PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034972

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034972

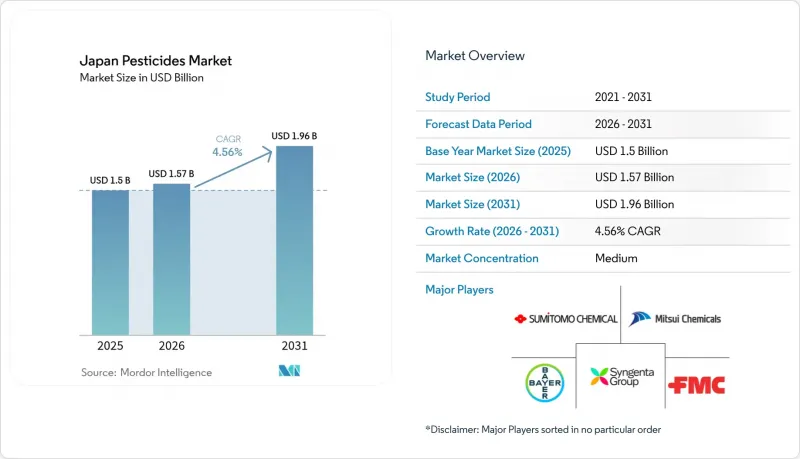

Japan Pesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan pesticides market size is expected to grow from USD 1.5 billion in 2025 to USD 1.57 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 4.56% CAGR over 2026-2031.

This projection highlights the steady transition of a mature farming sector toward data-driven, low-residue solutions, precision delivery systems, and increased deployment of biologically active ingredients. Behind the headline CAGR lies a confluence of drivers: government incentives that reward pesticide-risk reduction, climate variability that elevates pest pressure, a rapidly aging farming population that embraces labor-saving technologies, and continuous innovation in microencapsulation and drone-ready formulations. Competitive strategies are shifting toward portfolio diversification and cross-border expansion as local demand plateaus, while supply-chain resilience has become a boardroom priority after ingredient shortages exposed dependencies on imported raw materials.

Japan Pesticides Market Trends and Insights

Government initiatives and policies for Sustainable Food

Japan's MIDORI Strategy mandates a 50% reduction in risk-weighted chemical pesticide use by 2050 and allocates JPY 2.2683 trillion (USD 15.1 billion) for subsidizing farmers who halve synthetic applications. The combination of direct payments, expedited approvals for low-dose actives, and labeling incentives is pushing the Japan pesticides market toward higher efficacy per hectare and wider use of biocontrol agents. Suppliers that align portfolios with these guidelines are securing preferential registration, while export-oriented firms leverage Japan's elevated standards to differentiate in international markets. The policy pressure also accelerates research into micro-dosed formulations that maintain yield while satisfying residue targets, a focal point for domestic innovators.

Rising pest pressure driven by climate volatility

Weather volatility is intensifying migrant pest influx, notably the brown planthopper that now reaches Kyushu under favorable wind currents more frequently. The phenomenon compresses spray windows and forces farmers to adopt broad-spectrum or sequential applications, strengthening demand within the Japan pesticides market. High-resolution S-18 climate modelling data enable region-tailored product positioning, while manufacturers incorporate predictive pest analytics into advisory platforms to secure growers' loyalty.

Stringent registration and MRL compliance timelines

The Ministry of Health, Labour and Welfare cut cabbage methomyl residue limits from 0.7 mg/kg to 0.5 mg/kg, and 141 new substances entered regulatory scrutiny in 2024. These shifts raise toxicology study costs, delay product launches, and weigh on smaller registrants in the Japan pesticides market. Companies respond by pooling data across global subsidiaries and prioritizing dual-use chemistries designed for Japan and European Union alignment to amortize dossiers.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated adoption of labor-saving herbicides by aging farmers

- Growth of protected horticulture complexes boosting fungicide demand

- Heightened consumer scrutiny of chemical residues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic-based pesticides retained a 70.40% grip on the Japan pesticides market share in 2025 due to proven efficacy, ease of storage, and broad-spectrum performance valued by aging growers. Bio-based products are climbing at a 8.75% CAGR on the back of regulatory accelerators and consumer pull. Farmers cutting synthetic volume by 50% unlock direct payment eligibility, reinforcing the appeal of biological alternatives. At the same time, multinationals are licensing microbial actives from local startups to hedge against synthetic dependency.

The bio-based pesticides foster co-formulations that blend low-dose chemistry with living organisms, delivering robust control at reduced toxic-load indices. This hybrid strategy positions suppliers to satisfy MIDORI targets without compromising yield. Regulatory frameworks under MAFF's Strategy for Sustainable Food Systems provide preferential treatment for biological products, including expedited registration processes and financial incentives that are reshaping competitive dynamics between synthetic and bio-based segments.

Herbicides secured 44.95% of sales in 2025 as mechanization-averse rice farmers adopted single-shot weed knockdown products. Yet herbicide resistance is a mounting risk that propels miticide and fungicide innovation. Miticides are accelerating at 8.36% CAGR, fueled by spider-mite outbreaks in greenhouse tomatoes and cucumbers. Fungicides maintain steady demand through greenhouse cultivation expansion, while insecticides face pressure from integrated pest management adoption and biological control alternatives. Nematicides represent a specialized segment serving high-value crops and protected cultivation systems requiring soil-borne pest control.

The herbicide segment confronts escalating resistance challenges, with multiple weed species, including Taiwan barnyardgrass, developing resistance to Groups 1 and 2 herbicides, necessitating rotation strategies and novel active ingredients. Kumiai Chemical's pyroxasulfone herbicide demonstrated 26% compound annual growth from 2013 to 2023, indicating market appetite for effective new chemistries. The National Agriculture and Food Research Organization's development of systematic herbicide control methods for invasive species demonstrates ongoing innovation in application techniques and resistance management strategies.

The Japan Pesticides Market Report is Segmented by Origin (Synthetic, and Bio-Based), Type (Herbicide, Fungicide, Insecticide, Miticide, and More), Formulation (Liquid Concentrates, Wettable Powders, and More), Crop Type (Grains and Cereals, Pulses and Oilseeds, and More), and Application (Foliar Spray, Soil Treatment, Seed Treatment, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sumitomo Chemical Co., Ltd.

- Syngenta CropProtection AG (Syngenta Group)

- Bayer AG

- Mitsui Chemicals Agro, Inc. (Mitsui Chemicals, Inc.)

- BASF SE

- FMC Corporation

- Nissan Chemical Corporation

- Nihon Nohyaku Co., Ltd (ADEKA Corporation)

- Kumiai Chemical Industry Co., Ltd

- UPL Limited

- OAT Agrio Co., Ltd

- Corteva Agriscience

- Hokko Chemical Industry Co., Ltd

- Nippon Soda Co., Ltd

- Ishihara Sangyo Kaisha, Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government initiatives and policies for Sustainable Food

- 4.2.2 Rising pest pressure driven by climate volatility

- 4.2.3 Accelerated adoption of labor-saving herbicides by aging farmers

- 4.2.4 Rapid uptake of bio-based pesticides

- 4.2.5 Expansion of drone-enabled precision spraying

- 4.2.6 Growth of protected horticulture complexes boosting fungicide demand

- 4.3 Market Restraints

- 4.3.1 Stringent registration and MRL compliance timelines

- 4.3.2 Heightened consumer scrutiny of chemical residues

- 4.3.3 Escalating herbicide-resistant weed populations

- 4.3.4 Intermittent shortages of critical formulation additives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook in Application and Formulation

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Origin

- 5.1.1 Synthetic

- 5.1.2 Bio-based

- 5.2 By Type

- 5.2.1 Herbicide

- 5.2.2 Fungicide

- 5.2.3 Insecticide

- 5.2.4 Miticide

- 5.2.5 Nematicide

- 5.2.6 Other Types (Rodenticide, Bactericide, etc.)

- 5.3 By Formulation

- 5.3.1 Liquid Concentrates

- 5.3.2 Wettable Powders

- 5.3.3 Granules

- 5.3.4 Microencapsulated

- 5.3.5 Suspension Concentrates

- 5.4 By Crop type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Fruits and Vegetables

- 5.4.4 Commercial Crops

- 5.4.5 Ornamental Crops

- 5.4.6 Other Applications (Turfgrass Management, Forestry Seedlings, etc.)

- 5.5 By Application

- 5.5.1 Foliar Spray

- 5.5.2 Soil Treatment

- 5.5.3 Seed Treatment

- 5.5.4 Chemigation

- 5.5.5 Aerial / Drone Application

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Sumitomo Chemical Co., Ltd.

- 6.4.2 Syngenta CropProtection AG (Syngenta Group)

- 6.4.3 Bayer AG

- 6.4.4 Mitsui Chemicals Agro, Inc. (Mitsui Chemicals, Inc.)

- 6.4.5 BASF SE

- 6.4.6 FMC Corporation

- 6.4.7 Nissan Chemical Corporation

- 6.4.8 Nihon Nohyaku Co., Ltd (ADEKA Corporation)

- 6.4.9 Kumiai Chemical Industry Co., Ltd

- 6.4.10 UPL Limited

- 6.4.11 OAT Agrio Co., Ltd

- 6.4.12 Corteva Agriscience

- 6.4.13 Hokko Chemical Industry Co., Ltd

- 6.4.14 Nippon Soda Co., Ltd

- 6.4.15 Ishihara Sangyo Kaisha, Ltd

7 Market Opportunities and Future Outlook