PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035019

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035019

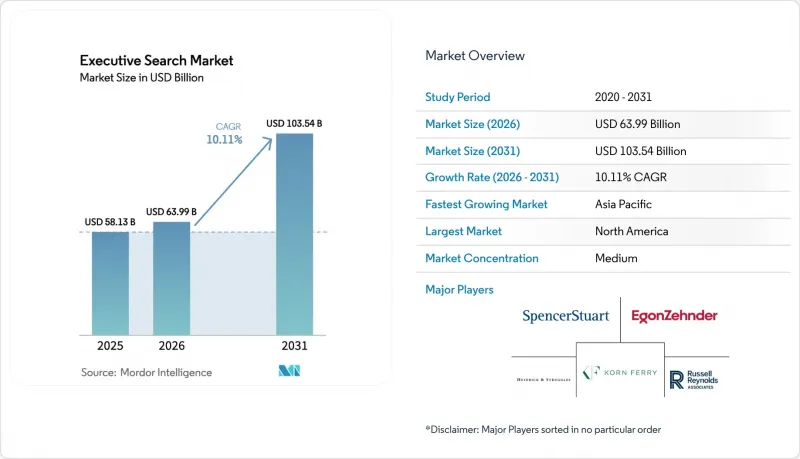

Executive Search - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The executive search market size in 2026 is estimated at USD 63.99 billion, growing from 2025 value of USD 58.13 billion with 2031 projections showing USD 103.54 billion, growing at 10.11% CAGR over 2026-2031.

Robust demand for leadership talent in digital transformation, ESG compliance, and corporate governance sustains double-digit growth even as in-house talent teams expand. Specialized C-suite roles such as Chief AI and Chief Sustainability Officers shorten executive tenures and intensify search cycles, while interim leadership assignments complement permanent placements to create new revenue streams for providers. Global private equity dry powder and heightened succession activity in family-owned enterprises add structural drivers that counterbalance pricing pressure from internal recruiting functions. Regulatory frameworks around data localization and sustainability reporting reinforce barriers to entry and favor search firms with sophisticated compliance infrastructure, thereby enabling premium fee structures.

Global Executive Search Market Trends and Insights

Growing demand for leadership talent in emerging and frontier markets

Companies in Asia Pacific, Latin America, and the Middle East and Africa accelerate professionalization as they scale beyond founder leadership and invite multinational competition. Family-owned enterprises that generate more in revenue seek external executives to manage succession complexity and globalize operations. The executive search market benefits because established firms offer local compliance expertise in regions where data privacy laws are tightening. Private equity inflows into fast-growing economies intensify the need for seasoned operators able to enact value-creation plans before exit events. Talent scarcity across frontier geographies allows retained search models to maintain premium fee structures and extended engagement timelines. Providers that combine on-the-ground networks with cross-border assessment methodologies enjoy sustainable competitive advantages.

Rise of specialized, next-gen executive roles (Chief AI, Chief Sustainability)

Artificial intelligence job titles tripled between 2022 - 2024 as organizations recognized AI governance as a C-suite imperative. Nearly half of large enterprises intend to appoint a Chief AI Officer within 12 months to mitigate algorithmic risk and unlock productivity gains. Parallel momentum surrounds Chief Sustainability Officers as ESG reporting deadlines approach, illustrated by Heidrick & Struggles expanding its Climate and Sustainability Practice in late 2024. Scarce candidate supply elongates search cycles and supports average fee structures of 33% on first-year cash compensation for specialized mandates. Retained search firms strengthen pricing power because contingency or DIY platforms cannot replicate their curated shortlists for niche roles.

Pricing pressure from in-house TA and RPO teams

Enterprises investing in internal recruiting report 30% to 35% cost savings when shifting mandates away from external firms. Recruitment Process Outsourcing providers expand up-market, competing for director-level and even selective C-suite searches at lower margins. Advanced internal teams leverage LinkedIn Recruiter, automated outreach, and employer branding to approach passive executives directly. Yet the executive search market retains an advantage for high-stakes placements because mis-hires at senior levels can cost USD 17,000 to USD 240,000 in downstream productivity losses. Search firms emphasize risk-mitigation and cultural alignment to justify retainers and defend pricing.

Other drivers and restraints analyzed in the detailed report include:

- Digital-transformation-driven C-suite churn

- Fractional leadership and interim CEO model adoption

- AI-enabled DIY talent platforms reducing external spend

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Retained engagements accounted for 62.88% of executive search market share in 2025, underlining persistent client preference for exclusivity when stakes are highest. The executive search market size attributed to retained searches reflected USD 36.55 billion, and hybrid models are projected to expand at 11.72% CAGR through 2031 as companies demand outcome-based pricing flexibility.

Hybrid contracts marry AI-powered candidate mapping with milestone-driven fees, reducing upfront commitment while preserving search rigor. Private equity clients favor hybrid structures to stretch budget across multiple portfolio companies, and technology improvements around remote interviewing reduce logistical costs. Contingency search remains relevant for director-level appointments but faces commoditization as internal sourcing capabilities mature.

C-suite mandates comprised 50.64% of overall placements in 2025, signaling the segment's importance to the executive search market size. Within this cadre, Chief Digital and Chief AI Officer searches are projected to grow at an 11.03% CAGR, outpacing traditional CEO and CFO roles.

Organizations prioritize technology literacy in top leadership, with 82% integrating AI responsibilities into business strategy by 2024. The surge elevates fee potential because candidate pools remain shallow. EVP and VP searches hold steady as firms build succession benches, whereas middle-management layers continue to thin under delayering strategies, pushing more responsibility to director roles.

The Executive Search Market Report is Segmented by Search Type (Retained, Contingency, and Hybrid/Engaged), Function Level (C-Suite, EVP/SVP/VP, and More), End-User Organization Type (Corporate/Private Sector, Government and Public-Sector Bodies, and More), Industry Vertical (Technology and Digital Services, Life Sciences and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38.20% executive search market share in 2025, buoyed by a concentration of Fortune 500 headquarters, robust private equity ecosystems, and active M&A pipelines. Short CEO tenures and venture capital-backed unicorn proliferation in technology corridors like Silicon Valley and Austin sustain premium search activity. Boards intensify governance scrutiny, elevating demand for directors versed in cybersecurity and ESG oversight, further anchoring retained search engagement.

Asia Pacific is projected to record a 10.71% CAGR through 2031, reflecting economic growth, capital market maturation, and succession planning in family-owned conglomerates. It is expected that family businesses to comprise a signficiant rate of large enterprises by 2025, signaling amplified leadership professionalization requirements. Governments encourage foreign direct investment in technology, healthcare, and renewable energy, which in turn necessitates localized executive talent capable of navigating regulatory and cultural complexity.

Europe maintains steady expansion underpinned by ESG regulation. The Corporate Sustainability Reporting Directive drives board refreshment cycles for sustainability expertise, while GDPR enforcement imposes stringent data-handling protocols that elevate compliance costs for smaller challengers. Continued post-Brexit corporate restructuring in financial services sustains cross-border leadership searches centered on Paris, Frankfurt, and Amsterdam hubs. Emerging regions in South America and the Middle East and Africa register rising mandates tied to infrastructure development and digital economy investments, though geopolitical volatility tempers overall contribution.

- Korn Ferry (KF Holdings, Inc.)

- Heidrick and Struggles International, Inc.

- Spencer Stuart Associates, LLC

- Russell Reynolds Associates, Inc.

- Egon Zehnder International AG

- Boyden World Corporation

- Odgers Berndtson Group Ltd.

- Signium International, Inc.

- DHR International, Inc.

- Stanton Chase International GmbH

- Amrop Partnership SCRL

- Caldwell Partners International, Inc.

- Allegis Partners, LLC

- True Talent Advisory, LLC (True Search)

- N2Growth, Inc.

- JM Search, Inc.

- Kestria International (U.N.I. Partners s.r.o.)

- ZSG (Executive Search) LLC

- Lucas Group, a Korn Ferry Company

- JMJ Phillip Holdings, Inc.

- Egon Zehnder International AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for leadership talent in emerging and frontier markets

- 4.2.2 Rise of specialized, next-gen executive roles (Chief AI, Chief Sustainability)

- 4.2.3 Digital-transformation-driven C-suite churn

- 4.2.4 Fractional leadership and interim CEO model adoption

- 4.2.5 ESG and sustainability mandates driving new board searches

- 4.2.6 Professionalization of family-owned enterprises in frontier economies

- 4.3 Market Restraints

- 4.3.1 Pricing pressure from in-house TA and RPO teams

- 4.3.2 Diversity metric compliance increasing search cycle time

- 4.3.3 AI-enabled DIY talent platforms reducing external spend

- 4.3.4 Cross-border data-privacy regulations limiting candidate pools

- 4.4 Customer Behavior Landscape

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Search Type

- 5.1.1 Retained

- 5.1.2 Contingency

- 5.1.3 Hybrid / Engaged

- 5.2 By Function Level

- 5.2.1 C-Suite (CEO, CFO, etc.)

- 5.2.2 EVP / SVP / VP

- 5.2.3 Director Level and Above

- 5.2.4 Niche / Emerging Roles (Chief AI, CISO, etc.)

- 5.3 By End-User Organization Type

- 5.3.1 Corporate / Private Sector

- 5.3.2 Government and Public-Sector Bodies

- 5.3.3 Non-Profit and NGOs

- 5.3.4 Private-Equity / Venture-Backed Firms

- 5.4 By Industry Vertical

- 5.4.1 Technology and Digital Services

- 5.4.2 Life Sciences and Healthcare

- 5.4.3 Financial Services

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Consumer and Retail

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia Pacific

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Alliances, Digital Platforms)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Korn Ferry (KF Holdings, Inc.)

- 6.4.2 Heidrick and Struggles International, Inc.

- 6.4.3 Spencer Stuart Associates, LLC

- 6.4.4 Russell Reynolds Associates, Inc.

- 6.4.5 Egon Zehnder International AG

- 6.4.6 Boyden World Corporation

- 6.4.7 Odgers Berndtson Group Ltd.

- 6.4.8 Signium International, Inc.

- 6.4.9 DHR International, Inc.

- 6.4.10 Stanton Chase International GmbH

- 6.4.11 Amrop Partnership SCRL

- 6.4.12 Caldwell Partners International, Inc.

- 6.4.13 Allegis Partners, LLC

- 6.4.14 True Talent Advisory, LLC (True Search)

- 6.4.15 N2Growth, Inc.

- 6.4.16 JM Search, Inc.

- 6.4.17 Kestria International (U.N.I. Partners s.r.o.)

- 6.4.18 ZSG (Executive Search) LLC

- 6.4.19 Lucas Group, a Korn Ferry Company

- 6.4.20 JMJ Phillip Holdings, Inc.

- 6.4.21 Egon Zehnder International AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment