PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034984

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034984

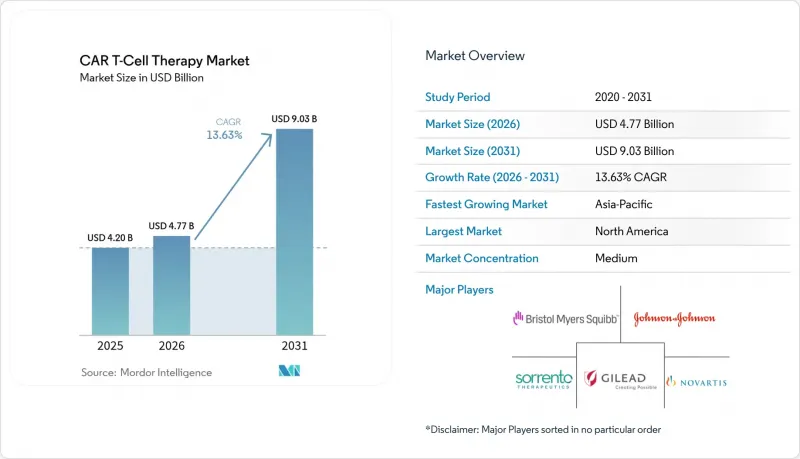

CAR T-Cell Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Global CAR T-Cell Therapy Market size was valued at USD 4.20 billion in 2025 and estimated to grow from USD 4.77 billion in 2026 to reach USD 9.03 billion by 2031, at a CAGR of 13.63% during the forecast period (2026-2031).

Uptake is accelerating as regulators permit use in earlier treatment lines, highlighted by the FDA's April 2024 clearance of Abecma after just two prior regimens, which broadens the eligible patient pool. North America remains the revenue leader on the back of established reimbursement, while Asia-Pacific is emerging as the fastest-expanding region thanks to dense clinical-trial activity and rising domestic manufacturing capacity. CD19-directed products continue to anchor sales, yet BCMA-targeted options are rapidly gaining momentum as earlier-line multiple-myeloma indications come online. Across Europe, point-of-care manufacturing hubs are cutting vein-to-vein time to roughly a week, giving early adopters a clear logistical advantage Blood. Persistent shortages of viral-vector capacity and high production costs, however, are constraining throughput and keeping pricing pressure in focus.

Global CAR T-Cell Therapy Market Trends and Insights

Second-line LBCL FDA Approvals Accelerating Early-Line Uptake

Phase 3 TRANSFORM data show Breyanzi delivering a 45.8% three-year event-free survival versus 19.1% for chemo in second-line LBCL, prompting oncologists to move CAR T earlier in the care cascade . Earlier-line positioning expands the pool of fitter patients, raising response durability and reducing salvage-therapy use. Competitors are therefore re-designing trials to target second-line settings, intensifying label-expansion races. Payers are beginning to weigh long-term cost offsets from reduced relapse, which may ease reimbursement hurdles. Collectively, these elements reinforce double-digit growth in the car t-cell therapy market.

Decentralised EU Point-of-Care Manufacturing Slashes Vein-to-Vein Time

The Euplagia-1 trial showed 92% overall and 75% complete response rates using a seven-day, on-site process in relapsed CLL/SLL Blood. Rapid manufacture cuts attrition in fast-progressing cancers and lifts centre capacity without large capital layouts. Developers such as Galapagos and academic consortia are scaling modular clean-rooms that can be grafted onto existing hospitals, a model already shaving costs for payers CGT Live. As regulators craft guidance on point-of-care quality control, firms with robust digital tracking are securing early site partnerships, speeding market penetration.

High Cost of Developing CAR T-Cell Therapy

Autologous batches require more than 200 labor hours and command list prices exceeding USD 500,000, thereby limiting uptake to high-income systems Oncoscience. Fragmented reimbursement in Latin America, the Middle East and parts of Eastern Europe leaves many eligible patients untreated. The economic burden has opened space for competing modalities such as bispecific antibodies, pressuring manufacturers to adopt automated closed systems or risk marginalisation. Programmes demonstrating outpatient feasibility and short adverse-event windows are best placed to convince payers of cost-effectiveness, but the constraint remains material for the car t-cell therapy market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Burden of Cancer Worldwide

- Allogeneic "Off-the-Shelf" Pipelines Lowering Cost-of-Goods

- Vector GMP Capacity Bottlenecks Raise Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CD19 platforms generated 46.05% of revenue in 2025, reflecting first-mover approvals across diffuse large B-cell lymphoma and paediatric ALL. Within this slice of the car t-cell therapy market, long-term datasets now exceed five years, underpinning physician confidence. BCMA constructs, boosted by Abecma's earlier-line label, are compounding at 14.02% through 2031, the quickest among current antigen classes. Dual-target programs that combine CD19 with CD20 or CD22 are entering mid-stage trials to combat antigen escape. Developers see potential to tap relapsed settings in chronic lymphocytic leukaemia and mantle-cell lymphoma, broadening the car t-cell therapy market.

Next-wave antigen strategies aim to move beyond haematology. GD2 programs are gaining ground in neuroblastoma, while HER2 constructs progress in gastric cancer cohorts. Chinese centres have opened over 20 trials on CLDN18.2, reflecting local gastric cancer prevalence. Should multi-specific designs show persistence advantages, CD19's share could erode, yet its entrenched installed base and manufacturing know-how support near-term dominance.

Autologous inventories delivered 91.25% of 2025 sales, cementing their role as the backbone of the car t-cell therapy market size at present. The personalised workflow fits existing regulatory frameworks and boasts five commercially approved brands. Nevertheless, vein-to-vein times of 2-4 weeks and variable product quality present obstacles in high-grade lymphomas. Allogeneic projects, projected to log a 15.22% CAGR, offer batch production, lower cost-of-goods and immediate dosing, attributes welcomed by cash-strapped payers.

Allogene, Precision BioSciences and Caribou are employing gene-editing tools to cloak donor cells from host immunity, aiming to match autologous durability. Early data suggest shorter cytopenia periods, improving outpatient viability. If large Phase 2 outcomes replicate this profile, the car t-cell therapy market could tilt toward off-the-shelf models later in the decade. Autologous incumbents are hedging by licensing allogeneic platforms, signalling market convergence rather than sudden displacement.

The CAR T-Cell Therapy Market Report is Segmented by Target Antigen (CD19, BCMA, CD22, GD2, and More), Type (Abecma, Breyanzi, and More), Cell Source (Autologous and Allogenic), Application (Leukemia, Lymphoma, and More), End User (Hospitals, Cancer Care Treatment Centers, and More), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 52.10% of 2025 global revenue, reflecting early FDA approvals, 311 accredited treatment sites and robust private insurance coverage. New CPT procedure codes, effective in 2025, should streamline billing and accelerate adoption outside academic hubs Oncology News Central. Nevertheless, access remains uneven; only 1 in 5 clinically eligible US patients currently receives therapy, creating white-space for mobile apheresis units and tele-monitoring services. Manufacturers with domestic vector plants and rapid-release testing enjoy smoother supply in light of persistent viral-vector bottlenecks.

Asia-Pacific is forecast to be the fastest-growing segment, advancing at 15.55% CAGR through 2031 as China surpasses the United States in registered CAR-T trials, tallying more than 300 by January 2024. Japan and South Korea are issuing expedited review pathways, aiming to domesticate manufacturing as a strategic healthcare asset. These developments place the region at the core of future expansion within the car t-cell therapy market.

Europe holds meaningful share with a distinct innovation edge in decentralised manufacturing. Seven-day point-of-care pilots in Belgium and Spain have proven technical feasibility and economic efficiency, positioning the bloc as a living lab for rapid delivery models Blood. Unified HTA rules slated for 2025 may harmonise reimbursement, yet country-level price negotiations still fragment uptake. Producers that couple modular clean-rooms with outcome-based pricing are most likely to penetrate price-sensitive systems. Collectively, geographic diversification cushions revenue streams and tempers region-specific policy risk across the car t-cell therapy market.

- Novartis

- Gilead Sciences

- Bristol-Myers Squibb

- Johnson & Johnson / Legend Biotech

- 2seventy bio Inc.

- Allogene Therapeutics

- Autolus Therapeutics plc

- Caribou Biosciences Inc.

- TCR2 Therapeutics Inc.

- Precision BioSciences Inc.

- Sorrento Therapeutics

- Sangamo Therapeutics

- Celyad Oncology SA

- Servier Laboratories

- Miltenyi Biotec B.V. & Co.

- Acro Biosystems

- JW Therapeutics

- Fosun Kite Biotechnology Co.

- Beigene Ltd.

- Gracell Biotechnologies Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Second-line LBCL FDA Approvals Accelerating Early-Line Uptake

- 4.2.2 Decentralised EU Point-of-Care Manufacturing Slashes Vein-to-Vein Time

- 4.2.3 Growing Burden of Cancer Worldwide

- 4.2.4 Allogeneic "Off-the-Shelf" Pipelines Lowering Cost-of-Goods

- 4.2.5 Increasing Invesment and Research and Development to Develop CAR T-Cell Therapy

- 4.2.6 Medicare NTAP Expansion to Community Oncology Centres Broadens Access

- 4.3 Market Restraints

- 4.3.1 High Cost of Developing CAR T-Cell Therapy

- 4.3.2 Vector GMP Capacity Bottlenecks Raise Lead-Times

- 4.3.3 Limited Patient Eligibility

- 4.3.4 Potential for Severe Side Effects

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Target Antigen

- 5.1.1 CD19

- 5.1.2 BCMA

- 5.1.3 CD22

- 5.1.4 GD2

- 5.1.5 HER2

- 5.1.6 PSMA

- 5.1.7 Multi-Target / Tandem

- 5.1.8 Others

- 5.2 By Cell Source

- 5.2.1 Autologous

- 5.2.2 Allogeneic

- 5.3 By Product (Approved)

- 5.3.1 Abecma

- 5.3.2 Breyanzi

- 5.3.3 Kymriah

- 5.3.4 Tecartus

- 5.3.5 Yescarta

- 5.3.6 Others

- 5.4 By Indication

- 5.4.1 Leukemia (ALL, CLL)

- 5.4.2 Lymphoma (DLBCL & Other B-Cell)

- 5.4.3 Multiple Myeloma

- 5.4.4 Auto-Immune Disorders

- 5.4.5 Others

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Cancer Care Treatment Centres

- 5.5.3 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia- Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Novartis AG

- 6.3.2 Gilead Sciences Inc. (Kite Pharma)

- 6.3.3 Bristol-Myers Squibb Co.

- 6.3.4 Johnson & Johnson / Legend Biotech

- 6.3.5 2seventy bio Inc.

- 6.3.6 Allogene Therapeutics Inc.

- 6.3.7 Autolus Therapeutics plc

- 6.3.8 Caribou Biosciences Inc.

- 6.3.9 TCR2 Therapeutics Inc.

- 6.3.10 Precision BioSciences Inc.

- 6.3.11 Sorrento Therapeutics Inc.

- 6.3.12 Sangamo Therapeutics Inc.

- 6.3.13 Celyad Oncology SA

- 6.3.14 Servier Laboratories

- 6.3.15 Miltenyi Biotec B.V. & Co.

- 6.3.16 ACROBiosystems

- 6.3.17 JW Therapeutics

- 6.3.18 Fosun Kite Biotechnology Co.

- 6.3.19 Beigene Ltd.

- 6.3.20 Gracell Biotechnologies Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment