PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035012

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035012

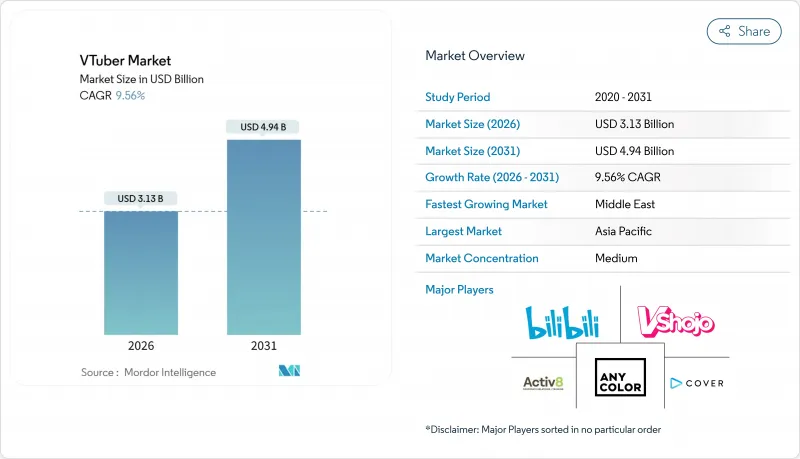

VTuber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The VTuber market size reached USD 3.13 billion in 2026 and is forecast to advance to USD 4.94 billion by 2031, reflecting a CAGR of 9.56%.

This growth trajectory is anchored in accessible motion-capture hardware, diversified monetization layers, and AI-enabled multilingual capabilities that broaden audience reach. Investors validated the business model when Cover Corp listed on the Tokyo Stock Exchange in 2024, and subsequent stock appreciation through 2025 underscored confidence in recurring revenue from subscriptions, donations, and merchandise. Parasocial engagement metrics also strengthened: Ironmouse sustained Twitch subscriber records in 2024, demonstrating that virtual talent can equal or surpass traditional entertainers in loyalty and revenue intensity. Platform fragmentation is accelerating discovery as indie agencies leverage decentralized scouting, while lower entry costs invite hobbyist experimentation. Concurrently, brand collaborations, from the Los Angeles Dodgers to Lawson convenience stores, validated commercial appeal across both physical and digital channels.

Global VTuber Market Trends and Insights

Advances in Real-Time Motion Capture and Live2D/3D Animation Tools

Hardware once reserved for studios now fits a consumer budget, lowering production hurdles for the VTuber market. Sony's mocopi launched in 2024 at USD 450, bringing six-axis inertial tracking into home setups. Rokoko's USD 2,500 Smartsuit Pro II added haptic feedback the same year, enhancing dance sequences and physical comedy. Unreal Engine 5 integrated Live2D workflows, letting creators swap between 2D and 3D without rebuilding assets. Nvidia's RTX 4090 cut real-time ray-tracing latency by 40%, making cinematic 3D streams viable on consumer PCs. These tools squeeze the quality gap between indie creators and agency-backed talent, opening the VTuber market to a broader pool while raising audience expectations.

Rapid Growth of Live Streaming Platform Monetization Models

Predictable revenue splits now underpin professional careers. YouTube paid creators about USD 1.2 billion via Super Chat and memberships in 2024, a pool disproportionately captured by VTubers who run multi-hour streams. Twitch shifted top partner splits to 70-30 in 2024, directly increasing VTuber earnings. Bilibili's tiered gifting offers creators 70% after fees, and TikTok rolled out LIVE Subscriptions globally with USD 4.99 entry pricing. Layering these income streams lets successful creators cross six-figure annual earnings without agency advances, underpinning sustainable expansion of the VTuber market.

High Production and Talent Management Costs

Premium content still demands capital. Optical capture solutions from Vicon cost about USD 50,000, restricting use to top agencies. AnyColor disclosed that talent management absorbed 42% of revenue in fiscal 2024, eroding margins and pressuring share price. Mid-tier agencies without large merchandise backends face consolidation pressure, while indie creators must self-fund upgrades and moderation labor. These financial burdens temper the overall VTuber market growth, especially in regions with higher labor costs.

Other drivers and restraints analyzed in the detailed report include:

- Strong Commercial Brand Adoption and Sponsorship Deals with VTubers

- AI-Powered Multilingual Autotranslation Enabling Global Audience Reach

- Intellectual Property and Licensing Complexities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 2D segment controlled 59.24% of VTuber market share in 2025 thanks to low rendering overhead and quick design refresh cycles. Live2D's 2024 physics update narrowed realism gaps, and open-source Inochi2D eliminated licensing fees, keeping barriers low for new entrants. However, rising demand for concert-grade visuals is propelling 3D avatars at an 11.17% CAGR. Unreal Engine 5 and Nvidia RTX 4090 have trimmed production latency, enabling indie studios to elevate quality without enterprise hardware. Agencies like Cover Corp lean into 3D for flagship talents, leveraging studio-grade capture to monetize ticketed events. Indie creators maintain 2D for daily streams yet increasingly test 3D for music videos and collaborations, reflecting strategic coexistence rather than a zero-sum shift within the VTuber market.

3D expansion is further fueled by VR adoption. Meta Quest 3 introduced affordable full-body tracking, allowing performers to engage audiences inside immersive venues. Spatial audio and dynamic lighting create premium fan experiences that justify higher ticket pricing. Conversely, 2D retains strengths in comedic timing and rapid meme iteration. The dual-format landscape allows creators to mix modalities: a debut might start in 2D to validate character appeal, then migrate to 3D as revenue scales. This flexibility preserves creator autonomy and underpins resilient growth for the VTuber market.

Livestreaming commanded 69.71% of the VTuber market size in 2025 as real-time interaction maximized donations and Super Chat volumes. Yet derivative content is climbing at an 11.27% CAGR. Hololive Super Expo 2025 repackaged concerts into standalone music videos that keep accruing ad revenue long after event completion. Short-form clips on TikTok and YouTube Shorts funnel discovery to long-form streams, forming a circular content economy. VTubers are also branching into scripted series, voice acting, and educational modules, which diversify risk from livestream fatigue.

Niche enterprise uses are emerging. A Japanese pharmaceutical firm reported 30% higher completion rates for VTuber-hosted e-learning modules, hinting at incremental revenue veins outside entertainment. Livestream saturation is evident as average concurrent viewership dipped 8% in 2024, intensifying differentiation pressures. Agencies now invest in post-production and music capabilities, evolving into full media studios to capitalize on evergreen assets. This pivot broadens monetizable surfaces and stabilizes revenue seasonality, supporting the long-term health of the VTuber market.

The VTuber Market Report is Segmented by Type (2D VTuber, and 3D VTuber), Application (Livestreaming and Performance, Digital Contents and Derivative, Other Application), Revenue Stream (Subscriptions and Donations, Sponsorship and Advertising, and More), Distribution Platform (YouTube, Bilibili, Twitch, Tiktok, Proprietary and Other Distribution Platform), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 65.14% of VTuber market revenue in 2025, powered by Japan's mature agency ecosystem and China's Bilibili infrastructure. Cover Corp and AnyColor together captured roughly 60% of Japanese receipts, illustrating regional concentration amid global fragmentation. South Korea's market lagged its robust K-pop sector due to limited monetization tools, whereas India's English-language creators targeted diaspora audiences through YouTube livestreams that fit Asia-Pacific time zones.

Growth momentum is shifting. The Middle East is set to log an 11.51% CAGR to 2031 as Saudi Vision 2030 funds digital entertainment studios and streaming venues. The United Arab Emirates clarified influencer licensing in 2024, giving VTubers legal certainty on revenue flows and IP rights. These policy moves entice agencies to establish regional hubs and cultivate Arabic-language rosters, diversifying away from saturated English and Japanese markets.

North America and Europe show steady uptake driven by VShojo's expansion and Hololive English's content pipeline, yet viewer competition stiffens as supply outpaces audience growth. Payment friction hampers South America, where high transaction fees erode creator shares on Super Chat and Twitch subscriptions. Africa remains nascent due to bandwidth constraints and low card penetration, but smartphone adoption trends suggest upside once fintech solutions mature. Overall, varied regulatory regimes, infrastructure quality, and disposable income levels shape the regional mosaics that collectively fuel the VTuber market.

- Cover Corp.

- AnyColor Inc

- Bilibili Inc

- VShojo Inc

- Mikai Inc

- Yuehua Entertainment

- Globie Inc

- Idol Corporation

- Taiwan VTuber Association

- United Talent Agency

- Activ8 Inc

- Neo-Porte Inc

- Phase-Connect

- NoriPro

- Virtual eSports Project

- V&U

- CAPTUREROID

- GeeXPlus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in Real-Time Motion Capture and Live2D/3D Animation Tools

- 4.2.2 Rapid Growth of Live Streaming Platform Monetization Models

- 4.2.3 Strong Commercial Brand Adoption and Sponsorship Deals with VTubers

- 4.2.4 Expansion of Fan Merchandise and Digital Goods Ecosystems

- 4.2.5 AI-Powered Multilingual Autotranslation Enabling Global Audience Reach

- 4.2.6 Affordable Cloud-Based Avatar Pipeline Services for Indie Creators

- 4.3 Market Restraints

- 4.3.1 High Production and Talent Management Costs

- 4.3.2 Intellectual Property and Licensing Complexities

- 4.3.3 Stringent Platform Policies and Content Moderation Risks

- 4.3.4 Audience Fatigue from Algorithmic Content Saturation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape Analysis

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 2D VTuber

- 5.1.2 3D VTuber

- 5.2 By Application

- 5.2.1 Livestreaming and Performance

- 5.2.2 Digital Contents and Derivative

- 5.2.3 Other Application

- 5.3 By Revenue Stream

- 5.3.1 Subscriptions and Donations

- 5.3.2 Sponsorship and Advertising

- 5.3.3 Merchandise and Licensing

- 5.3.4 Ticketed Events and Concerts

- 5.4 By Distribution Platform

- 5.4.1 YouTube

- 5.4.2 Bilibili

- 5.4.3 Twitch

- 5.4.4 TikTok

- 5.4.5 Proprietary and Other Distribution Platform

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cover Corp.

- 6.4.2 AnyColor Inc

- 6.4.3 Bilibili Inc

- 6.4.4 VShojo Inc

- 6.4.5 Mikai Inc

- 6.4.6 Yuehua Entertainment

- 6.4.7 Globie Inc

- 6.4.8 Idol Corporation

- 6.4.9 Taiwan VTuber Association

- 6.4.10 United Talent Agency

- 6.4.11 Activ8 Inc

- 6.4.12 Neo-Porte Inc

- 6.4.13 Phase-Connect

- 6.4.14 NoriPro

- 6.4.15 Virtual eSports Project

- 6.4.16 V&U

- 6.4.17 CAPTUREROID

- 6.4.18 GeeXPlus

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment