PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035086

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035086

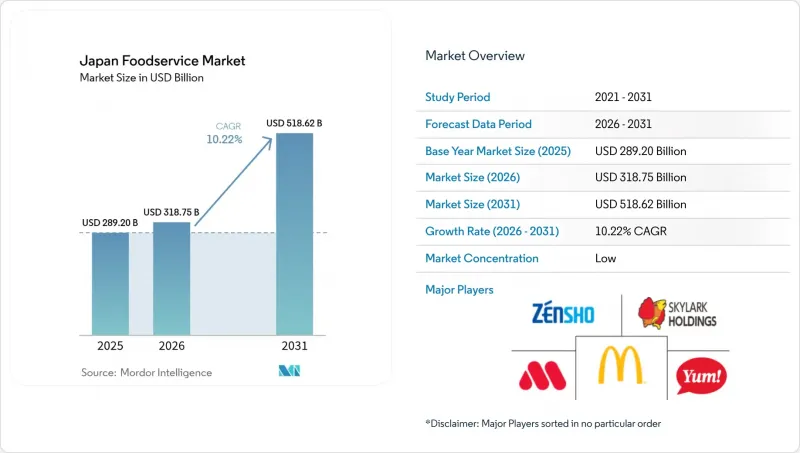

Japan Foodservice - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan Foodservice Market size was valued at USD 289.20 billion in 2025 and estimated to grow from USD 318.75 billion in 2026 to reach USD 518.62 billion by 2031, at a CAGR of 10.22% during the forecast period (2026-2031).

This exceptional growth trajectory reflects Japan's post-pandemic economic recovery, accelerated by the return of international tourism and widespread digital transformation across the industry. The market's expansion is fundamentally driven by structural shifts in consumer behavior, with busy urban lifestyles fueling demand for convenient dining solutions and the resurgence of inbound tourism creating unprecedented opportunities for authentic culinary experiences . The tourism comeback has lifted spending at restaurants positioned near airports, railway hubs, and key cultural sites, while strong urban wage growth is enabling consumers to trade up to premium coffee, specialty desserts, and experiential full-service formats.Operators are investing in mobile apps, QR-code menus, and in-store robots to confront a historic labor shortfall, and these technologies in turn improve table turns and encourage higher ticket sizes. However, the Japan foodservice market is navigating compressed margins due to higher import costs, persistent wage pressure, and continued dependence on overseas commodities.

Japan Foodservice Market Trends and Insights

Busy Modern Life Fuels Demand for Quick Convenience

Japan's accelerating urbanization and evolving work culture are fundamentally reshaping dining patterns, with time-pressed consumers increasingly prioritizing convenience over traditional sit-down experiences. The Ministry of Health, Labour and Welfare reported that average working hours in the service sector increased by 3.2% in 2024, while commuting times in major metropolitan areas extended due to hybrid work patterns creating irregular schedules according to the Ministry of Health, Labour and Welfare. This temporal compression is driving explosive growth in grab-and-go formats, mobile ordering systems, and express service concepts that can deliver quality meals within 10-15 minutes. Quick Service Restaurants are responding by redesigning kitchen workflows and implementing AI-powered demand forecasting to reduce wait times, while convenience stores are expanding their prepared food offerings to capture the growing "nakashoku" (eating at home but not cooking) trend. The demographic shift toward single-person households, which now represent 38% of all Japanese households, further amplifies demand for portion-controlled, individually packaged meal solutions that align with busy lifestyle requirements accorign to the Statistics Bureau of Japan.

Global Tourism Boosts Authentic Dining Experiences

The remarkable recovery of Japan's inbound tourism sector is creating unprecedented demand for authentic culinary experiences, with international visitors reaching 25.07 million in 2024, approaching pre-pandemic levels of 31.9 million in 2019 according to the Japan National Tourism Organization. Tourist spending on food and beverage represents approximately 22% of total expenditure, translating to over USD 11 billion in direct market impact, with particularly strong demand for regional specialties and traditional dining formats that offer cultural immersion. The World Travel & Tourism Council projects continued growth in Japanese tourism through 2030, driven by visa liberalization, increased flight capacity, and Japan's positioning as a premium destination for culinary tourism. Restaurant operators are capitalizing on this trend by developing tourist-specific menu formats with multilingual descriptions, cultural context, and Instagram-worthy presentation that appeals to social media-savvy international visitors. The ripple effect extends beyond tourist hotspots, as domestic consumers increasingly seek out "authentic" experiences inspired by international visitor preferences, creating a halo effect that benefits traditional and regional cuisine segments nationwide.

Severe Labor Shortages Strain Service Capacity

Japan's foodservice sector faces an unprecedented labor crisis, with unemployment rates at historic lows of 2.4% and an aging population creating structural workforce constraints that threaten operational capacity across all segments according to the Statistics Bureau of Japan. The industry's labor shortage rate reached 76.2% in 2024, the highest among all service sectors, forcing operators to reduce operating hours, limit menu complexity, and implement significant wage increases that compress profit margins. Average hourly wages in foodservice increased by 8.7% in 2024, outpacing inflation and creating cost pressures that smaller independent operators struggle to absorb without raising menu prices. The demographic challenge is compounded by cultural factors, as younger workers increasingly avoid foodservice careers due to demanding schedules and limited advancement opportunities, creating a vicious cycle of understaffing and operational stress. Compliance with Japan's revised Labor Standards Act, which limits overtime and mandates rest periods, further constrains operational flexibility while increasing labor costs per hour worked.

Other drivers and restraints analyzed in the detailed report include:

- Consumers Demand Healthier, Sustainable, Local Menus

- Digital Apps and In-Store Robots Drive Efficiency

- Reliance on Imports Creates Supply Chain Fragility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Quick Service Restaurants command a dominant 46.41% market share in 2025, reflecting Japanese consumers' increasing preference for speed, convenience, and value-oriented dining experiences. Cloud Kitchens emerge as the fastest-growing segment with a 11.91% CAGR through 2031, driven by delivery demand and operators' need to reduce real estate costs while expanding geographic reach. Full Service Restaurants maintain steady performance despite labor constraints, with Asian cuisine concepts particularly benefiting from tourism recovery and domestic interest in regional specialties. The QSR segment's growth is accelerated by successful digital transformation initiatives, including mobile ordering platforms that now process 43% of transactions and AI-powered kitchen automation that reduces labor requirements by up to 30%.

Cafe and Bars segment benefits from Japan's evolving coffee culture and after-work socializing patterns, with specialty coffee shops experiencing particular strength as consumers seek premium experiences and Instagram-worthy environments. The segment's performance is supported by the growing acceptance of higher price points for artisanal products and the expansion of third-wave coffee concepts that emphasize origin transparency and brewing expertise. Cloud Kitchen operators are leveraging technology to optimize delivery routes and reduce food preparation times, enabling them to capture market share from traditional dine-in establishments while maintaining higher profit margins through reduced overhead costs.

Independent outlets maintain a commanding 74.61% market share in 2025, demonstrating the enduring appeal of personalized service, local specialties, and community connections that characterize Japan's traditional dining culture. However, chained outlets are expanding rapidly at 11.08% CAGR through 2031, leveraging operational efficiencies, standardized processes, and technology investments to combat labor shortages and supply chain challenges more effectively than smaller operators. The competitive dynamics reflect a fundamental tension between authenticity and efficiency, with independent operators offering unique culinary experiences while chains provide consistency and convenience that appeals to time-pressed consumers.

Chained outlets benefit from economies of scale in procurement, technology deployment, and staff training, enabling them to maintain service levels despite labor constraints while offering competitive pricing. The recent wave of M&A activity, including Skylark's acquisition of Suisan Udon for JPY 24 billion (USD 160 million) in September 2024, demonstrates chains' strategic focus on expanding market presence through acquisition rather than organic growth. Independent operators are responding by forming purchasing cooperatives, adopting shared technology platforms, and developing niche positioning strategies that emphasize artisanal quality and local sourcing to differentiate from standardized chain offerings.

The Japan Foodservice Market is Segmented by Foodservice Type (Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants), Outlet (Chained Outlets, Independent Outlets), Location (Leisure, Lodging, Retail, Standalone, Travel), and Service Type (Dine-In, Takeaway, Delivery). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CKE Restaurants Holdings, Inc.

- Zensho Holdings Co. Ltd.

- Skylark Holdings Co. Ltd.

- Food & Life Companies Ltd.

- Colowide Co. Ltd.

- Toridoll Holdings Corp.

- Starbucks Corporation

- MOS Food Services Inc.

- Komeda Holdings Co. Ltd.

- Kura Sushi Inc.

- Plenus Co. Ltd.

- Domino's Pizza Enterprises Ltd.

- Yoshinoya Holdings Co. Ltd.

- Yum! Brands Inc.

- Saizeriya Co. Ltd.

- Hotland Co. Ltd.

- Ringer Hut Co. Ltd.

- McDonald's Corporation

- Papa John's International, Inc.

- Wendy's International, LLC,

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Number of Outlets

- 4.2 Average Order Value

- 4.3 Regulatory Framework

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Busy modern life fuels demand for quick convenience

- 5.2.2 Global tourism boosts authentic dining experiences

- 5.2.3 Consumers demand healthier, sustainable, local menus

- 5.2.4 Digital apps and in-store robots drive efficiency

- 5.2.5 Growing interest in diverse international cuisines

- 5.2.6 High-quality pre-prepared meals gain acceptance

- 5.3 Market Restraints

- 5.3.1 Increased competition from independent vendors and street-food sellers

- 5.3.2 Inconsistencies in food safety measures and adherence to hygiene standards

- 5.3.3 Severe labor shortages strain service capacity

- 5.3.4 Reliance on imports creates supply chain fragility.

- 5.4 Porter's Five Forces

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitutes

- 5.4.5 Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Foodservice Type

- 6.1.1 Cafe and Bars

- 6.1.1.1 By Cuisine

- 6.1.1.1.1 Bars & Pubs

- 6.1.1.1.2 Cafe

- 6.1.1.1.3 Juice/Smoothie/Desserts Bars

- 6.1.1.1.4 Specialist Coffee & Tea Shops

- 6.1.1.1 By Cuisine

- 6.1.2 Cloud Kitchen

- 6.1.3 Full Service Restaurants

- 6.1.3.1 By Cuisine

- 6.1.3.1.1 Asian

- 6.1.3.1.2 European

- 6.1.3.1.3 Latin American

- 6.1.3.1.4 Middle Eastern

- 6.1.3.1.5 North American

- 6.1.3.1.6 Other FSR Cuisines

- 6.1.3.1 By Cuisine

- 6.1.4 Quick Service Restaurants

- 6.1.4.1 By Cuisine

- 6.1.4.1.1 Bakeries

- 6.1.4.1.2 Burger

- 6.1.4.1.3 Ice Cream

- 6.1.4.1.4 Meat-based Cuisines

- 6.1.4.1.5 Pizza

- 6.1.4.1.6 Other QSR Cuisines

- 6.1.4.1 By Cuisine

- 6.1.1 Cafe and Bars

- 6.2 By Outlet

- 6.2.1 Chained Outlets

- 6.2.2 Independent Outlets

- 6.3 By Locations

- 6.3.1 Leisure

- 6.3.2 Lodging

- 6.3.3 Retail

- 6.3.4 Sandalone

- 6.3.5 Travel

- 6.4 By Service Type

- 6.4.1 Dine-in

- 6.4.2 Takeaway

- 6.4.3 Delivery

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 CKE Restaurants Holdings, Inc.

- 7.4.2 Zensho Holdings Co. Ltd.

- 7.4.3 Skylark Holdings Co. Ltd.

- 7.4.4 Food & Life Companies Ltd.

- 7.4.5 Colowide Co. Ltd.

- 7.4.6 Toridoll Holdings Corp.

- 7.4.7 Starbucks Corporation

- 7.4.8 MOS Food Services Inc.

- 7.4.9 Komeda Holdings Co. Ltd.

- 7.4.10 Kura Sushi Inc.

- 7.4.11 Plenus Co. Ltd.

- 7.4.12 Domino's Pizza Enterprises Ltd.

- 7.4.13 Yoshinoya Holdings Co. Ltd.

- 7.4.14 Yum! Brands Inc.

- 7.4.15 Saizeriya Co. Ltd.

- 7.4.16 Hotland Co. Ltd.

- 7.4.17 Ringer Hut Co. Ltd.

- 7.4.18 McDonald's Corporation

- 7.4.19 Papa John's International, Inc.

- 7.4.20 Wendy's International, LLC,

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK