PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034976

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034976

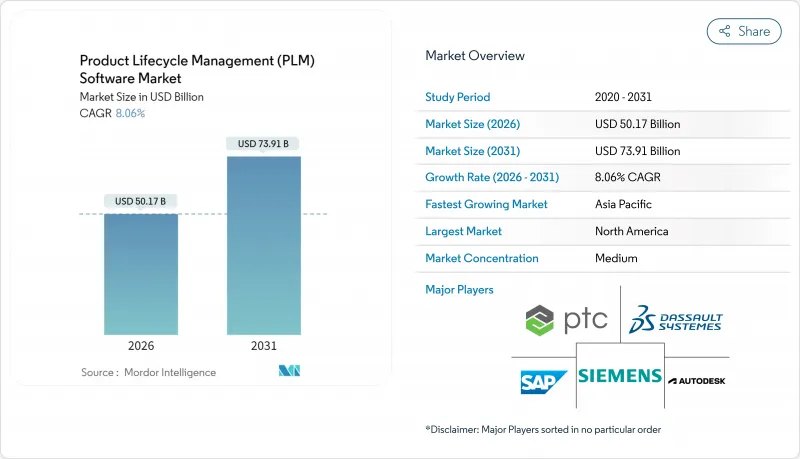

Product Lifecycle Management (PLM) Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Product Lifecycle Management (PLM) Software Market size reached USD 50.17 billion in 2026 and is projected to advance to USD 73.91 billion by 2031, reflecting an 8.06% CAGR during 2026-2031.

This trajectory is underpinned by fast-rising cloud adoption, the infusion of generative-AI copilots into engineering toolchains, and mounting regulatory demands for end-to-end digital traceability in automotive, aerospace, electronics, and life-sciences manufacturing. Tier-1 manufacturers are shifting toward SaaS platforms as elastic compute reduces simulation bottlenecks and real-time collaboration slashes review cycles. Incumbent vendors have moved aggressively to embed simulation, quality, and sustainability capabilities through acquisitions and platform extensions, while open-source alternatives apply price pressure, especially in cost-sensitive regions. Cyber-security concerns remain, yet continuous certification against FedRAMP, ISO 27001, and SOC 2 Type II is easing hesitancy among regulated industries. Mid-market firms, long held back by upfront capital outlays, now tap micro-subscription bundles that democratize access to best-of-breed PLM workflows.

Global Product Lifecycle Management (PLM) Software Market Trends and Insights

Cloud-First Adoption Among Tier-1 Manufacturers

Cloud-native PLM architectures reduce reliance on proprietary data centers and shorten global review loops. Siemens reported that cloud annual recurring revenue reached 49% of its EUR 5.3 billion (USD 5.67 billion) software ARR in fiscal Q4 2025, illustrating the velocity of SaaS migrations. PTC forecasts 7-9% ARR growth for 2026 as Windchill+ SaaS deployments accelerate. Elevated cloud uptake stems from on-demand compute that scales generative-design workloads without hardware over-provisioning, while real-time access for suppliers slashes engineering change-order latency.

Growing Need for End-to-End Digital Thread

A continuous digital thread links requirements, CAD, simulation, manufacturing instructions, and field data, enabling closed-loop feedback. NIST published a 2024 framework urging adoption of STEP AP242 and related schemas to knit PLM, ERP, and MES data together. Deloitte and Siemens formed the Digital Thread and Twin Alliance to operationalize such frameworks for aerospace and automotive clients. Early adopters report lower scrap, faster design iterations, and audit readiness as regulators request granular as-built traceability.

Persistent Interoperability Gaps Between Legacy CAD and Modern PLM

Hybrid CAD estates spanning CATIA, NX, SolidWorks, and Creo introduce data-translation errors when ported into cloud repositories. ITI documented that 30-40% of migrations still need manual remediation, inflating project timelines. Siemens' acquisition of Altair in January 2025 targets tighter integration of HyperWorks simulation with Teamcenter, yet neutral formats such as STEP remain unevenly adopted.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Product Traceability and Sustainability Reporting

- Generative-AI Copilots Trimming Engineering Change-Order Cycles

- Cyber-Security and IP Leakage Concerns in Multi-Tenant SaaS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations accounted for 56.66% revenue in 2025, a reminder that controlled technical data and legacy contracts still anchor many programs. The cloud segment of the PLM software market is growing at 10.96% CAGR to 2031, propelled by elastic compute that absorbs simulation spikes and supports global design reviews. The PLM software market size for cloud deployments is set to expand from USD 21.75 billion in 2026 to USD 36.61 billion in 2031, underscoring an irreversible shift toward SaaS. Siemens noted that cloud ARR equaled 49% of its software subscriptions by late 2025, confirming mainstream acceptance among Tier-1 manufacturers.

Hybrid topologies have emerged as a pragmatic compromise. Sensitive IP remains behind firewalls while supplier portals, digital twin analytics, and high-performance simulation burst to the cloud. Autodesk credits Fusion 360 for 15-16% manufacturing revenue growth in fiscal 2025 as mid-market fabricators adopted pay-as-you-go licensing. On-premise deployments will persist in defense and pharma, yet as cloud vendors attain FedRAMP and ISO 27001, growth will keep tilting to SaaS, reshaping support and upgrade economics across the Product Lifecycle Management (PLM) Software market.

Collaborative PDM maintained 48.26% revenue share in 2025 thanks to its core role in version control, change governance, and BOM hierarchy management. However, digital manufacturing and MES-PLM integration is the breakout segment, advancing at 9.32% CAGR. The Product Lifecycle Management (PLM) Software market size attributable to digital manufacturing solutions is anticipated to climb from USD 8.13 billion in 2026 to USD 12.75 billion in 2031. Siemens knitted Opcenter MES into Teamcenter to propagate engineering changes to shop-floor schedules, trimming scrap tied to outdated work instruction. Rockwell Automation achieved similar synergy by aligning FactoryTalk with PTC Windchill.

Simulation and analysis add-ons, now often delivered as cloud micro-services, reinforce the pull of integrated suites. Ansys introduced cloud-native solvers that handshake with Windchill and Teamcenter, compressing multi-physics validation from weeks to days. MCAD integration remains necessary for automotive chassis engineering, while application lifecycle management strengthens in electronics where firmware and hardware must co-evolve. Vendors bundling PDM, MES, and simulation under one contract gain stickiness, fortifying platform moats across the PLM software market.

The Product Lifecycle Management (PLM) Software Market Report is Segmented by Deployment Type (On-Premise, and Cloud), Solution Type (Collaborative PDM / CPDM, MCAD Integration PLM, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), End-User Industry (Automotive and Transportation, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 35.28% revenue share in 2025, spearheaded by entrenched PLM infrastructures in automotive, aerospace, and industrial machinery. The PLM software market share of the region reflects robust digital transformation budgets and early compliance with emerging cyber-security norms. U.S. manufacturers leverage tax credits for cloud R&D spending, smoothing SaaS transitions. Canadian aerospace clusters tap public-private consortia to pilot digital twins that integrate PLM with field sensor data.

Asia Pacific remains the fastest-growing region, posting a 10.44% CAGR through 2031. China's 14th Five-Year Plan actively subsidizes domestic PLM deployment to cut reliance on foreign engineering tools. India's digital manufacturing mission is pushing both domestic OEMs and global tier-one suppliers to unify design and production data via SaaS PLM. ASEAN electronics hubs in Vietnam and Thailand pair PLM rollouts with 5G factory networks, facilitating high-volume PCB design iterations.

Europe contributes sizable demand, centered in Germany, France, and the United Kingdom. CSRD-driven environmental reporting is prompting lifecycle-assessment plug-ins across PLM suites, while automotive and aerospace primes upgrade to manage hydrogen propulsion and urban air-mobility programs. Eastern Europe's contract manufacturers join EU value chains, adopting lightweight PLM to comply with customer audit requirements.

South America, the Middle East, and Africa remain nascent yet promising. Brazil's flex-fuel vehicle producers deploy PLM to juggle ethanol and gasoline variant engineering. Saudi Arabia's Vision 2030 funds digital industrial corridors where PLM orchestrates modular equipment builds. African telecom equipment refurbishers evaluate cloud PLM to optimize spare-parts logistics. Although absolute revenue lags, rising green-field investments yield double-digit growth pockets across the Product Lifecycle Management (PLM) Software Market.

- Siemens AG

- Dassault Systems SE

- PTC Inc.

- SAP SE

- Autodesk Inc.

- Oracle Corporation

- IBM Corporation

- ANSYS Inc.

- Aras Corporation

- Arena (SaaS by PTC)

- Infor Inc.

- Hexagon AB

- Bentley Systems Inc.

- Altair Engineering Inc.

- Propel Software

- IFS AB

- HCLTech xLMCloud

- Accenture Industry X

- OpenBOM

- Propulsion-PLM

- Centric Software

- CONTACT Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first Adoption among Tier-1 Manufacturers

- 4.2.2 Growing Need for End-to-End Digital Thread

- 4.2.3 Regulatory Push for Product Traceability and Sustainability Reporting

- 4.2.4 Generative-AI Copilots Trimming Engineering Change-Order Cycles

- 4.2.5 Micro-subscription PLM Bundles for SMB Value Chains

- 4.2.6 Low-Code PLM Platforms Democratising Custom Workflows (UNDER-REPORTED)

- 4.3 Market Restraints

- 4.3.1 Persistent Interoperability Gaps between Legacy CAD and Modern PLM

- 4.3.2 Cyber-security and IP Leakage Concerns in Multi-tenant SaaS

- 4.3.3 Growing Open-Source Digital-Twin Stacks Cannibalising Paid Licences

- 4.3.4 Trade-Policy-Driven Chip Export Controls Disrupting PLM Upgrade Cycles (UNDER-REPORTED)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Solution Type

- 5.2.1 Collaborative PDM / cPDM

- 5.2.2 MCAD Integration PLM

- 5.2.3 Simulation and Analysis

- 5.2.4 Digital Manufacturing and MES-PLM

- 5.2.5 ALM / SLM

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Aerospace and Defence

- 5.4.3 Electronics and High-Tech

- 5.4.4 Industrial Machinery and Heavy Equipment

- 5.4.5 Architecture, Engineering and Construction

- 5.4.6 Life Sciences and Medical Devices

- 5.4.7 Consumer Packaged Goods / Retail

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Dassault Systems SE

- 6.4.3 PTC Inc.

- 6.4.4 SAP SE

- 6.4.5 Autodesk Inc.

- 6.4.6 Oracle Corporation

- 6.4.7 IBM Corporation

- 6.4.8 ANSYS Inc.

- 6.4.9 Aras Corporation

- 6.4.10 Arena (SaaS by PTC)

- 6.4.11 Infor Inc.

- 6.4.12 Hexagon AB

- 6.4.13 Bentley Systems Inc.

- 6.4.14 Altair Engineering Inc.

- 6.4.15 Propel Software

- 6.4.16 IFS AB

- 6.4.17 HCLTech xLMCloud

- 6.4.18 Accenture Industry X

- 6.4.19 OpenBOM

- 6.4.20 Propulsion-PLM

- 6.4.21 Centric Software

- 6.4.22 CONTACT Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment