PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035083

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035083

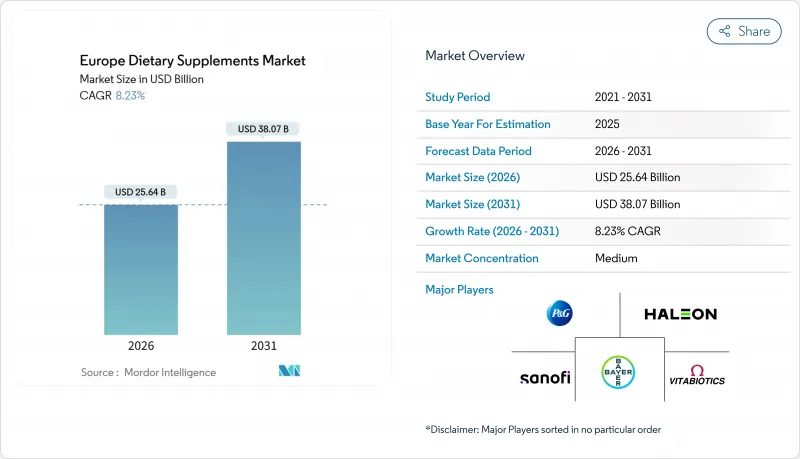

Europe Dietary Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The European dietary supplements market size is valued at USD 25.64 billion in 2026 and is forecast to reach USD 38.07 billion by 2031, expanding at an 8.23% CAGR.

This growth is driven by several key factors, including an aging population, an increasing gap in micronutrient intake, and the implementation of clear regulatory policies under Directive 2002/46/EC, which collectively sustain long-term demand. Additionally, the expansion of online retail channels, the introduction of innovative supplement formats, and the rising trend of personalized nutrition are further broadening the market's consumer base. Vitamins and minerals continue to dominate as the leading segment, supported by national campaigns aimed at reducing deficiencies and promoting daily supplementation. However, the fastest growth in volume is observed in gummies and subscription-based e-commerce models, which cater to evolving consumer preferences for convenience and novelty. Despite the challenges posed by fragmented country-level regulations that complicate product registration and labeling, pharmacies in countries like Italy and Germany remain trusted distribution channels, particularly for clinically focused brands. Efforts to suppress counterfeit products and the European Food Safety Authority's (EFSA) stricter reviews of health claims may temper overall market growth. However, these measures also create opportunities for companies that can demonstrate the authenticity of their ingredients and provide clinical evidence of their products' efficacy, thereby gaining a competitive edge in the market.

Europe Dietary Supplements Market Trends and Insights

Preventive healthcare trends are driving regular supplement consumption

European health systems dedicate a smaller share of their total health expenditure to preventive measures. Consequently, consumers are increasingly relying on self-directed supplementation to address this gap. This trend is particularly prominent in markets with high out-of-pocket healthcare expenses and prolonged waiting times for specialist care, where supplements are perceived as a convenient alternative to pharmaceuticals. The European Commission's 2024 State of Health in the European Union report revealed that 23% of adults aged 65 and older are at risk of malnutrition . This risk is fueling greater demand for fortified multivitamins and protein supplements. National initiatives, such as the United Kingdom's vitamin D supplementation guidance for at-risk groups, are both legitimizing regular supplement use and positioning preventive nutrition as an essential public health measure. Furthermore, Germany's Federal Institute for Risk Assessment has issued updated tolerable upper intake levels for micronutrients. These evidence-based dosing guidelines aim to reduce consumer concerns about long-term supplementation.

Supplements targeting women consumers fueling growth

Women's health supplements have shifted their focus from solely prenatal care to addressing a broader range of concerns, including menopause, hormonal balance, skin elasticity, and bone density, areas often neglected by pharmaceutical companies. Highlighting the growing investor interest in the menopause supplement market, Venture Life Group acquired Health and Her Limited for GBP 7.5 million (USD 9.5 million) in October 2024. This market stands out due to its longer treatment durations and higher per-capita spending compared to general wellness products. In 2025, the European Medicines Agency clarified labeling requirements for botanical substances in menopause products, reducing regulatory uncertainties for manufacturers. Additionally, France's ANSES approved specific health claims for calcium and vitamin D in postmenopausal women, setting a precedent likely to be followed by other European Union member states. Furthermore, women's demand for clean-label formulations and transparent sourcing is driving progress in organic certification and third-party testing protocols.

Presence of counterfeit products hampering the growth

Counterfeit supplements significantly undermine consumer trust and pose a serious risk to the reputations of legitimate manufacturers, particularly when adverse incidents occur. Online platforms, with third-party sellers on sites like Amazon and eBay, have emerged as major distribution channels for counterfeit products. Among these, weight-loss, bodybuilding, and sexual-enhancement supplements are the most frequently adulterated categories. To combat this issue, premium brands are increasingly adopting advanced authentication technologies such as blockchain-enabled traceability and DNA barcoding. However, the high costs associated with implementing these technologies remain a substantial barrier for smaller manufacturers. In response to these challenges, the European Commission has proposed extending pharmaceutical serialization requirements to high-risk supplement categories by 2025. While this initiative could help address the issue, industry groups have expressed concerns about the financial burden it may place on small and medium-sized enterprises (SMEs) in terms of compliance costs.

Other drivers and restraints analyzed in the detailed report include:

- Europe's aging population boosts demand for age-related supplements

- Consumers' inclination towards clean-label and natural supplements

- Scientific skepticism reduces consumer trust in unproven products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, vitamins and minerals dominated the market with a 51.31% share, and projections indicate an annual growth rate of 10.57% through 2031. This growth is largely attributed to heightened awareness campaigns about deficiencies and innovative bioavailability formulations. A case in point is DSM-Firmenich's April 2024 green light for calcidiol monohydrate, a vitamin D variant boasting enhanced absorption for the elderly. This move underscores the innovative momentum propelling this segment's dominance. Meanwhile, herbal supplements grapple with challenges. The EFSA's 2024 assessment flagged safety issues in 13 botanical substances, including turmeric and St. John's wort. This revelation has spurred reformulation initiatives and a more vigilant approach to ingredient sourcing. On another front, proteins and amino acids ride the wave of sports nutrition's popularity. Fatty acids, especially omega-3s, enjoy steady demand from consumers prioritizing cardiovascular health. Enzymes, though a niche, find their primary application in digestive health, catering to issues like lactose intolerance and pancreatic insufficiency.

The segment's expansion is anchored in the widespread prevalence of micronutrient deficiencies. For instance, vitamin D shortages are a concern for many Europeans, and iron deficiency anemia poses a significant challenge, especially for women of reproductive age. National supplementation initiatives, such as the United Kingdom's recommendations for vulnerable groups, bolster the legitimacy of routine vitamin consumption, ensuring a consistent demand. Postbiotics, which are metabolites from probiotic fermentation, are carving out a niche. They offer a potential solution to the regulatory ban on "probiotic" health claims. Manufacturers are now marketing these as innovative functional foods, stepping away from the traditional supplement label. The European Food Safety Authority, through its stringent health claims evaluation process under Regulation 1924/2006, guarantees that only robustly supported claims reach the public. However, this meticulous approach can stifle innovation and tends to benefit established players with the financial muscle to back clinical trials.

Tablets accounted for 27.85% of the market in 2025. However, gummies are the fastest-growing format, with an annual growth rate of 9.21% projected through 2031. This growth is driven by benefits such as taste masking, convenience, and their appeal to both pediatric and geriatric populations. Bayer's introduction of Berocca Multi-Action Gummies in the United Kingdom in December 2023, followed by a broader rollout in 2024, highlights how established brands are leveraging format innovation to meet rising demand. Advances in starchless depositing and pectin-based formulations have enabled the production of sugar-free gummies that comply with clean-label standards, addressing concerns about dental health and glycemic impact. Capsules and softgels remain popular for oil-soluble nutrients, such as omega-3s and fat-soluble vitamins, as gelatin or vegetarian shells protect these ingredients from oxidation. In sports nutrition, powders are preferred for their dose flexibility and rapid dissolution, while liquids cater to individuals with swallowing difficulties or those seeking faster absorption.

The growing preference for gummies reflects a broader consumer trend toward products that resemble confectionery rather than medicine, reducing psychological barriers to daily supplementation. However, gummies face formulation challenges; heat-sensitive nutrients like probiotics and certain vitamins can degrade during manufacturing, limiting the format's applicability. Regulatory scrutiny is also increasing, with some member states proposing restrictions on marketing gummies to children due to concerns about overconsumption. Tablets and capsules, supported by established manufacturing infrastructure and lower per-unit costs, continue to dominate in price-sensitive segments. The European Commission's ongoing review of food supplement labeling requirements may lead to standardized dosing guidelines, which could influence format choices, particularly for nutrients with narrow therapeutic windows.

The Europe Dietary Supplements Market Report is Segmented by Product Type (Vitamins and Minerals, Enzymes, Herbal, Proteins, and More), Form (Tablets, Capsules, Powders, Gummies, Liquids), Consumer Group (Men, Women, Children), Health Application (Wellness, Bone Health, Energy Management, Gut Health, and More), Distribution Channel (Supermarkets, and More), and Geography. Market Forecasts are in Value (USD) and Volume (Tons).

List of Companies Covered in this Report:

- Bayer AG

- Nestle S.A.

- Herbalife Nutrition Ltd.

- GlaxoSmithKline plc

- Procter and Gamble Company

- Perrigo Company plc

- Sanofi S.A.

- Reckitt Benckiser Group plc

- DSM-Firmenich AG

- Abbott Laboratories

- Orkla ASA

- BioGaia AB

- Lonza Group AG

- Probi AB

- Arkopharma Laboratories

- Pileje SAS

- Vitabiotics Ltd.

- Unilever plc (OLLY)

- H and H Group (Swisse)

- Pharma Nord ApS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Preventive healthcare trends are driving regular supplement consumption

- 4.2.2 Supplements targeting women consumers fueling growth

- 4.2.3 Consumers' inclination towards clean-label and natural supplements

- 4.2.4 Europe's aging population boosts demand for age-related supplements

- 4.2.5 The growing popularity of sports nutrition and fitness trends drives supplement use among younger consumers

- 4.2.6 E-Commerce expansion makes supplements more accessible and promotes market growth

- 4.3 Market Restraints

- 4.3.1 Presence of counterfeit products hampering the growth

- 4.3.2 Scientific skepticism reduce consumer trust in unproven products

- 4.3.3 Strict regulations limit health claims on supplements

- 4.3.4 Growing preference for natural food-based nutrition reduces reliance on supplements

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Vitamins and Minerals

- 5.1.2 Enzymes

- 5.1.3 Herbal Supplements

- 5.1.4 Proteins and Amino Acids

- 5.1.5 Fatty Acids

- 5.1.6 Probiotics

- 5.1.7 Other Product Types

- 5.2 By Form

- 5.2.1 Tablets

- 5.2.2 Capsules and Softgels

- 5.2.3 Powders

- 5.2.4 Gummies

- 5.2.5 Liquids

- 5.2.6 Other Forms

- 5.3 By Consumer Group

- 5.3.1 Men

- 5.3.2 Women

- 5.3.3 Kids/Children

- 5.4 By Health Application

- 5.4.1 General Health and Wellness

- 5.4.2 Bone and Joint Health

- 5.4.3 Energy and Weight Management

- 5.4.4 Gastrointestinal and Gut Health

- 5.4.5 Immunity Enhancement

- 5.4.6 Cardiovascular Health

- 5.4.7 Diabetes Management

- 5.4.8 Cognitive and Mental Health

- 5.4.9 Skin, Hair and Nail Care

- 5.4.10 Eye Health

- 5.4.11 Other Health Applications

- 5.5 By Distribution Channel

- 5.5.1 Supermarkets/Hypermarkets

- 5.5.2 Specialty Stores

- 5.5.3 Online Retail Channels

- 5.5.4 Direct Selling

- 5.5.5 Other Distribution Channels

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Sweden

- 5.6.8 Belgium

- 5.6.9 Poland

- 5.6.10 Netherlands

- 5.6.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Nestle S.A.

- 6.4.3 Herbalife Nutrition Ltd.

- 6.4.4 GlaxoSmithKline plc

- 6.4.5 Procter and Gamble Company

- 6.4.6 Perrigo Company plc

- 6.4.7 Sanofi S.A.

- 6.4.8 Reckitt Benckiser Group plc

- 6.4.9 DSM-Firmenich AG

- 6.4.10 Abbott Laboratories

- 6.4.11 Orkla ASA

- 6.4.12 BioGaia AB

- 6.4.13 Lonza Group AG

- 6.4.14 Probi AB

- 6.4.15 Arkopharma Laboratories

- 6.4.16 Pileje SAS

- 6.4.17 Vitabiotics Ltd.

- 6.4.18 Unilever plc (OLLY)

- 6.4.19 H and H Group (Swisse)

- 6.4.20 Pharma Nord ApS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK