PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035101

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035101

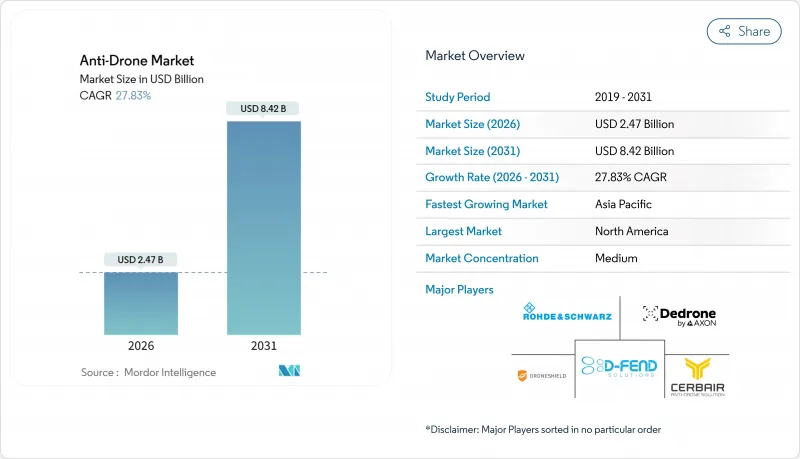

Anti-Drone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The anti-drone market size was valued at USD 2.47 billion in 2026, and is projected to reach USD 8.42 billion by 2031, advancing at a 27.83% CAGR, as commercial operators, critical infrastructure managers, and homeland security agencies move to counter the accelerating proliferation of small unmanned aerial systems.

Demand momentum stems from converging regulatory mandates, a sharp increase in airspace incursions, and the maturation of AI-powered sensor fusion, which lowers false-alarm rates while improving range discrimination. Vendors that package detection and mitigation capabilities into software-defined, service-based offerings now address long-standing capital-budget hurdles and shorten procurement cycles for stadiums, prisons, and temporary venues. Simultaneously, rising geopolitical risk, particularly in Eastern Europe and the Middle East, prompts increased public-sector spending, which accelerates the diffusion of technology into civilian facilities. Overall, the anti-drone market benefits from a multi-layered growth engine, comprising regulation, threat escalation, and technology convergence, which creates structural resilience even when discretionary security budgets are tightened.

Global Anti-Drone Market Trends and Insights

Proliferation Of Low-Cost Commercial Drones Threatening Civilian Assets

Consumer drones priced under USD 500 now deliver 4K video and 30-minute endurance, enabling hostile actors to gather intelligence or deliver payloads with minimal skill. Monthly FAA incident logs exceeded 100 airport drone sightings in 2024, a year-on-year rise of 40%, while Copenhagen Airport halted operations for 90 minutes in September 2025 after an unidentified quadcopter breached its perimeter. UK prisons recorded 347 contraband-carrying drone incursions in 2024, prompting the Ministry of Justice to issue an order for fixed counter-UAS installations at all Category A facilities by mid-2026. The asymmetry is stark: a USD 400 drone can idle a multi-million-dollar facility, forcing operators to adopt layered detection and mitigation frameworks. Insurance underwriters began excluding drone-related losses from standard property cover in 2025, effectively obligating risk-exposed sites to invest in counter-UAS technologies to retain coverage.

Stricter FAA And EU U-Space Mandates For Drone Detection

The FAA's Remote ID rule, which has been in effect since March 2024, requires drones weighing more than 250 grams to broadcast identifying data, establishing an implicit obligation for airports and critical infrastructure owners to monitor compliance in real-time. In the EU, Regulation 2021/664 requires member states to develop U-space corridors that integrate cooperative and non-cooperative traffic detection by 2026. These policies shift liability: operators that fail to detect incursions face risks to their license renewal and rising insurance premiums. National aviation authorities now routinely link operating permits to demonstrated anti-drone capability, compressing procurement timelines and rewarding vendors that ship software-defined, update-ready platforms.

Ambiguous Legality of RF Jamming and Kinetic Takedown

US law prohibits non-federal entities from emitting RF jammers; however, experimental licenses granted by the Federal Communications Commission, under the supervision of the Department of Homeland Security (DHS), permit limited use. This process can take a year to complete. The EU's Radio Equipment Directive also restricts intentional interference, pushing commercial sites toward cyber takeover or kinetic options that raise concerns about safety and tort liability. Net-capture drones or interceptor rounds risk third-party damage, yet few jurisdictions provide safe-harbor immunity. This patchwork hinders the commercial adoption of neutralization technologies and diverts capital toward detection-only deployments that cannot resolve immediate threats.

Other drivers and restraints analyzed in the detailed report include:

- Drone Incursions at Critical Infrastructure (Energy, Airports)

- AI-Powered Multi-Sensor Fusion Improves Detection Accuracy

- High False-Alarm Rates In 5G-Dense Urban Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Neutralization systems are projected to expand at a 27.65% CAGR from 2026 to 2031, gradually eroding the detection-only dominance that delivered 53.95% of 2025 revenue. The shift accelerates as aviation and telecommunication regulators begin granting conditional approvals for cyber-takeover and low-collateral kinetic interceptors. Anduril's Roadrunner reusable interceptor demonstrated 95% kill probability in US Army trials and slashed per-engagement costs below USD 10,000 compared with expendable net-capture solutions. D-Fend Solutions' EnforceAir2 guides rogue drones to safe-landing zones via GPS spoofing, avoiding RF-jamming prohibitions in European jurisdictions. Detection remains critical, yet insurers started offering 10% to 15% premium reductions in 2025 for sites that demonstrate autonomous mitigation, tilting capital-allocation decisions toward neutralization capability.

Detection vendors answer by embedding analytics and machine-learning (ML) classifiers rather than proliferating hardware. Dedrone's RF-EO fusion sensors integrate into Verizon private LTE cores, enabling subscription pricing that offsets upfront capital expenditure. Directed-energy systems, such as Epirus's 20 kW microwave effector, attract defense customers but remain niche in civil markets due to their 30 kVA power requirements and USD 2 million unit costs. Between 2026 and 2031, the anti-drone market is expected to split by jurisdiction: detection-only in regulation-heavy regions and integrated detection-defeat packages in territories where liability regimes evolve faster than legislative reform.

In 2025, fixed platforms accounted for 39.85% of the revenue, as airports, nuclear plants, and oil refineries require 24/7 coverage with overlapping sensor fields. Even so, portable systems are forecast to post a 28.59% CAGR, mirroring the rise of event-driven security contracting. DroneShield's DroneSentry-X Mk2, weighing 35 kg and deployable in 15 minutes, protected the 2024 Paris Olympics and the 2025 World Economic Forum.

Rental economics amplify traction for portables: operators pay USD 10,000-20,000 per week versus USD 500,000 upfront for fixed arrays, aligning with the C-UAS-as-a-Service paradigm. Fixed installations still dominate the anti-drone market size for critical facilities because 10-km radar envelopes, as offered by Thales' Falcon Shield, remain indispensable at congested airfields. Modular designs blur the boundary; Saab's Giraffe 1X ships in ISO containers that bolt to rooftops or truck beds, satisfying semi-permanent use cases.

The Anti-Drone Market Report is Segmented by Technology (Detection Systems and Neutralization/Countermeasure Systems), Platform Type (Fixed and Portable), End-Use Vertical (Commercial and Homeland Security and Law Enforcement), Operating Range (Short-Range, Medium-Range, and Long-Range), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 40.55% of the global revenue in 2025, driven by US DHS contracts and FAA enforcement of Remote ID. The region is forecasted to post a 25.8% CAGR through 2031, slightly trailing the global average as early adopters transition from new installations to software upgrades. US nuclear plants must install perimeter detection systems by 2027 under NRC guidance, while GAO-validated airport pilots reinforce multi-sensor architectures that reduce false positives in dense RF environments. Canada moves more slowly, yet Transport Canada's 2025 draft mandates extend counter-UAS coverage to Vancouver, Toronto, and Montreal airports. Mexico remains nascent, but cartel drone incidents triggered pilot deployments at Guadalajara and Tijuana in late 2024.

The Asia-Pacific region is expected to post the fastest growth at a 27.11% CAGR from 2026 to 2031, as India's Digital Sky platform enforces drone registration, China scales up smart-city surveillance, and Japan liberalizes kinetic interceptors. India removed prior-approval bottlenecks for commercial counter-UAS installs in 2024, accelerating project timelines. China's state-owned airport operators have disclosed that more than 50 major hubs now operate RF-EO fusion systems, primarily sourced from domestic vendors, including CETC. Japan awarded Mitsubishi Electric a contract in 2024 for Narita Airport, integrating radar, EO, and net interceptors. South Korea's nationwide 5G rollout complicates RF detection; yet, Incheon Airport's AI retraining reduced false alarms to below 10% in 2025 trials.

Europe represented roughly 28% of 2025 revenue and is expected to grow at a 26.5% CAGR through 2031, primarily due to U-space compliance and high-profile incidents, such as Copenhagen's 2025 shutdown. The UK leads adoption: airports exceeding 5 million passengers must sustain 24/7 coverage, and Category A prisons must install systems by mid-2026. Germany created an RF-jamming carve-out for refineries in 2025, potentially easing broader EU restrictions. France validated C-UAS-as-a-Service during the 2024 Paris Olympics, awarding contracts to Thales and DroneShield that showcase rapid redeployment capabilities. The Middle East and Africa are expected to expand at a 26.8% CAGR as Saudi Arabia's NEOM and the UAE integrate detection layers into smart-city blueprints, backed by 2024 GACA rules mandating systems at all commercial airports. South America remains the smallest but shows momentum after Brazil's 2025 ANAC guidelines triggered a procurement wave led by Sao Paulo's Guarulhos Airport.

- Dedrone Holdings, Inc.

- CERBAIR

- D-Fend Solutions AD Ltd.

- DroneShield Group Pty Ltd.

- Rohde & Schwarz GmbH & Co. KG

- Thales Group

- QinetiQ Group

- Saab AB

- Anduril Industries, Inc.

- SRC Inc.

- DeTect, Inc.

- CACI International Inc.

- Honeywell International Inc.

- Meteksan Defence Industry Inc.

- OpenWorks Engineering Ltd.

- Rheinmetall AG

- Northrop Grumman Corporation

- Leonardo S.p.A.

- Terma Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of low-cost commercial drones threatening civilian assets

- 4.2.2 Stricter FAA and EU U-space mandates for drone detection

- 4.2.3 Drone incursions at critical infrastructure (energy, airports)

- 4.2.4 AI-powered multi-sensor fusion improves detection accuracy

- 4.2.5 C-UAS-as-a-Service cuts CapEx for venue operators

- 4.2.6 Private 5G campus networks enable passive RF detection

- 4.3 Market Restraints

- 4.3.1 Ambiguous legality of RF jamming and kinetic takedown

- 4.3.2 High false-alarm rates in 5G-dense urban zones

- 4.3.3 Privacy concerns over wide-area acoustic/EO surveillance

- 4.3.4 Fragmented liability between drone and site operators

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Detection Systems

- 5.1.2 Neutralization/Countermeasure Systems

- 5.2 By Platform Type

- 5.2.1 Fixed

- 5.2.2 Portable

- 5.3 By End-Use Vertical

- 5.3.1 Commercial

- 5.3.2 Homeland Security and Law Enforcement

- 5.4 By Operating Range

- 5.4.1 Short-Range (Less than 1 km)

- 5.4.2 Medium-Range (1 to 5 km)

- 5.4.3 Long-Range (Greater than 5 km)

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, and Recent Developments)

- 6.3.1 Dedrone Holdings, Inc.

- 6.3.2 CERBAIR

- 6.3.3 D-Fend Solutions AD Ltd.

- 6.3.4 DroneShield Group Pty Ltd.

- 6.3.5 Rohde & Schwarz GmbH & Co. KG

- 6.3.6 Thales Group

- 6.3.7 QinetiQ Group

- 6.3.8 Saab AB

- 6.3.9 Anduril Industries, Inc.

- 6.3.10 SRC Inc.

- 6.3.11 DeTect, Inc.

- 6.3.12 CACI International Inc.

- 6.3.13 Honeywell International Inc.

- 6.3.14 Meteksan Defence Industry Inc.

- 6.3.15 OpenWorks Engineering Ltd.

- 6.3.16 Rheinmetall AG

- 6.3.17 Northrop Grumman Corporation

- 6.3.18 Leonardo S.p.A.

- 6.3.19 Terma Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment