PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034990

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034990

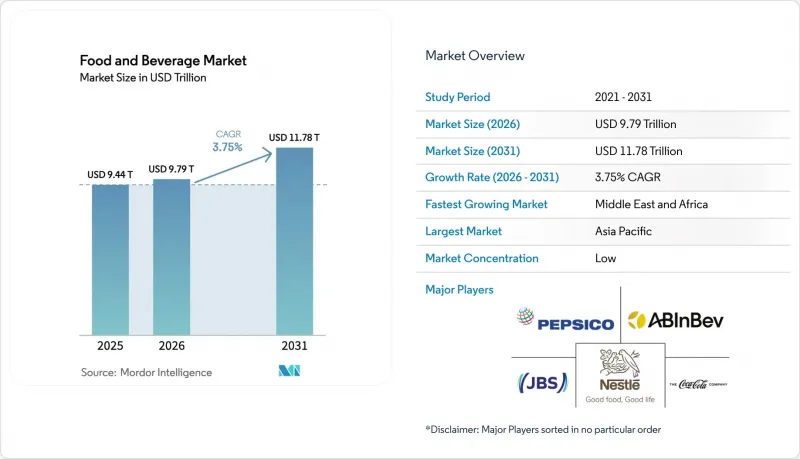

Food And Beverage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

food and beverage market size in 2026 is estimated at USD 9.79 trillion, growing from 2025 value of USD 9.44 trillion with 2031 projections showing USD 11.78 trillion, growing at 3.75% CAGR over 2026-2031.

The sector is expanding even as consumer tastes shift toward wellness, digital convenience, and sustainability. The market for functional foods and beverages is expanding as consumers demand products with enhanced nutritional and performance benefits. Growth reflects robust demand for faster adoption of e-commerce, and ongoing packaging upgrades that align with circular-economy rules. Pricing pressures remain, yet manufacturers are offsetting higher costs through automation, supply-chain partnerships, and premium positioning in organic portfolios. Intensifying regulatory oversight is raising compliance investments, but companies that modernize traceability and safety systems are securing long-term competitive advantages. Overall, the food and beverage market continues to demonstrate resilience through data-driven innovation and careful portfolio balancing.

Global Food And Beverage Market Trends and Insights

Growing Focus on Health and Wellness

Consumer emphasis on health is transforming the global packaged food and beverage market, with purchasing decisions increasingly influenced by nutritional value, ingredient transparency, and functional benefits. As per bioMerieux, in 2024, 75% of consumers demonstrate a willingness to pay premium prices for products without synthetic additives, establishing significant market opportunities for clean-label and minimally processed foods . Functional foods, which deliver specific health advantages including immune support, digestive health, and increased energy, constitute the market's fastest-growing segment. Advanced nutrition technologies enable manufacturers to develop products aligned with specific dietary requirements. Generation Z drives this market evolution, supporting companies that incorporate plant-based ingredients and demonstrate transparent sourcing and nutritional information. The market demonstrates product innovation through prebiotic and probiotic-enhanced snacks, protein beverages, and specialized hydration products. Food and beverage companies implement faster product development cycles and increase investment in health-focused product portfolios. This strategic focus on health benefits addresses current consumer requirements while supporting market growth.

Rising Convenience and On-the-Go Consumption

The global packaged food and beverage market demonstrates significant changes due to consumer requirements for products compatible with mobile lifestyles. The market indicates increased demand for single-serve, ready-to-eat, and shelf-stable products that deliver both convenience and nutritional value. New packaging formats, including resealable pouches and compact snack packs, facilitate portion control while enabling premium pricing and minimizing food waste. The Asia-Pacific region, specifically in urban markets, exhibits substantial growth as increased disposable incomes and time constraints drive consumer preferences toward convenient, high-quality food options. Manufacturers are enhancing distribution infrastructure through investments in cold-chain logistics, refrigerated transport, and delivery network optimization. The integration of digital inventory management systems enables retailers to maintain stock levels and meet consumer demand. Product development emphasizes convenient options, including nutrient-dense snacks, fortified beverages, and meal kits. These market developments capture key consumer segments, including working professionals and urban millennials, while establishing new standards for product quality and accessibility in the packaged food and beverage industry.

Stringent and Evolving Regulatory Compliance

Regulatory requirements have become increasingly stringent for food and beverage manufacturers, creating operational challenges and higher costs. Compliance expenditure has increased by over 1,400% since 2006 across major agricultural and food production regions, requiring companies to update their processes and invest in quality assurance systems. The FDA's recent bans on ingredients like brominated vegetable oil and Red Dye No. 3, along with new labeling requirements, have compelled manufacturers to modify product formulations . Additionally, regulations such as California's extended producer responsibility laws have introduced new fees and reporting requirements, increasing costs throughout the supply chain. While large multinational companies can manage these challenges through economies of scale and specialized regulatory teams, small and medium-sized enterprises (SMEs) face greater difficulties due to higher per-unit costs and limited resources. The increasingly strict global food safety and environmental standards continue to pose challenges for market participants, particularly affecting innovation and market access for smaller companies.

Other drivers and restraints analyzed in the detailed report include:

- Rising Digitalization and E-Commerce Expansion

- Surge in Food Safety and Quality Assurance Technologies

- Chronic Labour Shortages in Food and Beverage Manufacturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Supermarkets/hypermarkets dominated the global food and beverage market in 2025, capturing 51.10% of the total market share. These retailers maintain their market dominance through wide product selections, competitive prices, and convenient one-stop shopping experiences. Their extensive retail footprint and efficient supply chain networks enable regular inventory replenishment and consistent product availability, which helps retain customer loyalty.

The online retail channel is growing at a 5.63% CAGR, driven by changing consumer preferences, particularly in suburban and rural areas with limited access to physical stores. E-commerce platforms are expanding their market reach by offering diverse product selections, personalized recommendations, and home delivery services. Retailers are improving their fulfillment capabilities through investments in dark stores and automated picking systems to reduce delivery times and enhance order accuracy. Moreover, the retail landscape is transforming as traditional stores integrate digital capabilities, including click-and-collect services and real-time inventory management. This evolution has intensified competition between physical and online retailers as they focus on improving convenience, value, and product variety. The ongoing integration of technology and logistics improvements continues to reshape consumer purchasing patterns, emphasizing the need for adaptable and customer-focused strategies in the sector.

The food products segment captured 63.85% of the total food and beverage market share in 2025, reflecting the consistent demand for staples and diverse food sub-categories. This significant share stems from the fundamental necessity of food items and ongoing product development across bakery, confectionery, snacks, ready meals, and plant-based products. Bakery and confectionery manufacturers are modifying their formulations to meet sugar-reduction requirements and health standards, while ready meals continue to expand due to urban consumers' preference for convenient meal solutions. Meanwhile, beverage segment growth is projected at a CAGR of 4.42%, exceeding the food segment's expansion rate. Market demand continues to increase for premium hydration products, functional beverages with health benefits, and dairy alternatives. Collaborations between dairy companies and precision-fermentation startups, including Fonterra's partnerships, are creating new product opportunities in the alternative protein market.

Moreover, the snack segment is adapting by introducing fiber-rich and nutrient-dense products to meet consumer health preferences. The market for plant-based protein blends and meat hybrids is expanding due to growing interest from flexitarian consumers and sustainability-focused shoppers. These market changes are influencing product development and supporting growth across categories, as companies focus on health, sustainability, and convenience to increase their market presence in retail and online channels. The food and beverage market is expanding through innovation, lifestyle changes, and increased focus on wellness and environmental responsibility.

The Food and Beverage Market Report is Segmented by Product Category (Food, and Beverage), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, and More), Packaging Type (Plastic, Paperboard, and More), Nature (Conventional, and Organic/Natural), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The food and beverage market in Asia-Pacific constituted 40.88% of the global market value in 2025, making it the largest regional market. The region's growth stems from increasing urbanization and higher disposable incomes, which drive demand for packaged and premium products. Digital retail infrastructure, including mobile payment systems and e-commerce platforms, has improved delivery services and payment options, particularly among younger consumers. The beverage segment shows strong performance in functional hydration products and new drink varieties, supported by health-conscious urban consumers and expanding brand options from both international and domestic companies. While modern retail and digital channels expand, traditional markets and convenience stores remain important sales channels, emphasizing the importance of diverse distribution networks. The region's combination of established retail practices and emerging trends requires companies to develop products that align with local preferences while adapting to various retail formats.

North America commands a sizeable slice of the food and beverage market, driven by innovation in plant-based meats and functional snacks. Labour shortages intensify automation funding, while complex label mandates raise reformulation costs. Besides, Europe shows strong adoption of organic assortments and eco-friendly packaging, aided by consumer willingness to pay green premiums and by stringent policy frameworks such as the Single-Use Plastic Directive.

The Middle East and Africa region is forecast to advance at a 5.24% CAGR, propelled by youthful demographics and rising food-import dependence. Also, infrastructure upgrades and cold-chain investments are critical to curb spoilage in hot climates. Moreover, South America leverages export-oriented farm output yet faces currency swings and logistical gaps that hinder domestic processing scale. Across all geographies, the food and beverage market continues to blend local tastes with global health and sustainability themes.

- Nestle S.A.

- The Coca-Cola Company

- PepsiCo Inc.

- Anheuser-Busch InBev SA/NV

- JBS S.A.

- Tyson Foods Inc.

- Danone S.A.

- Unilever PLC

- Mondelez International, Inc.

- The Kraft Heinz Company

- Gujarat Cooperative Milk Marketing Federation (GCMMF)

- Heineken N.V.

- Arla Foods amba

- Mars, Incorporated

- General Mills, Inc.

- Beyond Meat, Inc.

- Conagra Brands, Inc.

- Suntory Holdings Limited

- Groupe Lactalis S.A.

- Hormel Foods Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Focus on Health and Wellness

- 4.2.2 Rising Convenience and On-the-Go Consumption

- 4.2.3 Rising Digitalization and E-Commerce Expansion

- 4.2.4 Surge in Food Safety and Quality Assurance Technologies

- 4.2.5 Product Innovation and Customization

- 4.2.6 Sustainability and Eco-Friendly Packaging

- 4.3 Market Restraints

- 4.3.1 Stringent and Evolving Regulatory Compliance

- 4.3.2 Rising Raw Material and Input Costs

- 4.3.3 Increased Competition and Market Saturation

- 4.3.4 Chronic labour shortages in Food and Beverage manufacturing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Category

- 5.1.1 Food

- 5.1.1.1 Dairy and Dairy Alternative Products

- 5.1.1.2 Bakery

- 5.1.1.3 Confectionery

- 5.1.1.4 Meat, Poultry, Seafood, and Meat Substitute

- 5.1.1.5 Snacks

- 5.1.1.6 Breakfast Cereals

- 5.1.1.7 Ready Meals

- 5.1.1.8 Sauces and Spreads

- 5.1.1.9 Others (Baby Food, and others)

- 5.1.2 Beverage

- 5.1.2.1 Alcoholic

- 5.1.2.1.1 Beer

- 5.1.2.1.2 Wine

- 5.1.2.1.3 Spirits

- 5.1.2.1.4 Others

- 5.1.2.2 Non-Alcoholic

- 5.1.2.2.1 Energy Drinks

- 5.1.2.2.2 Sports Drinks

- 5.1.2.2.3 Juices

- 5.1.2.2.4 Bottled Water

- 5.1.2.2.5 RTD Tea and Coffee

- 5.1.2.2.6 Others

- 5.1.2.1 Alcoholic

- 5.1.1 Food

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience/Grocery Stores

- 5.2.3 Online Retail Stores

- 5.2.4 Speciality Stores

- 5.2.5 Other Distribution Channel

- 5.3 By Packaging Type

- 5.3.1 Plastic Packaging

- 5.3.2 Paperboard Packaging

- 5.3.3 Metal Cans

- 5.3.4 Glass Packaging

- 5.3.5 Others (Tetra Pak/Cartons, Pouches, etc)

- 5.4 By Nature

- 5.4.1 Conventional

- 5.4.2 Organic/Natural

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 The Coca-Cola Company

- 6.4.3 PepsiCo Inc.

- 6.4.4 Anheuser-Busch InBev SA/NV

- 6.4.5 JBS S.A.

- 6.4.6 Tyson Foods Inc.

- 6.4.7 Danone S.A.

- 6.4.8 Unilever PLC

- 6.4.9 Mondelez International, Inc.

- 6.4.10 The Kraft Heinz Company

- 6.4.11 Gujarat Cooperative Milk Marketing Federation (GCMMF)

- 6.4.12 Heineken N.V.

- 6.4.13 Arla Foods amba

- 6.4.14 Mars, Incorporated

- 6.4.15 General Mills, Inc.

- 6.4.16 Beyond Meat, Inc.

- 6.4.17 Conagra Brands, Inc.

- 6.4.18 Suntory Holdings Limited

- 6.4.19 Groupe Lactalis S.A.

- 6.4.20 Hormel Foods Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK