PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035049

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035049

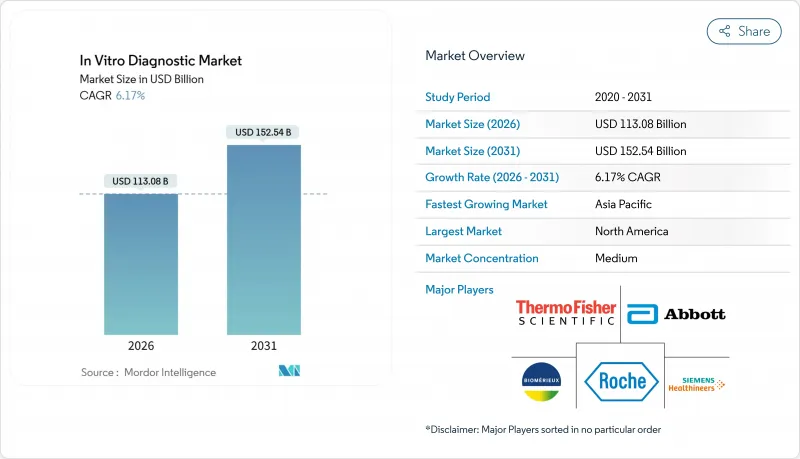

In Vitro Diagnostic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The In Vitro Diagnostic Market size is estimated at USD 113.08 billion in 2026, and is expected to reach USD 152.54 billion by 2031, at a CAGR of 6.17% during the forecast period (2026-2031).

Chronic disease prevalence, an aging global population, and artificial intelligence workflows now drive demand more sustainably than the pandemic surge. Laboratories are investing in cloud-based middleware, bundled reagent rental contracts, and integrated automation to contain labor costs and shorten turnaround times. Competitive pressure from ISO 13485-certified regional suppliers is compressing reagent margins, prompting multinationals to emphasize service bundles and decision-support software. Regulatory fragmentation, workforce shortages, and cybersecurity vulnerabilities remain structural headwinds; however, rising test volumes in the Asia-Pacific region and the increasing number of decentralized sites offset these constraints.

Global In Vitro Diagnostic Market Trends and Insights

Expanding Adoption of Point-of-Care (POC) Diagnostics

Regulators expanded CLIA-waived categories in 2024 and 2025, allowing pharmacies and employer clinics to perform rapid strep, influenza, and lipid panels without requiring laboratory staff. Retail chains such as CVS Health and Walgreens now capture routine tests that once flowed to reference labs, forcing central facilities to specialize in esoteric sequencing and autoimmune panels. FDA clearance of Dexcom's over-the-counter continuous glucose monitor in 2024 demonstrated that consumer electronics firms can bypass legacy infrastructure entirely. Handheld immunoassay readers and smartphone-linked lateral-flow devices meet hospital-grade precision, narrowing the performance gap that protected central labs. This decentralization boosts test access but squeezes reagent volumes in high-margin hospital settings.

High Prevalence of Chronic Diseases

Diabetes, cardiovascular disease, and chronic kidney disease drove 1.3 billion diagnostic procedures in 2025, straining global laboratory capacity. Diabetes prevalence climbed to 537 million adults in 2024, with the fastest growth in South Asia and the Middle East. Each chronic-care patient requires serial lipid, troponin, and kidney-function assays, raising consumable demand even as reimbursement remains flat. Wearable biosensors now continuously stream glucose and lactate data, shifting some monitoring from venipuncture to cloud analytics. Vendors, therefore, bundle laboratory reporting with longitudinal analytics subscriptions to preserve revenue even as traditional consumable sales plateau.

Stringent Multi-Region Regulatory Approval Timelines

The European Union's IVD Regulation, fully enforced in May 2024, transitioned thousands of low-risk assays from self-certification to notified-body review, resulting in a median approval time of 22 months. Japan and China impose parallel data requirements, adding 18 to 24 months before multinational launches reach the Asia region. Small innovators lack the regulatory manpower to run simultaneous trials, so they prioritize the United States first, ceding early share abroad. Staggered launches delay global scale and allow fast-follower rivals to secure reimbursement ahead of pioneers, marginally shaving the in vitro diagnostic market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Boosting Chronic Disease Testing Volumes

- Growing Infectious-Disease Burden Fueling Rapid Diagnostics

- Reimbursement Uncertainty Across Emerging Test Classes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits accounted for 54.28% of 2025 revenue, underscoring the consumable-based economics that sustain most laboratories. Hospitals favor reagent-rental agreements that waive analyzer acquisition costs in exchange for multi-year consumable purchases, a model that smooths vendor revenue. Software and services are forecast to post a 10.29% CAGR through 2031, powered by AI decision-support, cloud-hosted middleware, and remote instrument diagnostics. Instruments remain vital as lock-in platforms; Siemens Healthineers' Atellica Solution processes 440 tests per hour and auto-verifies 85% of results, saving labor minutes per report. The in vitro diagnostic market size for software is currently small, but its double-digit trajectory signals a shift by laboratories toward analytics and compliance outsourcing.

Software now decouples from hardware under the FDA's Software-as-a-Medical-Device framework, enabling independent algorithm upgrades. Vendors differentiate by pairing cloud dashboards with quality-control materials, creating sticky ecosystems. As capital budgets tighten, revenue from reagent rental and subscription-based software will rise faster than hardware placements, reshaping vendor profit pools within the in vitro diagnostic market.

Immunoassay retained a 26.63% revenue share in 2025, driven by thyroid, cardiac, and tumor markers. Yet, molecular diagnostics are projected to expand at an 8.21% CAGR, driven by liquid biopsy approvals, CRISPR assays, and syndromic infectious disease panels. Clinical chemistry automation has commoditized metabolic panels, so vendors now differentiate themselves through faster throughput and middleware integration rather than reagent chemistry. Hematology platforms incorporate AI-based cell classification, while microbiology shifts from culture to MALDI-TOF for rapid identification in 15 minutes.

Technology convergence is blurring legacy silos; next-generation platforms combine immunoassay, molecular techniques, and mass spectrometry on a single track. Laboratories welcome consolidated workflows that reduce sample handling, minimize error risk, and contain labor costs. As these hybrid systems scale, the in vitro diagnostic market will shift toward multi-modal analyzers that integrate AI-driven sample triage, increasing switching costs and solidifying vendor relationships.

The in Vitro Diagnostic Market Report is Segmented by Product Type (Instruments, Reagents & Kits, Software & Services), Technology (Immunoassay, Clinical Chemistry, Molecular Diagnostics, and More), Application (Infectious Diseases, Oncology, Diabetes, and More), End User (Hospitals & Academic Labs, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 37.16% of the 2025 revenue, supported by early adoption of molecular diagnostics and robust reimbursement. CMS value-based-care models now tie laboratory utilization to bundled payments, pressuring providers to limit low-value testing. FDA cybersecurity mandates increase compliance costs but improve data integrity. Canada and Mexico consolidate testing into regional hubs to capture scale economies.

The Asia-Pacific region is forecast to post a 7.19% CAGR from 2026 to 2031, the fastest regional pace. China's volume-based procurement slashed reagent prices by up to 60%, yet soaring volumes protect vendor revenue. India's National Health Mission funded 5,000 district labs in 2024-25, increasing per-capita test penetration from 0.08 to 0.15 tests per capita annually. Aging Japan and South Korea are automating aggressively to offset labor shortages, resulting in increased capital expenditure on total laboratory automation.

Europe enforces the IVD Regulation, extending approval timelines and favoring multinationals with seasoned regulatory teams. GCC states channel oil revenue into laboratory infrastructure under Vision 2030. Sub-Saharan Africa remains under-penetrated but benefits from donor-funded HIV, tuberculosis, and malaria programs. South American laboratories struggle with currency fluctuations and import tariffs, sourcing reagents locally whenever possible to manage costs.

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- Bio-Rad Laboratories

- bioMerieux

- Danaher

- DiaSorin

- Roche

- GE Healthcare

- Grifols

- Hologic

- Illumina

- Meril Diagnostics Pvt Ltd

- Ortho Clinical Diagnostics / QuidelOrtho

- PerkinElmer

- QIAGEN

- QuidelOrtho

- Randox Laboratories

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Adoption of Point-of-Care (POC) Diagnostics

- 4.2.2 High Prevalence of Chronic Diseases

- 4.2.3 Aging Population Boosting Chronic Disease Testing Volumes

- 4.2.4 Growing Infectious-Disease Burden Fueling Rapid Diagnostics

- 4.2.5 Surge in Decentralized Point-of-Care (POC) Testing

- 4.2.6 Lab Automation & Digital Pathology Convergence Drives Bundled IVD Procurement

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Region Regulatory Approval Timelines

- 4.3.2 Reimbursement Uncertainty Across Emerging Test Classes

- 4.3.3 Cyber-Security & Data-Interoperability Gaps in Connected IVD

- 4.3.4 Global Shortage of Skilled Lab Technologists

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Reagents & Kits

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 Immunoassay

- 5.2.2 Clinical Chemistry

- 5.2.3 Molecular Diagnostics

- 5.2.4 Hematology

- 5.2.5 Microbiology

- 5.2.6 Coagulation

- 5.2.7 Urinalysis

- 5.2.8 Others

- 5.3 By Application

- 5.3.1 Infectious Diseases

- 5.3.2 Oncology

- 5.3.3 Diabetes

- 5.3.4 Cardiology

- 5.3.5 Autoimmune Diseases

- 5.3.6 Nephrology

- 5.3.7 Others

- 5.4 By End User

- 5.4.1 Hospitals & Academic Labs

- 5.4.2 Reference Laboratories

- 5.4.3 Point-of-Care Testing Sites

- 5.4.4 Homecare/OTC Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Bio-Rad Laboratories Inc.

- 6.3.5 bioMerieux SA

- 6.3.6 Danaher Corporation

- 6.3.7 DiaSorin SpA

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 GE Healthcare

- 6.3.10 Grifols SA

- 6.3.11 Hologic Inc.

- 6.3.12 Illumina Inc.

- 6.3.13 Meril Diagnostics Pvt Ltd

- 6.3.14 Ortho Clinical Diagnostics / QuidelOrtho

- 6.3.15 PerkinElmer Inc.

- 6.3.16 Qiagen NV

- 6.3.17 QuidelOrtho Corporation

- 6.3.18 Randox Laboratories Ltd

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Sysmex Corporation

- 6.3.21 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment