PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035060

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035060

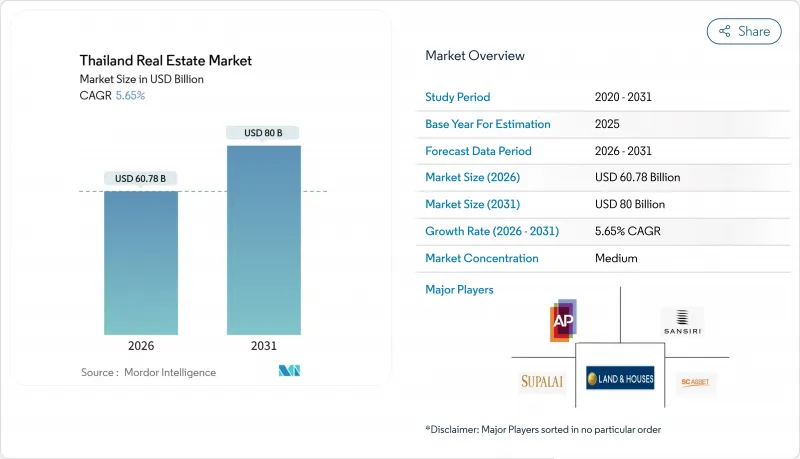

Thailand Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Thailand real estate market size is estimated at USD 60.78 billion in 2026 and is expected to reach USD 80.00 billion by 2031, growing at a 5.65% CAGR during 2026 to 2031.

The 2026 inflection reflects pressure from weak mid-income purchasing power, high household debt, and tighter underwriting, while public infrastructure projects, targeted government stimulus, and foreign capital in luxury and logistics help sustain activity in select corridors. Developers listed in Bangkok are shifting toward logistics and industrial assets within the Eastern Economic Corridor, where demand links to e-commerce and data center investments. Government measures such as fee cuts on property transfers and loan-to-value relaxations are intended to clear transactions at the margin, even as banks maintain prudent credit standards due to balance sheet risks. Monetary easing since August 2025 and mass transit additions around the MRT Orange Line are expected to improve sentiment and stabilize transfer volumes into mid-2026 as project timelines progress.

Thailand Real Estate Market Trends and Insights

Transit expansion and infrastructure upgrades

Transit additions are shaping how demand forms across Bangkok's core and periphery in 2026. New mass-transit lines improve accessibility and are expected to lift values and absorption near stations as construction progresses in the 2026 to 2027 window. The Bangkok to Nakhon Ratchasima high-speed rail, slated to open in 2028, also supports land assembly and planning activity in secondary cities that benefit from future connectivity. Early data on the Pink Line's launch showed a burst of transfers followed by softer absorption in mid-priced suburban condominiums, which signals that station proximity alone does not guarantee sustained take-up without strong job anchors nearby. Developers are increasing focus on transit-proximate, lower-rise projects priced below THB 10 million (USD 285,714), targeting owner-occupiers who value safety, access, and resilience. This selective transit-oriented strategy favors corridors that pair mobility gains with employment density and livability improvements, rather than transit alignment alone.

Government incentives and fee cuts

Fiscal and macroprudential steps are supporting transactions, but cannot fully offset household debt constraints. Authorities reduced transfer and mortgage registration fees to 0.01% for homes priced up to THB 7 million (USD 200,000), which is expected to lift near-term transaction counts but does not resolve credit screening hurdles for mid-income buyers. The loan-to-value relaxation to 100% for second homes priced below THB 10 million (USD 285,714) was designed to stimulate upper mid-market demand, yet bank underwriting remains cautious in segments exposed to high rejection rates. Developers postponed some planned projects in 2025 as presales fell short of targets, while luxury units maintained stronger absorption, underscoring liquidity concentration at the top end. Subsidized housing programs expand access and create price reference points, but private developers still face margin pressure in overlapping catchments. New responsible lending rules effective January 2025, including preemptive debt restructuring guidelines, acknowledge that fee cuts alone will not revive mass-market demand without household balance sheet repair.

Weak mid-income housing demand amid high debt

Household debt levels and prudent underwriting are suppressing approval rates for homes priced below THB 3 million (USD 85,714). Rising non-performing and special mention loans have led banks to formalize affordability testing and residual income thresholds under responsible lending rules introduced in January 2025. High rejection rates for lower-priced homes raise inventory carry and discount pressure for developers focused on mid-income segments. Developers have experimented with rent-to-own and seller financing to convert the pipeline, which shifts credit risk back to corporate balance sheets. New housing launches were curtailed in 2025 as firms recalibrated exposure to the most credit-constrained demand pools. Structural affordability will remain a constraint until income growth and household deleveraging improve debt service metrics in this price band.

Other drivers and restraints analyzed in the detailed report include:

- Rising foreign buyer interest

- Logistics Demand Absorbing EEC Industrial Land Faster Than Residential Recovers

- Urban condo oversupply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential properties were the largest by revenue with a 52.4% share in 2025, indicating the balance of consumer demand within the Thailand real estate market. Commercial assets are advancing as the fastest-growing segment at a 6.22% CAGR during 2026 to 2031 as data center approvals and logistics expansion in the EEC attract new capital allocations. The Board of Investment cleared a wave of digital infrastructure and related investments in 2024 to 2025, including multi-billion-dollar commitments that anchor industrial estate leasing and power procurement strategies. This cycle raises the importance of power availability and zoning near hyperscale sites and has prompted listed developers to build warehousing capacity consistent with institutional-grade tenancy. Apartments and condominiums still hold the largest share within residential, while detached houses are benefiting from buyer preference for more space and safety in outer Bangkok zones.

Hospitality shows steady recovery on the back of tourism, with operators emphasizing asset enhancements and mixed-use integration to improve earnings durability. Office fundamentals are mixed in 2026 as Grade A vacancy remains elevated during a flight to quality, with ESG-certified towers gaining relative strength while secondary assets deploy concessions and upgrades. Retail assets in prime locations continue to attract tenants, though e-commerce competition keeps pressure on formats that do not provide experiential value. Logistics warehouse occupancy and rents are supported by e-commerce and cold chain requirements, with REIT demand providing additional liquidity and development pipeline certainty. Against this backdrop, commercial momentum is expected to remain the outlier for the Thailand real estate market through 2031 based on anchor tenant demand and financing models suited to long leases.

The Thailand Real Estate Market Report is Segmented by Property Type (Residential and Commercial), by Business Model (Sales and Rental), by End User (Individuals/Households, Corporates & SMEs and Others), and by Major Cities (Bangkok, Phuket, and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- AP (Thailand) PCL

- Sansiri PCL

- Supalai PCL

- Land and Houses PCL

- SC Asset Corporation PCL

- Pruksa Holding PCL

- Origin Property PCL

- Ananda Development PCL

- Quality Houses PCL

- L.P.N. Development PCL

- Noble Development PCL

- Central Pattana PCL

- Asset World Corporation PCL

- WHA Corporation PCL

- Frasers Property (Thailand) PCL

- Amata Corporation PCL

- Siam Piwat Co., Ltd.

- Raimon Land PCL

- Magnolia Quality Development Corporation (MQDC)

- Minor International PCL

- Central Plaza Hotel PCL (CENTEL)

- Erawan Group PCL

- Dusit Thani PCL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Overview of the Economy and Market

- 4.2 Real Estate Buying Trends - Socioeconomic and Demographic Insights

- 4.3 Rental Yield Analysis

- 4.4 Capital-Market Penetration & REIT

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into Real Estate Tech and Startups Active in the Real Estate Segment

- 4.8 Insights into Existing and Upcoming Projects

- 4.9 Market Drivers

- 4.9.1 Transit expansion and infrastructure upgrades are boosting urban and suburban property demand.

- 4.9.2 Government incentives and fee cuts are stimulating housing sales and new project launches.

- 4.9.3 Growing foreign buyer interest supports condo sales in key tourism and business zones.

- 4.9.4 E-commerce growth and supply chain shifts are driving demand for logistics and industrial assets.

- 4.9.5 Large mixed-use developments are attracting capital and reshaping city real estate clusters.

- 4.9.6 Limited premium supply and rising build costs are sustaining prices in prime locations.

- 4.10 Market Restraints

- 4.10.1 Weak mid-income housing demand due to high household debt and tighter credit rules.

- 4.10.2 Condo oversupply in urban areas is leading to slower absorption and price stagnation.

- 4.10.3 Planning delays and zoning issues are disrupting project timelines and approvals.

- 4.10.4 Economic uncertainty and inflation are lowering buyer confidence and investment activity.

- 4.11 Value/Supply-Chain Analysis

- 4.11.1 Overview

- 4.11.2 Real estate developers & Contractors - key quantitative and qualitative insights

- 4.11.3 Real estate brokers and agents - key quantitative and qualitative insights

- 4.11.4 Property management companies - key quantitative and qualitative insights

- 4.11.5 Insights on Valuation Advisory and Other Real Estate Services

- 4.11.6 State of the building materials industry and partnerships with key developers

- 4.11.7 Insights on key strategic real estate investors/buyers in the market

- 4.12 Porter's Five Forces

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Buyers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes

- 4.12.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value,USD billion)

- 5.1 Sales

- 5.2 Rental

6 Sales Mode Market Size & Growth Forecasts (Value, USD billion)

- 6.1 By Property Type

- 6.1.1 Residential

- 6.1.1.1 Apartments & Condominiums

- 6.1.1.2 Villas & Landed Houses

- 6.1.2 Commercial

- 6.1.2.1 Office

- 6.1.2.2 Retail

- 6.1.2.3 Logistics

- 6.1.2.4 Others

- 6.1.1 Residential

- 6.2 By End-user

- 6.2.1 Individuals / Households

- 6.2.2 Corporates & SMEs

- 6.2.3 Others

- 6.3 By Major Cities

- 6.3.1 Bangkok

- 6.3.2 Phuket

- 6.3.3 Pattaya

- 6.3.4 Chiang Mai

- 6.3.5 Rest of Thailand

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 7.4.1 AP (Thailand) PCL

- 7.4.2 Sansiri PCL

- 7.4.3 Supalai PCL

- 7.4.4 Land and Houses PCL

- 7.4.5 SC Asset Corporation PCL

- 7.4.6 Pruksa Holding PCL

- 7.4.7 Origin Property PCL

- 7.4.8 Ananda Development PCL

- 7.4.9 Quality Houses PCL

- 7.4.10 L.P.N. Development PCL

- 7.4.11 Noble Development PCL

- 7.4.12 Central Pattana PCL

- 7.4.13 Asset World Corporation PCL

- 7.4.14 WHA Corporation PCL

- 7.4.15 Frasers Property (Thailand) PCL

- 7.4.16 Amata Corporation PCL

- 7.4.17 Siam Piwat Co., Ltd.

- 7.4.18 Raimon Land PCL

- 7.4.19 Magnolia Quality Development Corporation (MQDC)

- 7.4.20 Minor International PCL

- 7.4.21 Central Plaza Hotel PCL (CENTEL)

- 7.4.22 Erawan Group PCL

- 7.4.23 Dusit Thani PCL

8 Market Opportunities & Future Outlook

- 8.1 White-space & unmet-need assessment