PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035001

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035001

Japan Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

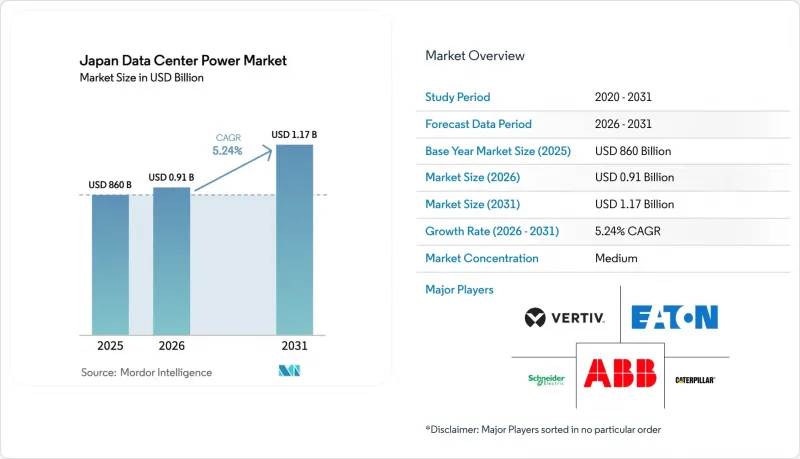

The Japan data center power market size is expected to grow from USD 860 million in 2025 to USD 910 million in 2026 and is forecast to reach USD 1.17 billion by 2031 at 5.24% CAGR over 2026-2031.

Robust cloud-first strategies, fast-rising AI workloads, and a sustained push for carbon-neutral operations are combining to raise demand for resilient, energy-efficient infrastructure. The market is also buoyed by new submarine-cable landings that widen connectivity options and stimulate investment in secondary coastal cities. Power-hungry hyperscale campuses are increasing average facility capacity from 10-15 MW three years ago to well above 40 MW today, forcing utilities to reinforce local grids and driving operators toward on-site renewable generation and large battery systems. Grid fragmentation between the 50 Hz east and 60 Hz west continues to complicate interconnection strategies, yet it is spurring new partnerships focused on frequency-independent storage technologies. Corporate Power Purchase Agreements (PPAs) signed by Google and Equinix in 2024-2025 mark a decisive shift toward long-term renewable procurement contracts that buffer operators against volatile utility tariffs.

Japan Data Center Power Market Trends and Insights

Rising adoption of hyperscale and cloud facilities

Hyperscale operators now commission campuses exceeding 40 MW, pushing rack densities past 60 kW and occasionally 100 kW.SoftBank's 300 MW Tomakomai complex in Hokkaido demonstrates how mega campuses decentralize processing loads while tapping cooler climates for free-air cooling advantages. Such scale drives localized grid congestion, especially around Tokyo, where new capacity requests face lead times of up to 36 months. Consequently, operators experiment with modular power blocks that work independently of grid constraints and allow phased expansion. This trend keeps the Japan data center power market on a steep modernization curve as facilities deploy lithium-ion-based UPS systems and busway distribution to accommodate volatile AI workloads

Government-led digital-transformation programs

The Green Growth Strategy requires data centers to draw from renewable sources as the national grid targets a 36-38% clean-energy share by 2030. Japan's Climate Transition Bond program seeks JPY 120 trillion (USD 800 billion) to finance renewable projects that directly feed digital infrastructure.Authorities also offer fast-track permitting for power projects in regional prefectures rich in wind or solar resources, redirecting data center investment beyond the Tokyo-Osaka corridor. Incentives include tax reductions for equipment that improves power usage effectiveness (PUE), which helps raise the overall competitiveness of the Japan data center power market.

Grid congestion and power-availability limits

Tokyo's distribution network is strained by cumulative hyperscale loads that outpace substation upgrades. Operators queue for capacity reservations, delaying go-live dates and inflating project budgets. Battery energy storage systems (BESS) paired with PPAs offer interim relief but add to upfront spend. Utilities respond by reinforcing coastal transmission corridors that coincide with new submarine-cable landings, yet the lag keeps grid congestion a material brake on the Japan data center power market.

Other drivers and restraints analyzed in the detailed report include:

- 5G roll-out and edge build-outs accelerating demand

- Renewable power and carbon-neutral mandates

- High installation and maintenance CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UPS systems controlled 37.60% of the Japan data center power market in 2025, underscoring their role as a first-line defense against grid instability. Lithium-ion adoption shortens recharge cycles and lowers footprint despite a price premium, an acceptable trade-off for hyperscale campuses that target sub-1.3 PUE levels. The generator category is undergoing a pivot from diesel toward hydrogen fuel cells, a shift highlighted by pilot deployments in Shunan City that pair reused automotive cells with on-site solar arrays. PDUs, holding a vital position for high-density racks, will post the fastest component growth at 6.45% CAGR to 2031 due to granular metering and remote branch-level monitoring. This momentum keeps the Japan data center power market squarely focused on intelligent distribution technologies that integrate with DCIM platforms.

The UPS refresh cycle aligns with AI-driven compute clusters that demand stable power delivery at scale, pushing vendors to embed predictive analytics for battery health inside their firmware. Energy-storage modules linked to UPS frameworks help shave peak demand charges and improve renewable absorption rates. As carbon-free targets tighten, operators rely on continuous-cycle UPS architectures capable of syncing with microgrids that fluctuate when cloud cover or wind speeds change. The component mix, therefore, evolves toward systems that safeguard loads yet also act as grid-interactive assets within the wider Japan data center power market.

Colocation providers account for 60.95% of total consumption because enterprises prize interconnection-rich campuses that deliver diverse carrier access and compliance clarity. Tokyo's multi-tenant facilities remain preferred on-ramp sites into the broader Asian cloud fabric. Hyperscale cloud operators, while fewer in number, represent the fastest growth slice at 7.85% CAGR as domestic AI and machine-learning workloads surge. Public-sector digital-transformation programs and fintech adoption spur demand for secure cages and dedicated halls, reinforcing colocation's central role in the Japan data center power market.

Edge and enterprise sites form a complementary layer that supports 5G latency targets. Their modest 1-5 MW footprints adopt modular power trains and containerized battery packs to shorten lead times. Combined, these tiers diversify locations at which Japan data center power market capacity is installed, cushioning the grid and raising overall resilience. International players partner with local power specialists to navigate regulatory hurdles tied to frequency mismatches and seismic safety, ensuring that new builds, whether colocation or hyperscale, integrate robust backup schemes from inception

Japan Data Center Power Market is Segmented by Component (Electrical Solutions, Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd

- Schneider Electric SE

- Vertiv Group Corp.

- Mitsubishi Electric Corp.

- Eaton Corporation

- Cummins Inc.

- Caterpillar Inc.

- Hitachi Energy Ltd.

- Legrand Group

- Rittal GmbH and Co. KG

- Fujitsu Ltd.

- Toshiba Energy Systems and Solutions

- Kohler Power Systems

- Fuji Electric Co. Ltd.

- Socomec Group

- Delta Electronics Inc.

- Huawei Technologies Co. Ltd.

- Nidec Corp.

- Rolls-Royce Power Systems (MTU)

- Cisco Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of hyperscale and cloud facilities

- 4.2.2 Government-led digital-transformation programs

- 4.2.3 5G roll-out and edge build-outs accelerating demand

- 4.2.4 Renewable power and carbon-neutral mandates

- 4.2.5 Regional submarine-cable landings boosting rural builds

- 4.2.6 On-site corporate PPAs driving battery storage uptake

- 4.3 Market Restraints

- 4.3.1 High installation and maintenance CAPEX

- 4.3.2 Grid congestion and power-availability limits

- 4.3.3 Stringent seismic-resilience compliance costs

- 4.3.4 Shortage of high-voltage power engineers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (advanced UPS, BESS, solid-state switchgear)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assesment of Macroeconomic Trends on the Market

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Electrical Solutions

- 5.1.1.1 UPS Systems

- 5.1.1.2 Generators

- 5.1.1.2.1 Diesel Generators

- 5.1.1.2.2 Gas Generators

- 5.1.1.2.3 Hydrogen Fuel-cell Generators

- 5.1.1.3 Power Distribution Units

- 5.1.1.4 Switchgear

- 5.1.1.5 Transfer Switches

- 5.1.1.6 Remote Power Panels

- 5.1.1.7 Energy-storage Systems

- 5.1.2 Service

- 5.1.2.1 Installation and Commissioning

- 5.1.2.2 Maintenance and Support

- 5.1.2.3 Training and Consulting

- 5.1.1 Electrical Solutions

- 5.2 By Data Center Type

- 5.2.1 Hyperscaler/Cloud Service Providers

- 5.2.2 Colocation Providers

- 5.2.3 Enterprise and Edge Data Center

- 5.3 By Data Center Size

- 5.3.1 Small Size Data Centers

- 5.3.2 Medium Size Data Centers

- 5.3.3 Large Size Data Centers

- 5.3.4 Massive Size Data Centers

- 5.3.5 Mega Size Data Centers

- 5.4 By Tier Level

- 5.4.1 Tier I and II

- 5.4.2 Tier III

- 5.4.3 Tier IV

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Schneider Electric SE

- 6.4.3 Vertiv Group Corp.

- 6.4.4 Mitsubishi Electric Corp.

- 6.4.5 Eaton Corporation

- 6.4.6 Cummins Inc.

- 6.4.7 Caterpillar Inc.

- 6.4.8 Hitachi Energy Ltd.

- 6.4.9 Legrand Group

- 6.4.10 Rittal GmbH and Co. KG

- 6.4.11 Fujitsu Ltd.

- 6.4.12 Toshiba Energy Systems and Solutions

- 6.4.13 Kohler Power Systems

- 6.4.14 Fuji Electric Co. Ltd.

- 6.4.15 Socomec Group

- 6.4.16 Delta Electronics Inc.

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Nidec Corp.

- 6.4.19 Rolls-Royce Power Systems (MTU)

- 6.4.20 Cisco Systems Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment