PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035007

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035007

Fire Alarm Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

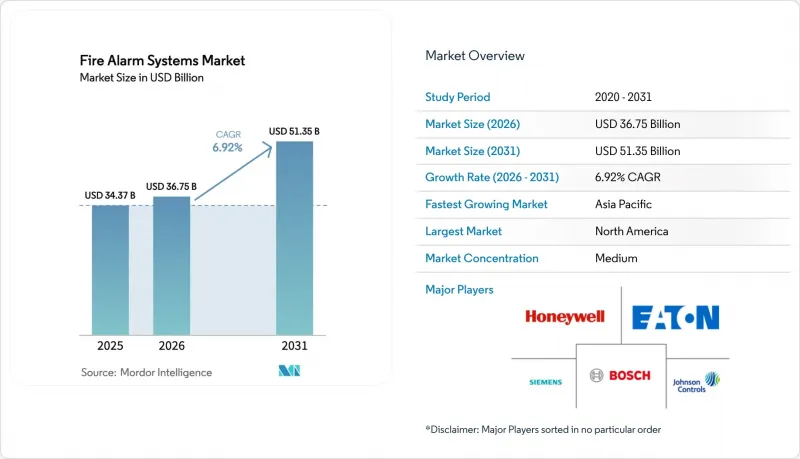

The fire alarm systems market size was valued at USD 34.37 billion in 2025 and estimated to grow from USD 36.75 billion in 2026 to reach USD 51.35 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031).

Strong code enforcement, the spread of smart-building projects, and a broad transition from hard-wired conventional panels to connected, addressable platforms sustained this growth path during 2024 and 2025. Commercial developers favored networkable systems that integrate with wider building-management software, while data-center operators and battery-storage owners demanded specialized detection and suppression that protect sensitive electronics. Rapid code revisions, such as NFPA 72 (2025), introduced cybersecurity obligations, thermal-imaging detection, and acoustic leak sensing, forcing vendors to redesign products and installers to upskill. Private-equity funds accelerated roll-ups to create national service platforms, a response to the technician shortage that lifted labour costs but widened aftermarket revenue opportunities. Regionally, spending momentum shifted toward the Asia-Pacific, while North America maintained scale advantages through earlier adoption of smart-facility retrofits.

Global Fire Alarm Systems Market Trends and Insights

Stringent Global Fire-Safety Regulations and Codes

Code revisions shaped demand during 2024-2025. The 2025 update of NFPA 72 made cybersecurity controls, acoustic leak detection, and thermal-imaging capabilities mandatory for new addressable panels, following federal alerts that exposed buffer-overflow flaws that hackers could exploit in legacy systems. European EN 54 standards moved in parallel, shifting certification from component-level to full-system testing to assure functional integrity. In North America, UL 217 and UL 268 smoke-alarm rules suppressed kitchen nuisance alarms, compelling residential builders to specify new sensor algorithms. As a result, the fire alarm systems market experienced a surge in retrofit orders, particularly on healthcare and education campuses, where "Restricted Audible Mode Operation" became mandatory for patient- and student-sensitive zones.

Acceleration of Commercial Real Estate and Smart Building Construction

Developers prioritized digital readiness even amid material-cost inflation. Fire alarm platforms with open APIs linked to energy dashboards, visitor management, and security video feeds, creating a single pane of glass for facility operators. Edge computers inside new panels processed smoke-sensor data locally, trimming latency for suppression commands while reserving the cloud for fleet-wide analytics. Wireless detectors and annunciators were chosen for retrofit towers where conduit labour had become cost-prohibitive, cutting installation time by up to 35%. Even with supply bottlenecks, contractors kept adoption high because smart-ready projects earned higher lease rates, reinforcing the upward trajectory of the fire alarm systems market.

High Upfront Installation and Retrofitting Costs

Addressable technology and specialty detectors carried price premiums of 15-25% over conventional gear through 2025. Retrofit projects in hospitals and heritage sites faced extra hurdles such as asbestos abatement and infection-control partitions, doubling labour hours. The technician shortfall, half of North American service firms reported vacancies amplified wage benchmarks and stretched project timelines. Small enterprises delayed upgrades or opted for the lowest-cost, limited-feature panels, creating a bifurcated demand curve inside the broader fire alarm systems market.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Conventional to Addressable and Networked Systems

- Rapid Expansion of Datacenters and Li-ion Battery Storage Facilities

- Nuisance/False-Alarm Frequency and Associated Fines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Detectors accounted for 35.12% of the fire alarm systems market in 2025 and are projected to grow at an 8.07% CAGR through 2031. Platform makers embedded micro-fog smoke, rate-of-rise heat, CO, and air-quality chambers in one housing, allowing algorithms to cross-reference signals and silence spurious alarms. Cloud-linked detectors streamed self-diagnostic data, giving service firms advance notice of contamination or impending battery depletion. As IoT frameworks mature, detectors become addressable nodes that feed real-time status into digital twins, a capability prized by pharmaceutical plants pursuing zero-downtime goals.

Control panels followed a parallel path of innovation. New boards incorporated dual IP ports, LTE failover, and TPM chips that meet NFPA 72 cyberhardening guidance. Power-supply modules switched to lithium-ion backup packs rated for 24-hour standby, halving rack footprint. Notification appliances utilized low-profile LED strobes and intelligible voice horns to comply with accessibility regulations. As accessories such as BACnet gateways and PoE switch racks are sold alongside every panel, the component mix becomes a system-level package that expands the average selling price, reinforcing growth within the fire alarm systems market.

Addressable fire alarm systems accounted for 64.12% of the fire alarm systems market share in 2025, a dominance that deepened as price gaps narrowed, while hybrid systems are set to expand at a 10.03% CAGR through 2031. Builders preferred them for precise point identification and for remote service functions that cut truck rolls by 20%. Modular addressable loops accepted wireless translators, creating hybrid topologies suited to phased renovations.

Conventional panels retained footholds in low-rise retail and rural warehouses, yet their share slid each year as copper costs rose. Voice evacuation systems, once a niche technology, gained mainstream traction after the NFPA introduced Restricted Audible Mode Operation to reduce patient stress in hospitals. This pushed panel makers to bundle audio amplifiers and prerecorded message libraries. In parallel, wireless-only systems blossomed in historic buildings where drilling masonry is restricted, delivering the fastest incremental revenue segment of the fire alarm systems market.

Fire Alarm Systems Market is Segmented by Component (Detector, Control Panels, Notification Devices, and More), System Type (Conventional Fire Alarm Systems, Hybrid Systems, and More), Technology (IoT-Enabled Smart Alarms, and More), End-User Industry (Commercial, Industrial, Residential, Government and Institutional, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained leadership in the fire alarm systems market, accounting for 40.02% of 2025 revenue. Adoption remained high because existing stock replaced legacy panels to comply with NFPA 72 cyber provisions and UL nuisance-alarm rules. Service companies widened e-learning programs to close talent gaps, and private-equity backed roll-ups stitched regional contractors into nationwide compliance networks. Municipal incentive funds for school retrofits hinged on voice evacuation and network supervision supported baseline demand.

Asia-Pacific delivered the fastest expansion, clocking a 9.42% CAGR to 2031. Urban infrastructure projects in India, Indonesia, and Vietnam specified addressable systems with seismic-resistant enclosures. Japanese regulators advanced guidelines urging cybersecurity safeguards for connected building subsystems; while not yet codified nationally, the stance spurred early uptake of encrypted panel communications. South Korean research institutes demonstrated AI smoke algorithms that trimmed false dispatches in high-rise kitchens, catalysing local vendor investment in embedded analytics.

Europe posted steady mid-single-digit growth after EN 54 revisions compelled whole-system certification, elevating barriers for low-cost imports. German factories automated compliance logs to satisfy workplace inspectors, expanding sales of panels equipped with digital event-report exports. Meanwhile, mergers accelerated as UK and Nordic service firms dove into cross-border acquisitions, drawn by predictable code-driven maintenance fees. The resulting scale increased bargaining power on component sourcing, curbing inflationary pressure, and safeguarding margin in the region's portion of the fire alarm systems market.

- Honeywell International Inc.

- Johnson Controls International plc

- Siemens Aktiengesellschaft

- Robert Bosch GmbH (Bosch Building Technologies)

- Eaton Corporation plc

- Halma plc

- Hochiki Corporation

- Nittan Company, Limited

- Carrier Global Corporation (Kidde & Edwards)

- Gentex Corporation

- Fike Corporation

- Mircom Group of Companies

- Apollo Fire Detectors Ltd

- Xtralis Pty Ltd

- System Sensor LLC

- Notifier

- Vigilant Fire & Security Systems

- Space Age Electronics Inc.

- Advanced Electronics Ltd

- Kentec Electronics Ltd

- Fike Corporation

- EMS Security Group Ltd

- Electro Detectors Ltd

- Cerberus (Phoenix Contact)

- Det-Tronics (Detector Electronics Corporation)

- Securiton AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent global fire-safety regulations and codes

- 4.2.2 Acceleration of commercial real-estate and smart-building construction

- 4.2.3 Migration from conventional to addressable and networked systems

- 4.2.4 Rapid expansion of data-centers and Li-ion battery storage facilities

- 4.2.5 NFPA 915-driven remote inspection and predictive-maintenance adoption

- 4.2.6 Private-equity consolidation accelerating product innovation

- 4.3 Market Restraints

- 4.3.1 High upfront installation and retrofitting costs

- 4.3.2 Nuisance/false-alarm frequency and associated fines

- 4.3.3 Shortage of certified technicians for advanced systems

- 4.3.4 Cyber-vulnerabilities in cloud-connected alarm networks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Imapct of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Detectors

- 5.1.2 Control Panels

- 5.1.3 Notification Devices

- 5.1.4 Power Supplies

- 5.1.5 Accessories

- 5.2 By System Type

- 5.2.1 Conventional Fire Alarm Systems

- 5.2.2 Addressable Fire Alarm Systems

- 5.2.3 Hybrid Systems

- 5.2.4 Wireless Fire Alarm Systems

- 5.2.5 Voice Evacuation Systems

- 5.3 By Technology

- 5.3.1 IoT-Enabled Smart Alarms

- 5.3.2 AI-Based Analytics and Predictive Detection

- 5.3.3 Cloud-Connected Monitoring Platforms

- 5.3.4 Edge-Computing Enabled Devices

- 5.4 By End-User Industry

- 5.4.1 Commercial

- 5.4.2 Industrial

- 5.4.3 Residential

- 5.4.4 Government and Institutional

- 5.4.5 Transportation and Infrastructure

- 5.4.6 Energy and Utilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Johnson Controls International plc

- 6.4.3 Siemens Aktiengesellschaft

- 6.4.4 Robert Bosch GmbH (Bosch Building Technologies)

- 6.4.5 Eaton Corporation plc

- 6.4.6 Halma plc

- 6.4.7 Hochiki Corporation

- 6.4.8 Nittan Company, Limited

- 6.4.9 Carrier Global Corporation (Kidde & Edwards)

- 6.4.10 Gentex Corporation

- 6.4.11 Fike Corporation

- 6.4.12 Mircom Group of Companies

- 6.4.13 Apollo Fire Detectors Ltd

- 6.4.14 Xtralis Pty Ltd

- 6.4.15 System Sensor LLC

- 6.4.16 Notifier

- 6.4.17 Vigilant Fire & Security Systems

- 6.4.18 Space Age Electronics Inc.

- 6.4.19 Advanced Electronics Ltd

- 6.4.20 Kentec Electronics Ltd

- 6.4.21 Fike Corporation

- 6.4.22 EMS Security Group Ltd

- 6.4.23 Electro Detectors Ltd

- 6.4.24 Cerberus (Phoenix Contact)

- 6.4.25 Det-Tronics (Detector Electronics Corporation)

- 6.4.26 Securiton AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment