PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035002

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035002

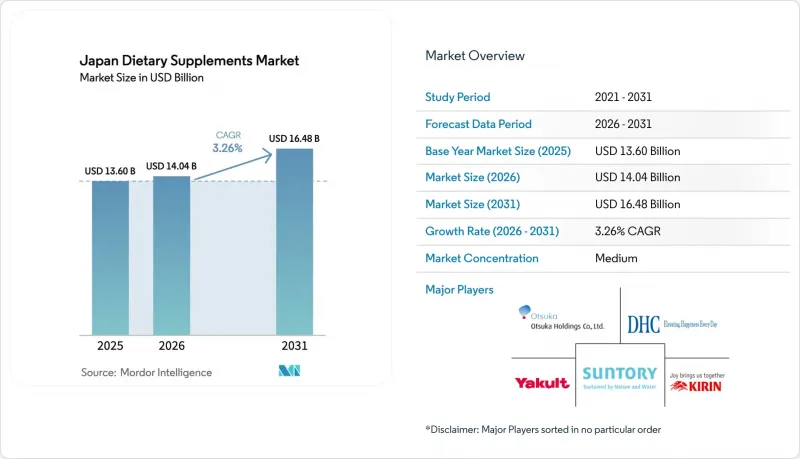

Japan Dietary Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japanese dietary supplements market size was valued at USD 13.60 billion in 2025 and estimated to grow from USD 14.04 billion in 2026 to reach USD 16.48 billion by 2031, at a CAGR of 3.26% during the forecast period (2026-2031).

This moderate growth rate masks significant underlying shifts in consumer preferences and product innovation, particularly in response to Japan's super-aging society, where supplements are increasingly viewed as essential health maintenance tools rather than optional wellness products. The aging population is driving demand for condition-specific nutrients, supported by the shift of a robust retail ecosystem toward online channels and advancements in probiotics, gummies, and plant-based formats. Government initiatives that position supplements as complements to food rather than pharmaceuticals continue to strengthen consumer trust. Additionally, premiumization trends are contributing to higher average selling prices. Market leaders are enhancing scientific validation, establishing cross-industry partnerships with biotech and digital health firms, and expanding their presence across broader Asian markets. Although cost-of-living challenges and stricter labeling regulations are moderating demand, they have not disrupted the positive revenue growth trajectory.

Japan Dietary Supplements Market Trends and Insights

Rising Emphasis on Preventive Healthcare

Japan's healthcare system is transitioning from a treatment-focused model to a prevention-oriented framework. To mitigate rising healthcare costs, consumers are increasingly adopting preventive health measures. According to the Organisation for Economic Co-operation and Development (OECD), the per capita health expenditure in Japan was USD 5,639.62 in 2023. This shift is driving substantial growth opportunities in the dietary supplements market, as these products are being positioned as essential components of proactive health management strategies. A key example of this transition is the Specific Health Checkup initiative, which has demonstrated a measurable reduction in the prevalence of chronic conditions such as diabetes and hypertension among participants compared to non-participants. The adoption of preventive healthcare practices is particularly strong among younger demographics, including millennials and Gen Z, who are increasingly incorporating dietary supplements into their daily routines. These consumer segments exhibit a strong preference for products that provide immune-boosting and energy-enhancing benefits, aligning with their active lifestyles and long-term health objectives.

Emergence of Personalized Nutrition Platforms Leveraging Gut-Microbiome Testing

Japan's supplement market is undergoing a significant transformation, driven by advancements in gut microbiome research and the integration of digital health technologies. These innovations are enabling the development of highly personalized solutions tailored to the unique biological profiles of individual consumers, marking a shift toward precision nutrition. For instance, Meiji Seika Pharma launched its meiQua supplement brand. This brand is strategically positioned to address specific nutrient deficiencies identified through comprehensive medical consultations and diagnostic testing. By leveraging a science-based approach, the brand aligns with the evolving preferences of Japan's well-informed and health-conscious consumer base, which increasingly prioritizes products supported by credible scientific evidence. This shift in consumer behavior is reflected in the personalized nutrition segment, which is projected to grow at nearly twice the rate of the overall supplements market. This growth underscores a clear trend as consumers move away from generic offerings and gravitate toward tailored solutions designed to meet their distinct biological and nutritional needs.

Counterfeit Products Stifling Growth

The prevalence of counterfeit dietary supplements is undermining consumer trust and disrupting various markets, particularly within e-commerce, where ensuring product authenticity remains a persistent challenge. This issue is especially significant in Japan, as counterfeit products often enter the market through cross-border e-commerce platforms. High-value segments, such as beauty supplements, are disproportionately impacted due to their premium pricing, which incentivizes counterfeit activities. To address this concern, leading manufacturers are increasingly implementing advanced authentication technologies, including blockchain-based traceability systems and QR code verification mechanisms, to protect product integrity. However, the adoption of these advanced technologies leads to higher operational costs, which are ultimately transferred to consumers, influencing overall market dynamics.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Wellness Programs Expanding Workplace Supplement Purchases

- Aging Population Driving Condition-Specific Supplement Uptake

- Growing Consumer Doubts on Synthetic Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The vitamins segment holds a significant 34.78% share of the market, highlighting its critical role in Japan's dietary supplementation industry. Recognized as essential for daily health support, vitamins are particularly valued by seniors seeking to maintain independence and prevent frailty. In comparison, the probiotics segment is anticipated to grow at a strong CAGR of 5.63% during the forecast period of 2026-2031. This growth is driven by increasing scientific research linking gut health to overall wellness and immunity, alongside advancements in delivery systems and strain-specific formulations that address a wider range of health concerns beyond digestion.

Yakult Honsha, leveraging its established cultural association with fermented products, has expanded its probiotic offerings. Its latest product, the Yakult BL Firstone capsule, incorporates the proprietary Lactobacillus casei strain Shirota, providing a convenient option for daily consumption. The protein and amino acids segment is diversifying its market focus, moving beyond traditional sports nutrition to target the aging population with claims centered on sarcopenia prevention. Simultaneously, herbal supplements are witnessing growth, driven by increasing consumer interest in traditional Japanese and Asian botanicals, supported by modern scientific research.

While capsules and softgels currently dominate the market with a 37.64% share in 2025, the gummies segment is experiencing explosive growth at 4.14% CAGR (2026-2031), revolutionizing supplement consumption patterns across demographic groups. This growth is significantly altering supplement consumption patterns across various demographic groups. The trend underscores a growing emphasis on improving the consumption experience and ensuring compliance, particularly among younger consumers and seniors who often encounter difficulties with traditional pill formats. Technological advancements in gummy formulations have addressed previous challenges related to ingredient stability and dosage precision, enabling the efficient delivery of active ingredients in consumer-preferred formats.

The tablet segment remains a significant market player but is gradually losing share to more consumer-focused formats. Powders continue to be relevant, especially in protein supplements and drink mixes. The liquid segment is gaining momentum in beauty-from-within products and energy formulations, leveraging its rapid absorption properties. Recent innovations include collagen gummies with enhanced bioavailability and probiotic gummies utilizing patented microencapsulation technology to maintain product efficacy. This diversification in delivery formats enables manufacturers to target specific demographic groups with tailored solutions, thereby broadening the consumer base beyond traditional supplement users.

The Japan Dietary Supplements Market Report is Segmented by Product Type (Vitamins, Minerals, and More), Form (Tablets, Capsules, and More), Source (Plant-Based, Animal-Based, and More), Consumer Group (Men, Women, and Kids/Children), Health Application (General Health and Wellness, and More), and Distribution Channel (Supermarkets/Hypermarkets, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Otsuka Pharmaceutical Co. Ltd.

- Suntory Holdings Limited

- ITOH KANPO PHARMACEUTICAL Co.,Ltd

- DHC Corporation

- Kobayashi Pharmaceutical Co. Ltd.

- Yakult Honsha Co. Ltd.

- Asahi Group Holdings, Ltd.

- Kirin Holdings Company, Ltd.

- Meiji Holdings Co. Ltd.

- Orihiro Co., Ltd.

- Taisho Pharmaceutical Co., Ltd.

- Nestle S.A.

- Abbott Laboratories

- Amway Corporation

- Herbalife Nutrition Ltd.

- Bayer AG

- NOW Health Group Inc.

- Nissin Foods Group

- Haleon Plc

- LKK Group Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Emphasis on Preventive Healthcare

- 4.2.2 Emergence of Personalized Nutrition Platforms Leveraging Gut-Microbiome Testing

- 4.2.3 Corporate Wellness Programs Expanding Workplace Supplement Purchases

- 4.2.4 Aging Population Driving Condition-Specific Supplement Uptake

- 4.2.5 Increasing Awareness of Nutritional Deficiencies Driving Supplement Adoption

- 4.2.6 Rising E-commerce Penetration Enhancing Accessibility to Dietary Supplements

- 4.3 Market Restraints

- 4.3.1 Counterfeit Products Stifling Growth

- 4.3.2 Growing Consumer Doubts on Synthetic Additives and Concerns Over Mega-Dose Safety

- 4.3.3 Stringent Advertising Rules Limiting Health-Benefit Claims

- 4.3.4 High Production Costs Challenge Market Expansion

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Vitamins

- 5.1.2 Minerals

- 5.1.3 Fatty Acids

- 5.1.4 Protein and Amino Acids

- 5.1.5 Prebiotic and Probiotic Supplements

- 5.1.6 Herbal Supplements

- 5.1.7 Enzymes

- 5.1.8 Blended Supplements

- 5.1.9 Other Types

- 5.2 By Form

- 5.2.1 Tablets

- 5.2.2 Capsules and Softgels

- 5.2.3 Powders

- 5.2.4 Gummies

- 5.2.5 Liquids

- 5.2.6 Other Forms

- 5.3 By Source

- 5.3.1 Plant-Based

- 5.3.2 Animal-Based

- 5.3.3 Synthetic/Fermentation-Derived

- 5.4 By Consumer Group

- 5.4.1 Men

- 5.4.2 Women

- 5.4.3 Kids/Children

- 5.5 By Health Application

- 5.5.1 General Health and Wellness

- 5.5.2 Bone and Joint Health

- 5.5.3 Energy and Weight Management

- 5.5.4 Gastrointestinal and Gut Health

- 5.5.5 Immunity Enhancement

- 5.5.6 Cardiovascular Health

- 5.5.7 Diabetes Management

- 5.5.8 Cognitive and Mental Health

- 5.5.9 Skin, Hair, and Nail Care

- 5.5.10 Eye Health

- 5.5.11 Other Health Applications

- 5.6 By Distribution Channel

- 5.6.1 Supermarkets/Hypermarkets

- 5.6.2 Specialty Stores

- 5.6.3 Online Retail Stores

- 5.6.4 Direct Selling

- 5.6.5 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Otsuka Pharmaceutical Co. Ltd.

- 6.4.2 Suntory Holdings Limited

- 6.4.3 ITOH KANPO PHARMACEUTICAL Co.,Ltd

- 6.4.4 DHC Corporation

- 6.4.5 Kobayashi Pharmaceutical Co. Ltd.

- 6.4.6 Yakult Honsha Co. Ltd.

- 6.4.7 Asahi Group Holdings, Ltd.

- 6.4.8 Kirin Holdings Company, Ltd.

- 6.4.9 Meiji Holdings Co. Ltd.

- 6.4.10 Orihiro Co., Ltd.

- 6.4.11 Taisho Pharmaceutical Co., Ltd.

- 6.4.12 Nestle S.A.

- 6.4.13 Abbott Laboratories

- 6.4.14 Amway Corporation

- 6.4.15 Herbalife Nutrition Ltd.

- 6.4.16 Bayer AG

- 6.4.17 NOW Health Group Inc.

- 6.4.18 Nissin Foods Group

- 6.4.19 Haleon Plc

- 6.4.20 LKK Group Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK