PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035108

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035108

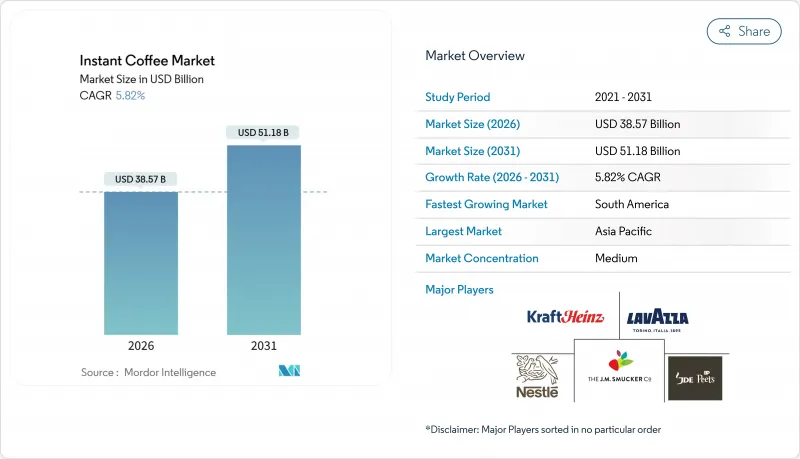

Instant Coffee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The instant coffee market size is estimated at USD 38.57 billion in 2026, and is expected to reach USD 51.18 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031).

This trajectory reflects a sector navigating simultaneous supply-chain stress and demand premiumization, as climate-induced yield volatility in Brazil and Vietnam collides with consumer appetite for single-origin freeze-dried formats. The International Coffee Organization reported that soluble coffee exports fell 28.2% year-over-year in December 2024 to 0.94 million bags, while the composite indicator price surged 75.8% to 310.12 US cents per pound by January 2025, signalling tightening green-coffee availability that compresses instant-coffee margins.

Global Instant Coffee Market Trends and Insights

Rising Demand for Premium Single-Origin Instant Coffee

The premium single-origin segment is fundamentally restructuring the global instant coffee market through substantial shifts in consumer preferences and market dynamics. Market analysis demonstrates a pronounced transition toward traceable, high-quality products with distinctive flavor characteristics, indicating a significant evolution in instant coffee purchasing behavior. This transformation is particularly evident among younger demographic segments, with the National Coffee Association reporting an increase in specialty coffee consumption since 2020, reaching 46% of American adults by January 2025. Consumer willingness to pay premiums for traceable, single-origin instant coffee is redefining value propositions across the category. Craft instant-coffee brands such as Swift Cup Coffee partner with approximately 150 specialty roasters to produce small-batch powders sourced from Colombia, Papua New Guinea, and Ethiopia, retailing at six-packs above USD 15 and per-cup prices exceeding USD 2.50, a multiple of 3 to 4 times conventional instant formats.

Technological Advances in Freeze-Drying

Technological advancements are driving the global instant coffee market's growth, especially as consumers increasingly favor convenience and cafe-style experiences at home. A prime example is Nestle's June 2025 launch of freeze-dried, cold-soluble coffee products, including Nescafe Ice Roast and Nescafe Espresso Concentrate. These products cater to the rising demand for cold coffee formats among Gen Z and millennial consumers. Nestle, utilizing patented freeze-drying and nitrogen-infusion technology, ensures flavor integrity and solubility in cold liquids, an innovation that addresses a major limitation of traditional instant coffee. Supporting this trend, data from the United States Department of Agriculture indicates that in 2024/25, premium green coffee constituted over 60% of China's coffee imports, surpassing traditional soluble coffee consumption. This shift highlights a global coffee culture transformation, with consumers, particularly in emerging markets, leaning towards higher-quality, origin-specific, and freshly brewed experiences. GEA Group introduced enzymatic-hydrolysis extraction, achieving 65 to 80% yield from green beans, paired with aroma-recovery loops that capture and reintroduce volatile esters post-drying. Purdue University researchers patented gas-hydrate foaming techniques that nucleate ice crystals uniformly, minimizing cell-wall rupture and improving reconstitution speed. These innovations lower the capital-intensity gap between spray-drying and freeze-drying, enabling mid-tier brands to offer freeze-dried formats without prohibitive upfront investment.

Climate-Induced Yield Volatility Raising Costs

Climate change disruptions in coffee production economics pose significant operational challenges for the instant coffee market. Extreme weather events have led to notable price volatility across the value chain, influencing both production costs and market balance. The Food and Agriculture Organization reported that adverse weather in key producing nations led to a 38.8% spike in coffee prices in 2024. This surge was particularly pronounced in Arabica prices, which jumped by 58%. Meanwhile, Robusta prices, crucial for instant coffee production, saw an even steeper rise of 70%. These price increases have a cascading effect on the entire value chain, from raw material procurement to final product pricing, making it difficult for manufacturers to absorb costs without impacting profitability. Additionally, supply chain uncertainties, such as delays in transportation, disruptions in sourcing raw materials, and logistical inefficiencies, further exacerbate the challenges. Production capacity limitations, driven by both resource constraints and increased operational costs, add another layer of complexity. Furthermore, manufacturers face difficulties in forecasting demand accurately due to fluctuating prices and inconsistent supply, which can lead to overproduction or underproduction. Together, these factors create considerable hurdles for instant coffee producers striving to maintain consistent output, ensure product availability, and sustain competitive market positioning in the instant coffee market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Penetration of Ready-to-Mix Coffee for On-the-Go Consumption

- Strategic Capacity Expansion by Soluble Coffee Exporters

- Health Concerns Over Added Sugar and Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unflavored instant coffee commands 85.01% of the market share in 2025, establishing itself as the foundation of the instant coffee industry through its versatility and broad consumer acceptance. The segment's dominance is reflected in traditional coffee markets like Brazil, where the United States Department of Agriculture (USDA) forecasts total coffee production for marketing year 2025/26 (July-June) at 65 million bags (60 kilograms per bag) green bean equivalent, representing a 0.5% increase from the 2024/2025. The flavored instant coffee segment is expected to grow at a CAGR of 7.62% from 2026 to 2031, as manufacturers respond to evolving consumer preferences, particularly among younger demographics seeking diverse taste experiences.

The growth in flavored instant coffee reflects changing consumer tastes. Products including vanilla, caramel, hazelnut, mocha, and seasonal variants provide alternatives to conventional coffee offerings. These options particularly resonate with younger consumers who demonstrate increased interest in experimenting with flavor combinations. The range of choices enables instant coffee to reach consumers beyond traditional coffee drinkers. Manufacturers are creating new flavor profiles that blend traditional coffee characteristics with flavored beverages to increase market penetration in the instant coffee market. The segment's growth is supported by advances in flavor encapsulation technologies that better preserve aromas during the drying process, resulting in more authentic flavors that rival fresh-brewed coffee.

Spray-dried instant coffee held a 63.52% share in 2025, reflecting entrenched capital bases and operational familiarity among large-scale producers. Freeze-dried formats grow at 6.33% CAGR through 2031, driven by patents that reduce cycle times and energy consumption while preserving volatile aromatics. Nestle's rapid freeze-drying patents halve processing duration, and GEA's enzymatic-hydrolysis extraction achieves 65 to 80% yield from green beans, paired with aroma-recovery systems that reintroduce volatile esters post-drying. Purdue University's gas-hydrate foaming technique nucleates ice crystals uniformly, minimizing cell-wall rupture and improving reconstitution speed, lowering the quality gap between freeze-dried and spray-dried outputs.

Brazil's soluble-coffee exports from January to March 2025 comprised 71.5% spray-dried and 23% freeze-dried formats, illustrating spray-drying's cost advantage in high-volume channels. However, freeze-dried instant commands 30 to 50% price premiums in retail, justifying the higher capital and energy outlays for brands targeting premium tiers. Food Empire Holdings' USD 80 million freeze-dried plant in Vietnam, scheduled for early-2028 completion, will serve Asian markets where freeze-dried instant penetration remains low, presenting a whitespace opportunity. The International Organization for Standardization's quality benchmarks, extraction yield between 18 and 22%, chlorogenic-acid retention, and acrylamide below 850 micrograms per kilogram, are increasingly met by freeze-dried processes, supporting regulatory compliance.

The Instant Coffee Market is Segmented Into Flavoring (Flavored and Unflavored), Production Technology (Spray-Dried Instant Coffee and Freeze-Dried Instant Coffee), Price (Mass and Premium), Packaging Format (Sachets, Pouches, and Jars), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds a 38.36% share of the instant coffee market in 2025, driven by rapid urbanization, rising disposable incomes, and evolving coffee cultures. According to the United States Department of Agriculture (USDA), Chinese consumers used approximately 5.8 million 60-kilogram bags of coffee between 2023 and 2024. The Chinese market has shifted toward higher-quality green coffee, which now represents over 60% of imports. In India, coffee consumption exceeded one million 60-kilogram bags between 2023 and 2024, as reported by the United States Department of Agriculture (USDA).

South America is experiencing the fastest regional growth at 7.22% CAGR (2026-2031), with Brazil transitioning from a traditional producer to a major consumer market. According to Brazil's National Supply Company, coffee production reached 58.81 million 60-kilogram bags in 2024, increasing from 55.07 million bags in 2023. The region's expansion stems from rising domestic consumption, capacity expansions, and increased focus on value-added processing.

North America and Europe maintain stable market positions with established coffee cultures. The National Coffee Association indicates that 66% of American adults consume coffee daily, averaging 3 cups per person. Household instant coffee ownership increased from 27% in 2020 to 35% in 2025. The Middle East and Africa, while holding a smaller market share, demonstrate growth potential through developing coffee cultures and increasing urbanization in the instant coffee industry.

- Nestle S.A.

- J.M. Smucker Company

- Kraft Heinz Company

- Tata Consumer Products Limited

- Luigi Lavazza S.p.A.

- JDE Peet's N.V.

- Tchibo GmbH

- Strauss Group Ltd.

- The Coca-Cola Company

- Unilever PLC

- UCC Ueshima Coffee Co., Ltd.

- Trung Nguyen Group JSC

- Massimo Zanetti Beverage Group

- Sleepy Owl Coffee

- PT Kapal Api Global

- Matthew Algie & Company Limited

- Zino Davidoff Group

- TGL Company

- CCL Products (India) Ltd.

- Blueberry Agro Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for premium single-origin instant coffee

- 4.2.2 Technological advances in freeze-drying

- 4.2.3 Increasing demand of ready-to-mix coffee for on-the-go consumption

- 4.2.4 Strategic capacity expansion by soluble coffee exporters

- 4.2.5 Expansion of retail channels and e-commerce platforms improves product accessibility

- 4.2.6 Growing cafe culture influences at-home coffee consumption habits

- 4.3 Market Restraints

- 4.3.1 Health concerns over added sugar and additive

- 4.3.2 Competition from ready-to-drink coffee and cold brews

- 4.3.3 High caffeine content may deter sensitive consumers

- 4.3.4 Climate-induced yield volatility raises costs

- 4.4 Consumer Behaviour Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Flavored

- 5.1.2 Unflavored

- 5.2 Production Technology

- 5.2.1 Spray-Dried Instant Coffee

- 5.2.2 Freeze-Dried Instant Coffee

- 5.3 Price

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 Packaging Format

- 5.4.1 Sachets

- 5.4.2 Pouches

- 5.4.3 Jars

- 5.5 Distribution Channel

- 5.5.1 Supermarkets/Hypermarkets

- 5.5.2 Convenience/Grocery Stores

- 5.5.3 Specialty Stores

- 5.5.4 Online Retail

- 5.5.5 Other Distribution Channels

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Poland

- 5.6.2.8 Belgium

- 5.6.2.9 Sweden

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Indonesia

- 5.6.3.6 South Korea

- 5.6.3.7 Thailand

- 5.6.3.8 Singapore

- 5.6.3.9 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Peru

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Egypt

- 5.6.5.6 Morocco

- 5.6.5.7 Turkey

- 5.6.5.8 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 J.M. Smucker Company

- 6.4.3 Kraft Heinz Company

- 6.4.4 Tata Consumer Products Limited

- 6.4.5 Luigi Lavazza S.p.A.

- 6.4.6 JDE Peet's N.V.

- 6.4.7 Tchibo GmbH

- 6.4.8 Strauss Group Ltd.

- 6.4.9 The Coca-Cola Company

- 6.4.10 Unilever PLC

- 6.4.11 UCC Ueshima Coffee Co., Ltd.

- 6.4.12 Trung Nguyen Group JSC

- 6.4.13 Massimo Zanetti Beverage Group

- 6.4.14 Sleepy Owl Coffee

- 6.4.15 PT Kapal Api Global

- 6.4.16 Matthew Algie & Company Limited

- 6.4.17 Zino Davidoff Group

- 6.4.18 TGL Company

- 6.4.19 CCL Products (India) Ltd.

- 6.4.20 Blueberry Agro Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK