PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035070

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035070

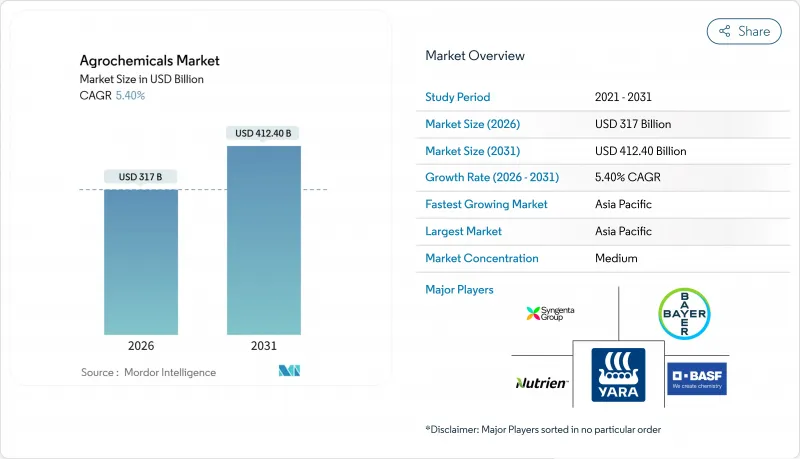

Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The agrochemicals market size is estimated to be USD 317.00 billion in 2026 and is forecast to reach USD 412.40 billion by 2031, reflecting a 5.40% CAGR.

This growth is driven not only by volume increases but also by a shift toward premium herbicides that address resistant weeds and regulatory measures phasing out high-toxicity chemicals. These trends are steering investments toward controlled-release fertilizers and advanced crop protection solutions. Initiatives such as Nutrien's carbon-aligned nitrogen program and Yara's green ammonia projects underscore the rising importance of combining product performance with sustainability compliance. Additionally, factors like carbon pricing, pesticide taxes, and stricter residue limits are reshaping product pipelines, favoring coated fertilizers that enable verified emission credits. However, litigation risks and re-registration costs are narrowing product portfolios, increasing entry barriers, and benefiting diversified companies capable of managing compliance costs effectively.

Global Agrochemicals Market Trends and Insights

Rising Incidence of Herbicide-Resistant Weeds Fuels Demand for Premium Herbicides

Palmer amaranth infestations now span 31 United States states, and glyphosate-resistant ryegrass covers more than 2 million hectares in Australia. Growers are substituting generic glyphosate with premium Group 15 and Group 27 chemistries, commanding 40-60% price uplifts. Revenue per treated hectare is rising even as acreage stays flat, rewarding portfolios that rotate multiple modes of action within a season. Trait-herbicide bundles such as Corteva's Enlist E3 soybean, which reached 35% of U.S. soybean acres in 2025, illustrate how integrated solutions secure recurring sales and temper resistance evolution. Regulators are tightening stewardship rules that formalize rotation and refuge planting, increasing demand for multi-site chemistry access. Growers, therefore, prioritize suppliers able to deliver complete resistance-management programs.

Precision Agriculture and Data Subscription Models Scale Globally

Input-as-a-Service contracts convert one-time input purchases into recurring revenue and data loops. Corteva's Granular platform guided 60 million acres in 2025, while Yara's Atfarm advised 1.2 million hectares in Europe, cutting nitrogen waste by 12% and spawning carbon credits priced at EUR 25 per metric ton (USD 27 per metric ton). Smartphone penetration in India and Indonesia is extending similar services to smallholders, and telematics are embedding Bayer's Climate FieldView across 4 million farms worldwide. Control of prescription data lets incumbents steer seed, fertilizer, and crop-protection mix, positioning platforms as profit centers equal in importance to active-ingredient pipelines.

Accelerating Phase-Outs of High-Toxicity Actives in the European Union, Brazil, and China

European Union proposals to retire 12 additional neonics and organophosphates by 2027, Brazil's reclassification of paraquat as "extremely toxic," and China's ban on 41 pesticide actives are shrinking registrant portfolios. Portfolio churn shortens effective patent lives for replacement molecules, forcing companies to accelerate product launches or pivot into biologicals to protect revenue. Smaller formulators, unable to fund reformulation, are exiting segments, further concentrating market power among diversified incumbents that can spread compliance costs.

Other drivers and restraints analyzed in the detailed report include:

- Controlled-Release and Inhibitor-Coated Fertilizers Gain Mainstream Adoption

- Carbon-Credit Monetization of Nitrogen-Efficiency Products

- Volatile Glyphosate Pricing Squeezes Formulator Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers dominated the agrochemicals market in 2025, holding 75% of revenue. Nitrogenous grades urea, ammonium nitrate, and Urea Ammonium Nitrate (UAN) solutions remain indispensable in cereal production across Asia-Pacific and North America. In contrast, plant growth regulators are forecast to post the fastest expansion at 13.0% CAGR, propelled by applications that synchronize flowering and extend shelf life in fruits and vegetables. Herbicides constitute a significant portion of pesticide value, reshaping product portfolios in regions with stringent zero-residue mandates. Adjuvants, though a small share, generate outsize strategic value because they reduce spray rates by up to 25%, preserving efficacy while easing regulatory pressure. Corteva Agriscience's ProGibb, a gibberellin-based regulator, recorded significant revenue in 2025, reflecting increasing demand for yield-enhancement molecules beyond traditional fertilizer expenditures. The agrochemicals market size for fertilizers is projected to grow steadily, with discretionary growth likely to center on high-margin regulators and other products that align with sustainability initiatives.

The ongoing phase-out of toxic active ingredients and the increasing preference for coated formulations enable companies to integrate fertilizer and crop protection solutions. Firms offering nutrient efficiency alongside pest control can cross-sell within the same acreage, strengthening relationships with channel partners and capturing additional market share. These trends allow agrochemical companies to maintain profitability despite fluctuations in commodity fertilizer cycles. Additionally, companies that validate environmental performance through third-party protocols are securing pricing premiums, indicating a long-term shift away from volume-based competition.

The Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Pesticides, and More), by Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Commercial Crops, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 53% of the agrochemicals market share in 2025 and is projected to grow at a CAGR of 6.6% through 2031. Key factors supporting baseline demand include China's zero-growth fertilizer mandate, which aims to stabilize fertilizer usage while maintaining agricultural productivity, and India's subsidized urea program, which ensures affordability for farmers and sustains demand. Additionally, Japan's precision agriculture platforms demonstrate how carbon monetization initiatives can incentivize the adoption of premium agricultural inputs, further driving market growth in the region. These developments position Asia-Pacific as a critical driver of the global agrochemicals market.

In Africa, digital advisory services are increasingly being adopted to enhance yields among smallholder farmers, addressing challenges such as restricted access to traditional inputs and climate variability. Egypt and South Africa stand out as anchor markets due to their well-developed irrigation infrastructure and focus on export-oriented horticulture, which supports higher-value crop production. Meanwhile, South America's market growth is primarily driven by Brazil's expanding soybean and corn acreage, supported by favorable climatic conditions and government policies, and Argentina's export-oriented agricultural practices, which emphasize competitiveness in global markets.

In North America, market growth reflects the challenges of mature acreage and the impact of litigation, yet advancements in data platforms and carbon programs are creating new service revenue opportunities for agrochemical companies. Europe's market growth is the slowest among regions, hindered by the Farm to Fork pesticide-reduction targets. However, the region is becoming a leader in adopting low-carbon fertilizers, supported by regulatory initiatives like the Carbon Border Adjustment Mechanism (CBAM). The Middle East is capitalizing on its low-cost natural gas resources to produce ammonia for export while actively exploring blue and green ammonia production pathways. These regional trends highlight that while Asia-Pacific dominates in absolute sales, Africa and South America offer significant growth opportunities, shaping expansion strategies in the agrochemicals market.

- Syngenta Group

- Bayer AG

- BASF SE

- Corteva Agriscience

- Nutrien Ltd.

- Yara International ASA

- Mosaic Company

- CF Industries Holdings Inc.

- UPL Ltd.

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Ltd.

- K+S Aktiengesellschaft

- ICL Group

- OCP Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Herbicide-Resistant Weeds Fuels Demand for Premium Herbicides

- 4.2.2 Precision Agriculture and Data Subscription Models Scale Globally

- 4.2.3 Major Pesticide Patent Cliff (2024-2028) Fuels Low-Cost Generic Uptake

- 4.2.4 Carbon-credit Monetization of Nitrogen-Efficiency Products

- 4.2.5 Controlled-release and Inhibitor-Coated Fertilizers Gain Mainstream Adoption

- 4.2.6 European Union Carbon Border Adjustment Mechanism (CBAM) and Similar Carbon Policies Accelerate Low-Carbon Ammonia Uptake

- 4.3 Market Restraints

- 4.3.1 Accelerating Phase-outs of High-toxicity Actives in the European Union, Brazil, and China

- 4.3.2 Volatile Glyphosate Pricing Squeezes Formulator Margins

- 4.3.3 Rising Regulatory Data-package and Re-registration Costs

- 4.3.4 Chronic Activist Litigation Risk in North America

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Fertilizers

- 5.1.1.1 Nitrogenous

- 5.1.1.2 Phosphatic

- 5.1.1.3 Potassic

- 5.1.1.4 Other Fertilizers

- 5.1.2 Pesticides

- 5.1.2.1 Herbicides

- 5.1.2.2 Insecticides

- 5.1.2.3 Fungicides

- 5.1.2.4 Other Pesticides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.1.1 Fertilizers

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamental

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva Agriscience

- 6.4.5 Nutrien Ltd.

- 6.4.6 Yara International ASA

- 6.4.7 Mosaic Company

- 6.4.8 CF Industries Holdings Inc.

- 6.4.9 UPL Ltd.

- 6.4.10 FMC Corporation

- 6.4.11 Sumitomo Chemical Co., Ltd.

- 6.4.12 Nufarm Ltd.

- 6.4.13 K+S Aktiengesellschaft

- 6.4.14 ICL Group

- 6.4.15 OCP Group

7 Market Opportunities and Future Outlook