PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035040

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035040

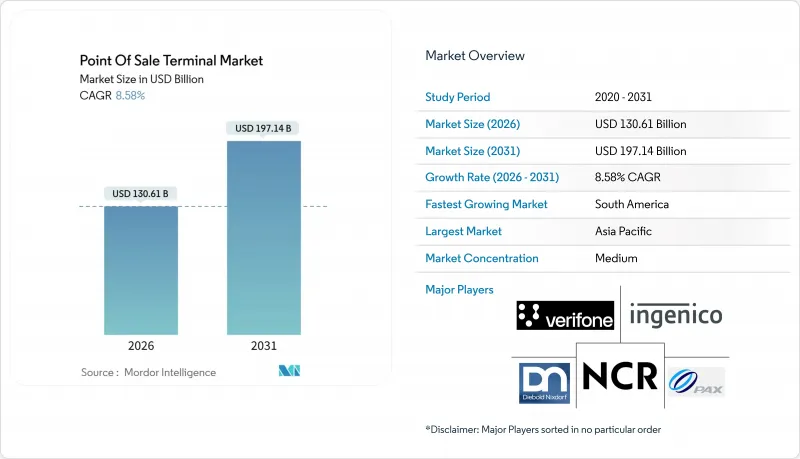

Point Of Sale Terminal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Point-of-Sale Terminal market size stood at USD 130.61 billion in 2026 and is projected to reach USD 197.14 billion by 2031, translating into an 8.58% CAGR during 2026-2031.

Demand is rising as governments legislate electronic invoicing, retailers orchestrate seamless omnichannel checkout, and healthcare providers accelerate digital billing. Hardware commoditization, cloud-native software, and embedded finance are reshaping vendor economics, while contactless acceptance and mobile wallets keep card-present payments relevant. Semiconductor supply-chain volatility is easing, yet cybersecurity standards such as PCI DSS v4.0 have lifted compliance costs. Competition is shifting toward software-centric platforms that monetize subscriptions rather than single-device sales, trimming margins for traditional hardware makers.

Global Point Of Sale Terminal Market Trends and Insights

Growing Adoption in the Retail Sector

Unified commerce initiatives allow store, online, and mobile purchases to clear through a single terminal interface, enabling stock sourced from store shelves to fulfill digital orders and trimming last-mile costs. Quick-service restaurants deploy self-service kiosks that marry payment with menu customization, cutting labor expenses and boosting basket size by presenting algorithmic add-ons. Grocery chains in Europe and North America piloted scan-and-go phone apps that let shoppers bypass staffed lanes, though theft controls and age-verification rules remain hurdles. Fashion stores equip associates with mobile devices that close sales on the showroom floor, slashing queue abandonment. Luxury retailers embed fingerprint readers to streamline identity confirmation for installment financing and loyalty redemption.

Rising Adoption of Cloud-based POS Platforms

Cloud architectures decouple processing logic from fixed hardware, so merchants retrieve transaction, stock, and customer data from any web device, a model that trims on-site IT costs. Automatic software updates end the expense of technician truck rolls, a boon to chains operating hundreds of terminals. Subscription pricing converts cap-ex to forecastable op-ex, making upgrades affordable for small businesses. Open application-programming-interfaces weave accounting, workforce scheduling, and marketing functions around the core payment flow, transforming terminals into business-management hubs. Continuous cloud backup improves disaster recovery, and provider-level PCI compliance shifts audit complexity away from individual merchants.

Data-Security and Cyber-fraud Concerns

Malware that scrapes volatile memory can snatch raw card data before encryption if firmware patches lag, keeping terminals an attractive attack vector. PCI DSS penalties may reach USD 500,000 per breach and prolonged non-compliance can lead to terminated processing privileges. Small businesses often lack cybersecurity staff, so outdated software persists. Tokenization and point-to-point encryption curb risk, yet hardware and acquirer upgrades impose costs that deter adoption. Europe's Digital Operational Resilience Act now forces payment providers to report incidents within 24 hours, lifting compliance budgets.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Demand for Contactless and Mobile Payments

- Integration of POS Data with Advanced Analytics and CRM

- Hardware Reliability and Maintenance-cost Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contact-based terminals accounted for 71.23% of the Point-of-Sale Terminal market revenue in 2025, a legacy of chip-and-PIN rollouts following global liability shifts. High-ticket merchants still favor the added security of PIN verification. Contactless acceptance is scaling at a 9.32% CAGR through 2031, fueled by tap-and-go convenience and government incentives that penalize cash-heavy operations. Transit agencies, convenience stores, and quick-service restaurants lead adoption because faster throughput trims queue times.

Hybrid devices accepting both contact and contactless are becoming standard, as a near-field antenna adds only USD 2-3 to the bill of materials. In the Asia-Pacific region, static quick-response codes further diversify checkout options, allowing merchants to forgo costly hardware. Early pilots of biometric authentication, fingerprint and facial recognition, are underway in luxury retail and hospital pharmacies to accelerate identity proofing.

Fixed countertop systems still accounted for 54.42% of the Point-of-Sale Terminal market in 2025, buoyed by grocery chains and pharmacies that process high transaction volumes at staffed stations. Integrated scanners and cash drawers maximize cashier efficiency where space and power are plentiful. Mobile and portable units, however, are advancing at a 9.67% CAGR, enticing food trucks, repair technicians, and outdoor vendors that require payment anywhere service is delivered.

Tablet-based systems dominate upscale restaurants, allowing servers to split checks and process payments tableside, reducing table turns and boosting tip percentages. Wearable forms such as wristbands and rings are trialed at festivals and stadiums, though limited battery life keeps usage niche. Ruggedized handhelds serve warehouses and courier fleets, marrying inventory scanning with payment collection under harsh conditions.

The Point of Sale Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based, and Contactless), POS Type (Fixed Point-Of-Sale Systems, and Mobile/Portable Point-Of-Sale Systems), Component (Hardware, Software, and Services), Deployment Mode (Cloud-Based, and On-Premise), and End-User Industry (Retail, Hospitality, Healthcare, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivered 40.52% of 2025 turnover, anchored by China's vast merchant base and India's Unified Payments Interface. China's shift from QR codes to contactless near-field communication is accelerating as global wallets compete for traffic. India's tax digitization push lifted terminal density, though rural adoption lags due to connectivity and fee sensitivity. Japan's aging demography tempers mobile uptake yet the 2025 Osaka Expo spurred hospitality upgrades. South Korea serves as a sandbox for biometric settlement trials, while Indonesia, Thailand, and Vietnam lean on omnichannel platforms to mesh e-commerce with storefronts.

Europe is in a replacement cycle triggered by fiscalization edicts such as the VAT in the Digital Age plan and Germany's Kassensicherungsverordnung. Certified security modules raise hardware costs but give tax agencies real-time visibility. The United Kingdom's post-Brexit divergence forces retailers to juggle distinct device configurations. Nordic countries are nearing cashless status, reducing demand for hybrid cash-card terminals, while EU accession is spurring infrastructure modernization in Eastern Europe.

North America is mature yet innovation-rich. Integrated platforms from Square and Toast displace legacy vendors by bundling payroll, analytics, and loyalty. State-level tax variation and patchwork privacy rules create compliance complexity that favors automated software. Canada's real-time rails improve cash flow for merchants, while Mexico's expanded e-invoicing mandate pushes micro-businesses toward certified devices despite uneven rural enforcement.

South America is the fastest riser at a predicted 10.18% CAGR, led by Brazil's Nota Fiscal Eletronica, which fines non-compliant merchants in real time. Argentina's inflation pushes consumers toward installment card plans, expanding electronic acceptance. Chile and Colombia are drafting similar fiscal frameworks, opening regional opportunities for vendors with service coverage. The Middle East and Africa remain nascent, but mobile money in Kenya and Nigeria is laying alternative rails that may leapfrog conventional terminals.

- Ingenico SA (Worldline)

- VeriFone Systems Inc.

- PAX Technology Ltd.

- NCR Corporation

- Diebold Nixdorf Inc.

- Toshiba Global Commerce Solutions

- HP Inc.

- Panasonic Corporation

- Fujitsu Ltd.

- Samsung Electronics Co. Ltd.

- Newland Payment Technology

- BBPOS Ltd.

- Square Inc. (Block)

- Fiserv Inc. (Clover)

- Lightspeed Commerce Inc.

- Shopify Inc. (Shopify POS)

- Toast Inc.

- Revel Systems Inc.

- Oracle Corporation (MICROS)

- Agilysys Inc.

- Aptos Inc.

- GK Software SE

- NEC Corporation

- NEXGO (Shenzhen Xinguodu Technology)

- Qashier Pte Ltd.

- Cegid Group

- Cow Hills Retail BV

- PCMS Group Ltd.

- SumUp Payments Limited

- Adyen N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption in the Retail Sector

- 4.2.2 Rising Adoption of Cloud-based POS Platforms

- 4.2.3 Accelerating Demand for Contactless and Mobile Payments

- 4.2.4 Integration of POS Data with Advanced Analytics and CRM

- 4.2.5 Regulatory Push for Fiscalisation and E-invoicing Mandates

- 4.2.6 Subscription-based "POS-as-a-Service" Models Lowering Cap-Ex

- 4.3 Market Restraints

- 4.3.1 Data-Security and Cyber-fraud Concerns

- 4.3.2 Hardware Reliability and Maintenance-cost Issues

- 4.3.3 Fragmentation of Regional Payment Standards

- 4.3.4 Semiconductor Supply-chain Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (IoT, AI, Edge-processing)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Deployment Mode

- 5.4.1 Cloud-based

- 5.4.2 On-Premise

- 5.5 By End-User Industry

- 5.5.1 Retail

- 5.5.2 Hospitality

- 5.5.3 Healthcare

- 5.5.4 Transportation and Logistics

- 5.5.5 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Italy

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Ingenico SA (Worldline)

- 6.4.2 VeriFone Systems Inc.

- 6.4.3 PAX Technology Ltd.

- 6.4.4 NCR Corporation

- 6.4.5 Diebold Nixdorf Inc.

- 6.4.6 Toshiba Global Commerce Solutions

- 6.4.7 HP Inc.

- 6.4.8 Panasonic Corporation

- 6.4.9 Fujitsu Ltd.

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 Newland Payment Technology

- 6.4.12 BBPOS Ltd.

- 6.4.13 Square Inc. (Block)

- 6.4.14 Fiserv Inc. (Clover)

- 6.4.15 Lightspeed Commerce Inc.

- 6.4.16 Shopify Inc. (Shopify POS)

- 6.4.17 Toast Inc.

- 6.4.18 Revel Systems Inc.

- 6.4.19 Oracle Corporation (MICROS)

- 6.4.20 Agilysys Inc.

- 6.4.21 Aptos Inc.

- 6.4.22 GK Software SE

- 6.4.23 NEC Corporation

- 6.4.24 NEXGO (Shenzhen Xinguodu Technology)

- 6.4.25 Qashier Pte Ltd.

- 6.4.26 Cegid Group

- 6.4.27 Cow Hills Retail BV

- 6.4.28 PCMS Group Ltd.

- 6.4.29 SumUp Payments Limited

- 6.4.30 Adyen N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment