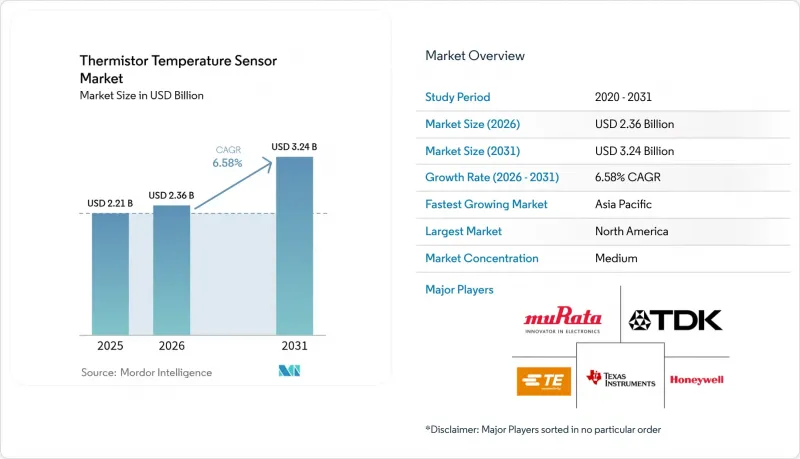

Thermistor Temperature Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The thermistor temperature sensor market size is expected to grow from USD 2.21 billion in 2025 to USD 2.36 billion in 2026 and is forecast to reach USD 3.24 billion by 2031 at 6.58% CAGR over 2026-2031.

Demand accelerates as high-density battery packs, ultra-low-power IoT nodes, and smart consumer devices all require millisecond-level thermal feedback. Dense monitoring arrays inside electric-vehicle battery modules, large-scale sensor rollouts across industrial IoT lines, and regulatory mandates for food and pharmaceutical cold chains form the core volume drivers. Cost-effective NTC devices control 70% of global shipments, while PTC variants carve out niches where self-regulation adds value. Regionally, Asia-Pacific's manufacturing depth anchors 46% of total 2024 revenue, yet the Middle East delivers the fastest regional upswing. Competitive positioning now hinges on the ability to bundle sensing elements with on-board signal processing and connectivity so that customers secure turnkey thermal-management subsystems rather than discrete components.

Global Thermistor Temperature Sensor Market Trends and Insights

Demand for Cost-Effective, High-Accuracy Sensors in Consumer Electronics

Thermistors are winning socket share in smartphones, laptops, and wearables because chip-scale 0402 packages occupy minimal board real estate while still achieving +-0.5 °C accuracy. Device makers now embed multi-point thermistor arrays across batteries and system-on-chip heat spreaders to trigger predictive throttling algorithms that lengthen component life and improve user safety. Continuous shrinkage of application processors lifts waste-heat density, so every new smartphone generation adds incremental thermal nodes. The result is a steady rise in the thermistor temperature sensor market as OEMs favor the low cost and mature supply chains of NTC parts over digital IC alternatives. Suppliers that combine ultra-small die with low-noise signal chains are carving out premium ASP positions despite the commodity reputation of discrete thermistors.

Rapid EV-Battery Deployment Requiring Dense Thermal-Runaway Monitoring

Modern battery packs mount hundreds of sensing beads per vehicle because a 5 °C cell-to-cell gradient can cascade into runaway failures. NTC materials deliver sub-100 millisecond response across -40 °C to 125 °C ranges, allowing battery-management units to isolate overheating modules before venting occurs. Second-generation chemistries such as high-nickel NMC require even tighter temperature envelopes, enlarging sensor counts per kilowatt-hour. Automakers have therefore become the largest volume buyers in the thermistor temperature sensor market. To meet stringent AEC-Q200 reliability tests, vendors are introducing epoxy-coated leads that resist vibration, humidity, and electromagnetic interference, ensuring long-term calibration stability over the vehicle's service life.

Limited Temperature Span Versus RTDs and IC Sensors

Most NTC formulations top out near 125 °C, which rules them out for aerospace turbines, petrochemical reactors, and engine-exhaust systems that run beyond 200 °C. End users in these sectors prefer platinum RTDs or digital silicon ICs that remain stable at elevated ranges and provide linear outputs without analog conditioning. The resulting application ceiling trims the obtainable share of the thermistor temperature sensor market in extreme-temperature verticals. Component makers are pursuing high-temperature glass-encapsulated beads, but production yields remain low and costs high, limiting near-term adoption.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Industrial IoT and Smart Factories

- Regulatory Mandates on Food Safety and Cold-Chain Traceability

- Volatility in Manganese, Cobalt, and Nickel-Oxide Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

NTC devices captured 69.62% of the 2025 volume, establishing clear leadership in the thermistor temperature sensor market share thanks to exponential resistance-temperature slopes that resolve 0.01 °C changes in medical, battery, and industrial control loops. The thermistor temperature sensor market size contribution from NTC parts is forecast to grow from USD 1.54 billion in 2025 to USD 2.22 billion by 2031, reflecting the segment's ability to scale into chip-scale, probe, and flexible-substrate formats. PTC products, while rising at a 7.38% CAGR, remain niche for inrush current limiting and self-heating heaters.

The evolution of perovskite-doped ceramics is amplifying beta coefficients above 4,400 K, further tightening accuracy without complex linearization. Vendors also deposit thin-film NTC layers on polyimide and PET, giving designers stretchable sensors for e-textile garments. This steady innovation cadence underpins long-term NTC dominance even as digital ICs nibble at legacy sockets, ensuring the thermistor temperature sensor market retains a robust core around high-sensitivity discrete components.

The Thermistor Temperature Sensor Market Report is Segmented by Type (Positive Temperature Coefficient (PTC), Negative Temperature Coefficient (NTC)), Temperature Range (Low Temperature (Below -40 C), Medium Temperature (-40 C To 125 C) and More), End-Use Industry (Automotive, Consumer Electronics, Industrial, Medical, Energy, Aerospace, HVAC), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 46.08% share in 2025 stems from its vertically integrated ceramic processing and surface-mount assembly hubs concentrated in China, Japan, and South Korea. Tier-one suppliers operate large-scale kilns near component plants, cutting logistics costs and shortening lead times. Government incentives for EV adoption amplify local demand, while regional giant battery makers source sensors from domestic vendors to comply with tight pack-level thermal budgets.

North America and Europe combine for roughly 34.75% of 2025 revenue. Their advantage lies in high-margin medical, aerospace, and ADAS markets that prize traceability and functional-safety certification. Automotive Tier-1s in Germany and the United States have begun qualifying combined temperature-voltage probes that simplify wiring inside 800-V battery architectures, a trend expected to lift average selling prices even if unit counts plateau.

The Middle East tops growth tables at 6.98% CAGR as giga-factories, smart-city programs, and energy-intensive desalination plants demand thousands of sensors per facility. Africa and South America remain nascent, but mining, agriculture, and renewables create early footholds. Export-oriented Asian vendors are partnering with local distributors to bridge support gaps and capture incremental share in these frontier regions, further broadening the thermistor temperature sensor market.

- Texas Instruments Inc.

- Murata Manufacturing Co. Ltd.

- TDK Corporation (EPCOS)

- TE Connectivity

- Honeywell International Inc.

- Panasonic Corp.

- Vishay Intertechnology Inc.

- Mitsubishi Materials Corp.

- Shibaura Electronics Co. Ltd.

- Littelfuse Inc. (Ametherm)

- SEMITEC Corp.

- KOA Corporation

- Ohizumi Manufacturing Co. Ltd.

- Molex LLC

- Analog Devices Inc.

- Amphenol Advanced Sensors

- Sensata Technologies

- Heraeus Nexensos

- Vishay BC Components

- AVX Corp. (KYOCERA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for cost-effective, high-accuracy sensors in consumer electronics

- 4.2.2 Rapid EV-battery deployment requiring dense thermal-runaway monitoring

- 4.2.3 Expansion of industrial IoT and smart factories

- 4.2.4 Regulatory mandates on food-safety and cold-chain traceability

- 4.2.5 Solid-state battery early-warning chips integrating micro-NTC beads

- 4.2.6 Smart-textile wearables embedding flexible thermistor yarns

- 4.3 Market Restraints

- 4.3.1 Limited temperature span versus RTDs and IC sensors

- 4.3.2 Volatility in manganese, cobalt, and nickel-oxide feedstock prices

- 4.3.3 Shift toward fully-digital temperature-sensor ICs in automotive ADAS

- 4.3.4 Self-heating drift in ultra-low-power IoT nodes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Positive Temperature Coefficient (PTC)

- 5.1.2 Negative Temperature Coefficient (NTC)

- 5.2 By Temperature Range

- 5.2.1 Low Temperature (Below -40 C)

- 5.2.2 Medium Temperature (-40 C to 125 C)

- 5.2.3 High Temperature (Above 125 C)

- 5.3 By End-Use Industry

- 5.3.1 Automotive and E-Mobility

- 5.3.2 Consumer Electronics and Wearables

- 5.3.3 Industrial Automation and IIoT

- 5.3.4 Medical and Life-Sciences Equipment

- 5.3.5 Energy and Power Generation

- 5.3.6 Aerospace and Defense

- 5.3.7 HVAC and Building Automation

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Singapore

- 5.4.4.7 Malaysia

- 5.4.4.8 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Murata Manufacturing Co. Ltd.

- 6.4.3 TDK Corporation (EPCOS)

- 6.4.4 TE Connectivity

- 6.4.5 Honeywell International Inc.

- 6.4.6 Panasonic Corp.

- 6.4.7 Vishay Intertechnology Inc.

- 6.4.8 Mitsubishi Materials Corp.

- 6.4.9 Shibaura Electronics Co. Ltd.

- 6.4.10 Littelfuse Inc. (Ametherm)

- 6.4.11 SEMITEC Corp.

- 6.4.12 KOA Corporation

- 6.4.13 Ohizumi Manufacturing Co. Ltd.

- 6.4.14 Molex LLC

- 6.4.15 Analog Devices Inc.

- 6.4.16 Amphenol Advanced Sensors

- 6.4.17 Sensata Technologies

- 6.4.18 Heraeus Nexensos

- 6.4.19 Vishay BC Components

- 6.4.20 AVX Corp. (KYOCERA)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment