PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035118

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035118

Insurance Third Party Administrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

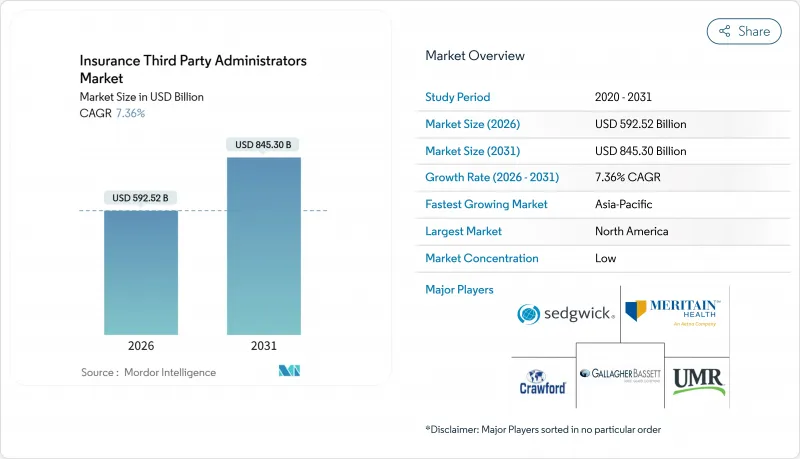

The Insurance Third-Party Administrators market is valued at USD 592.52 billion in 2026 and is forecast to reach USD 845.30 billion by 2031, reflecting a 7.36% CAGR.

This reflects a robust long-term growth trajectory and underscores the increasing scale and significance of the TPA sector. A major factor driving this growth is the rising adoption of self-funded health plans, which require specialized administrative services for efficient claims management and regulatory compliance. Insurers are also increasingly shifting toward digital-first administration models, leveraging technology to streamline workflows, reduce operational costs, and enhance customer service. The use of advanced analytics is further transforming the market, enabling carriers to optimize risk allocation, monitor claims more effectively, and improve financial performance. These changes have accelerated the trend toward outsourcing administration, as insurers seek operational flexibility, scalability, and resilience. TPAs play a critical role in helping insurers navigate complex regulatory environments, multi-state licensing, and cybersecurity challenges. The need for real-time data management and audit-ready processes has become a central requirement, further emphasizing the importance of third-party expertise. In India, regulatory and policy initiatives are driving additional growth in the TPA market. Guidelines from IRDAI, the implementation of the National Health Claim Exchange, and the ongoing expansion of the Ayushman Bharat program are creating demand for scalable, compliant TPA solutions that can support multilingual engagement and efficient claims processing.

Global Insurance Third Party Administrators Market Trends and Insights

Rising self-funded Health Plans Among Mid-sized Employers

Self-funded health coverage has become a mainstream choice, particularly among mid-sized and large employers. Among firms with 200 or more employees, the majority offer self-funded plans, while smaller and mid-sized firms increasingly adopt level-funded hybrid plans to manage risk and control costs. Average annual premiums for family coverage now exceed USD 26,900, with workers contributing nearly USD 6,850 on average, and single coverage deductibles averaging USD 1,886. These rising costs and the desire to avoid insurer risk loads have driven employers to consider self-funding, which allows greater control over plan design and financial exposure. High-deductible health plans with savings options and PPOs remain common, but self-funded arrangements are growing faster in larger firms. This expansion directly increases demand for third-party administrators that can provide stop-loss coverage, compliance support, and flexible, modular administrative services tailored to employer needs. As a result, self-funded adoption is reinforcing the TPA scale and sustaining the momentum of configurable benefits solutions across mid-sized employer segments.

Digitalization and Hyper-Automation in Claims

Digital-first claims processing is significantly reducing cycle times as insurers migrate to cloud platforms and deploy agentic AI for intake triage, fraud detection, and reserve optimization. These unified operating models minimize handoffs and rework, improving efficiency across the claims lifecycle. Generative coding tools now achieve high accuracy, reduce labor costs per claim, and lower denial rates, aligning automation with improved member experience. Leading platforms illustrate this transformation: Crawford's co-pilot guides adjusters with next-best actions, Gallagher Bassett's Luminos generates machine-driven claim summaries, and CorVel's agentic workflows reduce manual steps in eligibility verification and medical necessity reviews. Sedgwick has extended automation into legal bill review and vendor management by integrating legal spend management software, enabling real-time overbilling detection for complex casualty programs. The TPA market benefits when proprietary AI leverages claims data, offering buyers comparable insights into automation depth and delivering measurable cost and service advantages, particularly across Indian enterprise portfolios that prioritize efficiency and transparency.

Rising Cyber-Risk and Data-Privacy Liabilities

Rising cyber threats and evolving data privacy regulations are creating significant challenges for TPAs and healthcare administrators. The IBM Cost of a Data Breach Report further highlights that the global average cost of a data breach is around 4.44 million USD, and organizations lacking AI governance and proper access controls face heightened risk exposure. Breaches in complex environments increase remediation costs, while companies leveraging AI and automation in security save roughly 1.9 million USD per incident. TPAs, which aggregate eligibility, claims, and payment data across thousands of clients, are particularly attractive targets, creating cascading liabilities under HIPAA, state data protection laws, and GDPR when compromised. Buyers now mandate SOC 2 Type II compliance, annual penetration tests, and cyber-insurance as baseline conditions, though zero-day exploits and credential theft demonstrate that compliance alone is not sufficient. GCC markets are experiencing rising exposure as health information exchanges in Saudi Arabia and the UAE connect payers, providers, and patients, expanding the attack surface even as digital mandates accelerate adoption.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Cost Transparency & Value-Based Administration

- AI-driven Fraud Analytics Improving Loss Ratios

- Complexity of multi-state licensing and compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Life and Health Insurance contributed 51.27% of total revenue in 2025, reflecting the complexity and regulatory requirements that lead employers and public programs to outsource administration under structured service-level agreements and audit-ready processes. The Insurance Third-Party Administrators market is seeing strong growth in travel insurance, where TPAs are positioned to expand rapidly as embedded distribution with airlines and online agencies converts a significant portion of bookings into coverage. In the United States, the travel insurance segment is projected to nearly double over the coming years, with annual multi-trip policies for frequent travelers and remote workers driving much of the growth. Strategic acquisitions, such as PassportCard's purchase of Pattern, demonstrate the focus on controlling embedded distribution while TPAs manage mobile claims, ID cards, and regulatory compliance behind the scenes. The market benefits when TPAs deliver point-of-sale coverage that scales across travel portals in India, maintaining fast claims turnaround and high customer satisfaction.

Travel administration is only one pillar of TPA activity, as retirement and pensions provide stable volumes despite fee compression, sustaining revenues for incumbents even in a competitive pricing environment. Commercial general liability and motor lines follow broader P&C trends, with carriers increasingly insourcing high-frequency, low-severity claims as cloud-based tools streamline adjudication workflows. Workers' compensation remains a specialized niche requiring combined clinical management, subrogation, and litigation expertise that employers cannot replicate internally without substantial investment. Overall, the market is bifurcating by complexity, with commoditized health claims under AI and insourcing pressure while niche verticals preserve margins through specialized workflows and expert teams. India's market reflects a similar split, as employers rely on TPAs for complex lines and embedded travel insurance while adjusting sourcing models for routine health claims in areas where carriers have strong digital capabilities.

Claims administration accounted for 40.76% of service revenue in 2025, highlighting the continued centrality of claims handling and payment functions in third-party administration. Provider-network management is expected to grow rapidly as TPAs leverage claims history, quality metrics, and access modeling to build high-performing networks that reduce operating costs without compromising member satisfaction. The market benefits when data-driven network curation and personalized provider guidance improve outcomes, cost-efficiency, and convenience for members. Cost-transparency tools aligned with CMS machine-readable files further enhance employee decision-making, linking network design directly to member experience. In India, procurement increasingly emphasizes network depth, quality measures, and reporting granularity, pulling TPAs toward value-based administration with clear performance targets and corrective triggers.

Policy administration, billing, and enrollment continue to grow steadily as cloud platforms streamline onboarding, qualifying events, COBRA, and invoicing for standard plan designs. Risk and compliance services, including subrogation and Medicare Section 111 reporting, remain critical as penalties for lapses underscore their importance in complex programs. The TPA market is shifting as claims processing becomes a low-cost utility under AI, while network design, payment integrity, and compliance orchestration command premium pricing. Indian buyers now weigh the sophistication of network analytics and fraud controls alongside unit pricing when evaluating TPAs. Service providers that demonstrate measurable savings, robust audits, and performance-linked outcomes gain a competitive advantage in renewals and RFP processes.

The Insurance Third-Party Administrators Market Report is Segmented by Insurance Type (Healthcare, Retirement, and More), Service Type (Claims Management, Policy Administration, and More), End User (Insurance Companies, Self-Insured Employers, and More), Enterprise Size (Large, SME), Technology (Cloud, AI, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 29.39% of the 2025 Insurance Third-Party Administrators market, supported by a strong self-funded foundation where a large share of United States workers participate in self-insured plans and substantial funds flow through TPAs under ASO and direct administration structures. Procurement expectations have shifted toward strategic partnerships, as seen in Delaware's RFPs emphasizing advanced payment models and chronic-condition programs that go beyond basic claims processing. Market growth is slowing compared with post-ACA periods, as large-firm self-funding reaches saturation, and incremental expansion depends on mid-market and SME adoption driven by clear ROI from TPA capabilities. Technology adoption is mature, with cloud platforms and generative AI becoming mainstream and operational improvements such as lower denial rates demonstrating measurable value to clients. Regulatory complexity, including transparency file requirements, No Surprises Act arbitration, PBM state laws, and TCPA litigation exposure, favors TPAs with robust legal, compliance, and IT infrastructure.

Asia-Pacific is projected to grow at an 11.36% CAGR from 2026 to 2031, fueled by China's broad basic medical insurance coverage and India's strong annual expansion in life insurance, which expands administrative demand. Digital-first initiatives like India's National Health Claim Exchange and IRDAI guidelines under Ayushman Bharat support standardized data exchange and scalable TPA partnerships. Mobile-first populations and multilingual needs drive investment in platforms that balance localized service with central governance. Competitive dynamics include local specialists navigating provincial rules alongside multinational entrants serving cross-border employers and expatriates, creating diverse sourcing options. Sustained growth depends on strong execution in data governance, cybersecurity, and value-based frameworks that enable payer-provider collaboration as regional regulations evolve.

Europe, the Middle East, and Africa show steady gains, with the GCC standing out due to expatriate coverage mandates, where the UAE and Saudi Arabia contribute the largest share of health insurance premiums. HIE platforms in the Middle East accelerate the adoption of AI for claims and fraud management, speeding up the path to digital maturity for TPAs. European markets continue steady TPA growth, supported by outsourcing and digitization trends, while profitability improvements among carriers encourage strategic investments in complex claims management and cross-border coverage. Latin America grew 7.5% year-over-year in 2025 across the insurance sector, but regulatory fragmentation and currency volatility limit TPA penetration to below 5% of regional premiums. For India-focused multinationals, these regional patterns shape strategies for risk pooling, shared services, and vendor selection to balance global standards with local execution in the TPA market.

- Sedgwick Claims Management Services

- Gallagher Bassett Services

- Crawford & Company

- CorVel Corporation

- Charles Taylor TPA

- UMR Inc.

- ESIS Inc.

- Helmsman Management Services

- Meritain Health

- Healthscope Benefits

- Planned Administrators Inc. (PAI)

- Davies Group

- EXL Service/Xceedance

- Amalgamated Employee Benefits Administrators

- BASIC TPA

- HR Works

- AbsencePlus

- UC Alternative

- Caremark TPA

- Trizetto Provider Solutions

- Key Benefit Administrators

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing self-funded health plans among mid-sized employers

- 4.2.2 Acceleration of digitalization & hyper-automation in claims

- 4.2.3 Regulatory push for cost-transparency and value-based administration

- 4.2.4 AI-driven fraud analytics improving loss ratios

- 4.2.5 Private-equity roll-ups unlocking national scale economics

- 4.2.6 Embedded-insurance models needing post-bind TPA support

- 4.3 Market Restraints

- 4.3.1 Escalating cyber-risk & data-privacy liabilities

- 4.3.2 Multi-state licensing & compliance complexity

- 4.3.3 Insurers' in-house administration squeezing fee margins

- 4.3.4 Acute shortage of AI / claims-tech talent

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Digital Adoption & Significance in TPAs

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Insurance Type

- 5.1.1 Life and Health Insurance

- 5.1.2 Retirement & Pension

- 5.1.3 Commercial General Liability

- 5.1.4 Motor

- 5.1.5 Workers' Compensation

- 5.1.6 Travel

- 5.1.7 Others

- 5.2 By Service Type

- 5.2.1 Claims Management

- 5.2.2 Policy Administration

- 5.2.3 Billing & Enrollment

- 5.2.4 Provider-Network Management

- 5.2.5 Risk & Compliance Services

- 5.3 By End User

- 5.3.1 Insurance Companies

- 5.3.2 Self-insured Employers

- 5.3.3 Government Health Schemes

- 5.3.4 Brokers & Reinsurers

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small & Medium Enterprises

- 5.5 By Technology

- 5.5.1 Cloud-based Platforms

- 5.5.2 On-premise Solutions

- 5.5.3 AI-enabled TPAs

- 5.5.4 Blockchain-enabled TPAs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Sedgwick Claims Management Services

- 6.4.2 Gallagher Bassett Services

- 6.4.3 Crawford & Company

- 6.4.4 CorVel Corporation

- 6.4.5 Charles Taylor TPA

- 6.4.6 UMR Inc.

- 6.4.7 ESIS Inc.

- 6.4.8 Helmsman Management Services

- 6.4.9 Meritain Health

- 6.4.10 Healthscope Benefits

- 6.4.11 Planned Administrators Inc. (PAI)

- 6.4.12 Davies Group

- 6.4.13 EXL Service/Xceedance

- 6.4.14 Amalgamated Employee Benefits Administrators

- 6.4.15 BASIC TPA

- 6.4.16 HR Works

- 6.4.17 AbsencePlus

- 6.4.18 UC Alternative

- 6.4.19 Caremark TPA

- 6.4.20 Trizetto Provider Solutions

- 6.4.21 Key Benefit Administrators

7 Market Opportunities & Future Outlook

- 7.1 Adoption of Advanced Technologies (AI, Blockchain, Cloud)

- 7.2 Growth in Claims Management Services