PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035117

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035117

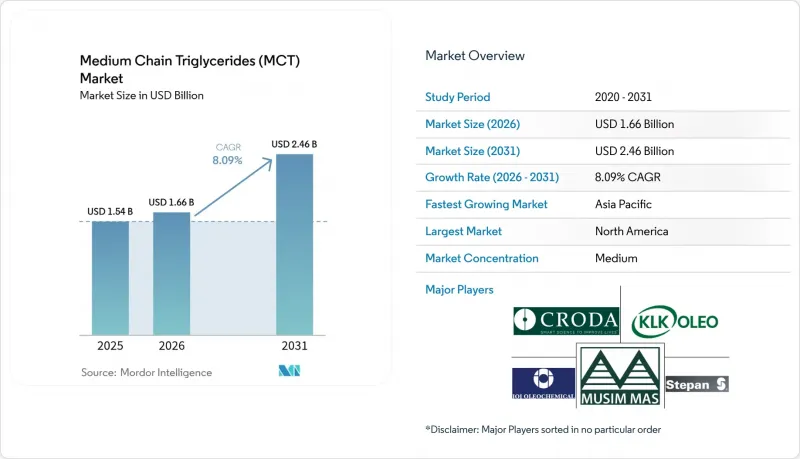

Medium Chain Triglycerides (MCT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Medium Chain Triglycerides market size is expected to grow from USD 1.54 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 8.09% CAGR over 2026-2031.

Growth is led by widening usage in sports nutrition, ketogenic diets, premium infant formulas, and lipid-based drug delivery systems. Liquid formats, particularly those sourced from coconut oil, underpin mainstream adoption because they blend easily into foods and beverages while delivering rapid, stomach-friendly energy. Pharmaceutical formulators value MCTs' portal-vein absorption pathway, which enhances bioavailability for poorly soluble actives, and cosmetic brands prize their light texture and clean-label positioning. Supply-side strategies now center on source diversification-especially into certified palm kernel oil and emerging oil crops-to hedge climate-related price swings, while technology investments focus on purity upgrades and tailored fatty-acid blends. Competitive intensity remains moderate as vertically integrated players scale production, yet niche innovators secure premium contracts in clinical nutrition and specialty cosmetics.

Global Medium Chain Triglycerides (MCT) Market Trends and Insights

Growing Usage in Sports & Performance Nutrition

Athletes increasingly replace long-chain fats and simple carbohydrates with MCT-fortified gels, shots, and powders because caprylic-dominant oils generate ketones within minutes, sustaining endurance without glycemic spikes. Clinical work in older adults shows that daily MCT supplementation enhances muscle quality while lowering glucose oxidation, hinting at crossover benefits for recovery and healthy aging. Research highlights that a significant portion of sports-nutrition buyers are willing to pay a premium for recognizable, single-origin lipids that align with clean-label diets. Brand owners now list specific chain-length ratios on front-of-pack claims to differentiate performance profiles, pushing processors toward tighter fractionation and purity specifications. North American contract-manufacturers report double-digit order growth for keto-friendly ready-to-drink beverages that rely on liquid MCTs for smooth mouthfeel and shelf stability. Sustainable palm kernel supply chains that carry RSPO certification are being tapped to manage cost while meeting Environmental, Social, and Governance (ESG) targets in athlete-focused product lines.

Rising Adoption of Ketogenic & Low-Carb Diets

Widespread interest in ketogenic eating is re-shaping grocery aisles as shoppers seek ingredients that elevate circulating ketone bodies quickly. Caprylic-dominant tricaprylin delivers the most efficient ketogenic response compared with traditional coconut oil, driving its dominance in concentrated drops and shots. Medical professionals now prescribe MCT-enriched meal plans to epilepsy patients because medium-chain triglyceride formulations allow higher carbohydrate intake than classical ketogenic protocols without compromising seizure control. Social-media recipe influencers amplify this clinical endorsement, accelerating household penetration in the United States, Canada, and Western Europe. Asian urban consumers are joining the trend as e-commerce platforms bundle MCT oil with glucomannan fibers in low-carb starter packs, prompting regional refiners to add smaller SKUs and flavored variants. The dietary shift sustains robust baseline demand and mitigates seasonality, anchoring revenue streams for vertically integrated producers.

Volatile Coconut & Palm Kernel Oil Prices

Weather-driven supply shocks frequently lift feedstock prices. Statistical modelling shows that a 1% uptick in palm kernel oil prices can push coconut-oil demand higher by 1.89% as buyers substitute between the two inputs, amplifying volatility. Erratic rainfall in Indonesia and Malaysia, the twin pillars of palm supply, depresses fresh-fruit bunch yields and spills into refined-oleochemical pricing. Such spikes compress gross margins for MCT refiners that operate on three-month fixed-price contracts with food manufacturers. Vertical integration into plantations offers a natural hedge, but smaller processors without acreage must rely on financial derivatives or long-term supply agreements, which can raise working-capital requirements.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in Personal Care & Cosmetics Applications

- MCTs in Lipid-Based Drug Delivery Systems

- Availability of Alternative Functional Lipids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid products accounted for 77.10% sales in 2025, a commanding lead that will widen as sports-drink, RTD coffee, and medical-nutrition brands prefer pourable formats for quick dispersion. The liquid sub-category is projected to grow at 8.74% CAGR, outpacing powders. One-shot ampoules targeting endurance athletes illustrate the trend: formulators achieve isotonic profiles without emulsifiers, preserving label simplicity. In contrast, powders cater to bars, bakery mixes, and sachets, where low moisture and long shelf life matter. Advancements in spray-drying and encapsulation have significantly improved oil-load capacity, reducing the cost per gram of active lipid. However, challenges like bulk density and mouth-feel limitations continue to confine these powders to specialized applications. Innovations such as agglomerated granules with lecithin carriers could expand penetration into instant beverages.

Coconut oil retained a 75.60% share in 2025 thanks to positive consumer perception and long-standing supply chains across the Philippines, Indonesia, and India. That dominance masks rapid palm kernel oil gains: the latter is forecast at 8.56% CAGR. Malaysian refiners are investing in mid-stream fractionation to supply pharmaceutical-grade C8/C10 cuts, eroding brand-owner prejudice. Alternative feedstocks like macauba and synthetic esters are gaining attention due to their climate-resilient yields, despite their limited adoption. Multinationals trial blended-source strategies to hedge climate risks and harmonize fatty-acid spectra, a sign that supply diversification will become standard by the decade's end.

The Medium Chain Triglycerides Report is Segmented by Form (Dry, Liquid), Source (Coconut Oil, Palm Kernel Oil, Others), Fatty Acid Type (Caprylic (C8), Capric (C10), Lauric (C12), Caproic (C6)), Application (Food and Beverage, Personal Care and Cosmetics, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.90% revenue in 2025. The region benefits from well-defined FDA GRAS rulings, enabling swift cross-category adoption. Canadian functional-food regulations similarly streamline MCT-supplement launches, cementing regional leadership.

Asia-Pacific is the fastest-growing territory at 8.76% CAGR. China's dual-circulation policy encourages domestic production of high-value oleochemicals, catalyzing investments such as KLK's expanded refinery in Jiangsu. Rising birth rates in India and Indonesia underpin robust infant-formula demand, while Japan's aging population fuels clinical-nutrition consumption. Import duties on refined coconut oil were cut in Vietnam and Thailand during 2024, facilitating intra-ASEAN trade and lowering landed costs for local blenders.

Europe maintains a technology-driven market. Germany, France, and the United Kingdom source high-purity MCTs for drug-delivery platforms and cosmeceuticals. The EU's 2024 novel-food approvals cement regulatory certainty, yet the imminent Deforestation Regulation raises compliance hurdles for non-segregated palm-kernel material; as a result, suppliers are accelerating satellite-based traceability systems. Eastern European processors increasingly import raw coconut oil via the Black Sea corridor, then fractionate internally to sidestep RSPO premium charges, a tactic that trims cost yet demands stringent in-house sustainability audits.

South America shows steady growth as Brazil's sports-nutrition category broadens and domestic macauba plantations promise future feedstock resilience. Middle East & Africa remain nascent but are opening via medical-nutrition tenders and halal-certified personal-care launches in the Gulf Cooperation Council states. Trade incentives in the African Continental Free Trade Area may foster local fractionation hubs over the next decade, though infrastructure and feedstock availability remain early-stage.

- AAK AB

- ABITEC

- Acme-Hardesty

- Barlean's Organic Oils, LLC

- BASF SE

- ConnOils

- CREMER OLEO GmbH & Co. KG

- Croda International Plc

- Henry Lamotte Oils GmbH

- IOI Oleo GmbH

- Jarrow Formulas Inc.

- Kerry Group plc

- KLK Oleo

- Musim Mas Group

- Oleon NV

- Stepan Company

- Sternchemie GmbH & Co. KG

- The Nisshin OilliO Group Ltd.

- Vitaflo International Ltd.

- Wilmar International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of MCTs in sports and performance nutrition

- 4.2.2 Rising adoption of ketogenic and low-carb diets

- 4.2.3 Expansion in personal care and cosmetics applications

- 4.2.4 MCTs in lipid-based drug delivery systems

- 4.2.5 Premium infant formula demand in Asia

- 4.3 Market Restraints

- 4.3.1 Volatile coconut and palm kernel oil prices

- 4.3.2 Availability of alternative functional lipids

- 4.3.3 Sustainability certification costs for palm sourcing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Dry

- 5.1.2 Liquid

- 5.2 By Source

- 5.2.1 Coconut Oil

- 5.2.2 Palm Kernel Oil

- 5.2.3 Others

- 5.3 By Fatty Acid Type

- 5.3.1 Caprylic (C8)

- 5.3.2 Capric (C10)

- 5.3.3 Lauric (C12)

- 5.3.4 Caproic (C6)

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Turkey

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AAK AB

- 6.4.2 ABITEC

- 6.4.3 Acme-Hardesty

- 6.4.4 Barlean's Organic Oils, LLC

- 6.4.5 BASF SE

- 6.4.6 ConnOils

- 6.4.7 CREMER OLEO GmbH & Co. KG

- 6.4.8 Croda International Plc

- 6.4.9 Henry Lamotte Oils GmbH

- 6.4.10 IOI Oleo GmbH

- 6.4.11 Jarrow Formulas Inc.

- 6.4.12 Kerry Group plc

- 6.4.13 KLK Oleo

- 6.4.14 Musim Mas Group

- 6.4.15 Oleon NV

- 6.4.16 Stepan Company

- 6.4.17 Sternchemie GmbH & Co. KG

- 6.4.18 The Nisshin OilliO Group Ltd.

- 6.4.19 Vitaflo International Ltd.

- 6.4.20 Wilmar International Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment