PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034998

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034998

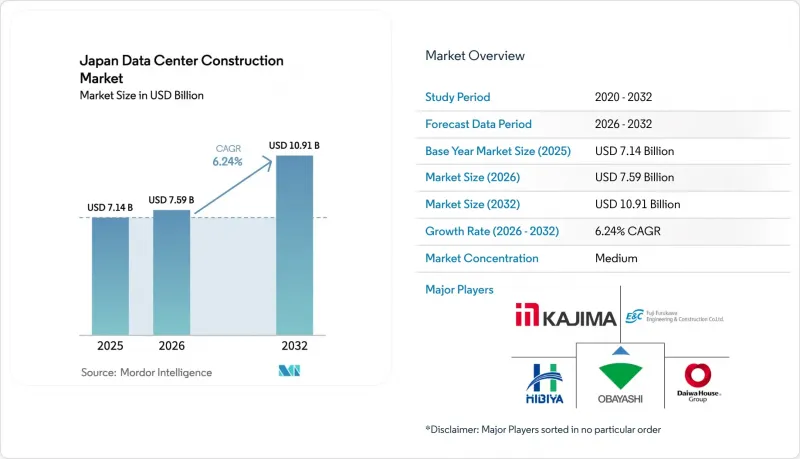

Japan Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032)

The Japan data center construction market size is expected to grow from USD 7.14 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 10.91 billion by 2032 at 6.24% CAGR over 2026-2032.

Rising hyperscale investments, sovereign-cloud mandates, and edge computing rollouts keep large projects in the pipeline, while seismic engineering expertise and liquid cooling innovations sharpen competitive advantages. The steady capital inflow from Japanese real-estate investment trusts (J-REITs), coupled with subsidies under the Economic Security Promotion Act, continues to ease financing constraints for domestic operators. Grid upgrade plans by Kansai Electric and other utilities mitigate power-availability risks, and higher voltage distribution designs support GPU-dense halls. However, skilled labor shortages and land-price inflation temper the build-out pace, pushing firms to pursue modular designs and secondary-metro sites for cost control. Operators increasingly favor renewable power purchasing agreements to protect margins from tariff volatility, reinforcing the shift toward northern regions with ample green energy.

Japan Data Center Construction Market Trends and Insights

Accelerating Cloud, AI and Big-Data Workloads

Rising generative-AI projects lift rack densities to 100 kW plus, raising electricity demand by up to 20% and forcing operators toward liquid immersion systems. SoftBank's 300 MW Tomakomai campus shows the new scale benchmark and targets 100% renewable power. GPU cloud providers such as Sakura Internet recorded a 476.3% profit jump in 2025, underscoring demand pull. Domestic oil major Idemitsu now supplies immersion fluids that cut cooling power 90%, anchoring a local value chain for sustainable AI infrastructure.

Hyperscale Campus Build-Outs by US and Domestic Majors

AWS has budgeted JPY 2.26 trillion through 2027, adding 30,500 annual jobs and JPY 5.57 trillion GDP impact. Oracle's USD 8 billion plan centers on data sovereignty clients in Tokyo and Osaka. On the domestic front, the KDDI-Sharp alliance aims to open Asia's largest cloud campus, while EdgeConneX is deploying 140 MW in Osaka to serve AI clusters. These multiyear programs anchor construction order books and intensify competition for skilled contractors.

Grid-Power Bottlenecks and Surging Electricity Tariffs

Kansai Electric will invest more than JPY 150 billion from 2026 on four substations serving new campuses. Operators face extended grid-connection queues and tariff spreads that make Hokkaido the most expensive and Hokuriku the least. Higher costs strain profit margins just as liquid cooling drives power draw above historic norms. Some firms lock renewable PPAs or install on-site generation to hedge exposure.

Other drivers and restraints analyzed in the detailed report include:

- Sovereign-Cloud and Data-Residency Regulations

- 5G-Driven Edge-DC Demand in Secondary Metros

- Scarcity of Tier-III/IV-Certified MEP Labor

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical infrastructure accounted for 37.62% of 2025 revenue, anchoring the Japan data center construction market share with high-voltage switchgear and busway upgrades. Services, though smaller, are forecast to achieve an 8.05% CAGR through 2032 as operators pay premiums for seismic engineering, immersion-cooling design, and AI workload layout optimization. Canon IT Solutions' West Tokyo site now supports 100 kVA liquid-cooled racks, showcasing hybrid cooling integration. Construction material inflation of 21-24% since 2021 pushes firms to modularize builds and pre-fabricate power rooms for faster delivery.

Japan data center construction market size expansion in services reflects demand for capacity-planning, commissioning, and retrofit consulting tied to generative-AI ramps. Mechanical infrastructure evolves toward dielectric fluids and direct-chip cooling, while IT infrastructure maintains steady orders for GPU servers despite enterprise cloud migration.

Tier III facilities maintained 56.42% Japan data center construction market share in 2025, serving enterprises and colocation tenants that value cost balance. Tier IV projects, though fewer, are rising at 8.43% CAGR through 2032 as hyperscale operators accept higher capital intensity for uninterrupted AI model training. Obayashi deploys active base isolation and ultra-high strength steel to secure Tier IV uptime in seismic zones.

Japan data center construction market size for Tier IV builds concentrates in the Tokyo-Osaka corridor where land costs justify high-density, high-availability designs. Tier I and Tier II legacy sites see attrition as tenants migrate workloads to cloud platforms demanding higher fault tolerance.

The Japan Data Center Construction Market is Segmented by Infrastructure (Electrical Infrastructure, Mechanical Infrastructure, and More), Tier Standard (Tier I and II, Tier III, and More), Data Center Type (Colocation, Hyperscale, and More), End User Industry (Banking Financial Services and Insurance, IT and Telecommunications, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Obayashi Corporation

- Taisei Corporation

- Kajima Corporation

- Shimizu Corporation

- Takenaka Corporation

- Tokyu Construction

- Toda Corporation

- Maeda Corporation

- Daiwa House Industry Co., Ltd.

- Penta-Ocean Construction

- Fuji Furukawa Engineering and Construction

- Nishimatsu Construction

- Sumitomo Mitsui Construction

- Hazama Ando

- Kitano Construction

- Mirai-Build (Mirait Holdings)

- Haseko Corporation

- Kinden Corporation (EPC)

- JGC Japan

- DRP Construction Japan

- AECOM Japan

- Fluor Japan

- Hibiya Engineering Ltd

- ARUP Japan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating cloud, AI and big-data workloads

- 4.2.2 Hyperscale campus build-outs by US and domestic cloud majors

- 4.2.3 Sovereign-cloud and data-residency regulations

- 4.2.4 5G-driven edge-DC demand in secondary metros

- 4.2.5 J-REIT capital inflows into shell-ready DC sites (under-the-radar)

- 4.2.6 Seismic base-isolation tech de-risking mega-facilities (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Grid-power bottlenecks and surging electricity tariffs

- 4.3.2 Scarcity of Tier-III/IV-certified MEP labour

- 4.3.3 Lengthy environmental licensing and community opposition

- 4.3.4 Escalating land prices inside Tokyo-Chiba-Kanagawa corridor (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Japan Data-Center Construction Statistics

- 4.8.1 Data Centers Total Installed Capacity (MW) in the Japan, 2023 and 2024

- 4.8.2 Total IT Load Under Construction in the Japan, MW, 2025 - 2030

- 4.8.3 Average Capex and Opex for the Japan Data Center Construction

- 4.8.4 Top Capex Spenders on Data Center Infrastructure in the Japan

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, US$ BN)

- 5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 Power Distribution Solutions

- 5.1.1.1.1 Power Distribution Units

- 5.1.1.1.2 Switchgears

- 5.1.1.1.3 Others

- 5.1.1.2 Power Backup Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.1 Power Distribution Solutions

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Liquid-based Cooling

- 5.1.2.1.2 Air-based Cooling

- 5.1.2.2 Racks and Cabinets

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.3 IT Infrastructure

- 5.1.3.1 Servers

- 5.1.3.2 Storage

- 5.1.3.3 Other IT Infrastructure

- 5.1.4 General Construction

- 5.1.5 Services

- 5.1.5.1 Design and Consulting

- 5.1.5.2 Integration

- 5.1.5.3 Support and Maintenance

- 5.1.1 Electrical Infrastructure

- 5.2 By Tier Standard

- 5.2.1 Tier I and II

- 5.2.2 Tier III

- 5.2.3 Tier IV

- 5.3 By Data Center Type

- 5.3.1 Colocation Data Centers

- 5.3.2 Hyperscale / Self-built Data Centers

- 5.3.3 Others (Enterprise / Edge / Modular)

- 5.4 By End User Industry

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Obayashi Corporation

- 6.2.2 Taisei Corporation

- 6.2.3 Kajima Corporation

- 6.2.4 Shimizu Corporation

- 6.2.5 Takenaka Corporation

- 6.2.6 Tokyu Construction

- 6.2.7 Toda Corporation

- 6.2.8 Maeda Corporation

- 6.2.9 Daiwa House Industry Co., Ltd.

- 6.2.10 Penta-Ocean Construction

- 6.2.11 Fuji Furukawa Engineering and Construction

- 6.2.12 Nishimatsu Construction

- 6.2.13 Sumitomo Mitsui Construction

- 6.2.14 Hazama Ando

- 6.2.15 Kitano Construction

- 6.2.16 Mirai-Build (Mirait Holdings)

- 6.2.17 Haseko Corporation

- 6.2.18 Kinden Corporation (EPC)

- 6.2.19 JGC Japan

- 6.2.20 DRP Construction Japan

- 6.2.21 AECOM Japan

- 6.2.22 Fluor Japan

- 6.2.23 Hibiya Engineering Ltd

- 6.2.24 ARUP Japan

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment