PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035119

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035119

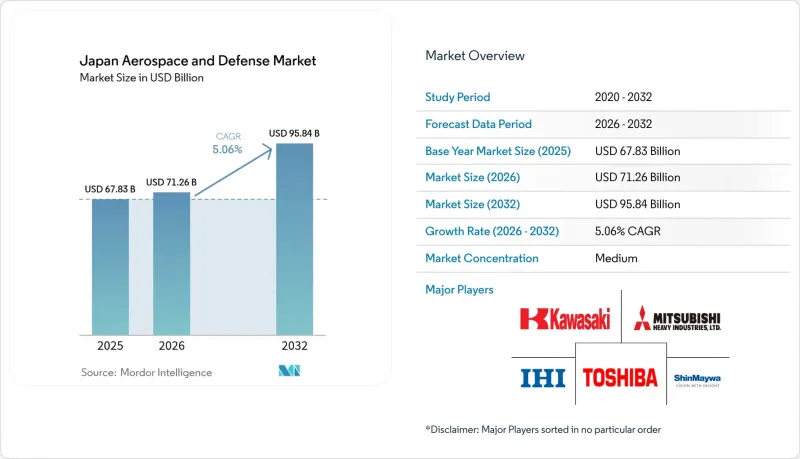

Japan Aerospace And Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032)

Japan aerospace and defense market size in 2026 is estimated at USD 71.26 billion, growing from 2025 value of USD 67.83 billion with 2032 projections showing USD 95.84 billion, growing at 5.06% CAGR over 2026-2032.

Tokyo's multi-year plan to lift defense outlays to 2% of gross domestic product, combined with a rebound in commercial flight activity, underpins the expansion. Rising orders for wide-body aircraft, accelerated delivery schedules for F-35 fighters, and new work on the Global Combat Air Programme (GCAP) broaden the industrial base. Simultaneously, tax measures that take effect in 2026 help secure predictable funding for missile, cyber, and space programs, while joint sustainment frameworks with the US drive incremental maintenance revenue. EW upgrades and sensor procurements pass critical design reviews, creating pull-through demand for domestic semiconductor and composite suppliers. Moderate market concentration persists because Japanese primes rely on US and European design authority for engines and mission systems, even as local content rules channel 60% of spending to in-country vendors.

Japan Aerospace And Defense Market Trends and Insights

Rising Defense Spending Aligned With the 2% of GDP Target

The FY 2025 defense budget reached JPY 8.7 trillion (USD 56 billion), marking a 7.2% year-on-year increase and positioning the plan on a glide path to achieve the 2% of GDP objective by FY 2027. Tax hikes that take effect in 2026 provide a recurring revenue stream, enabling multi-year missile, cyber-defense, and space projects. Funding priorities shift toward stand-off munitions and network-centric systems, prompting new orders for electronic-warfare suites, data-link terminals, and low-latency satellite links. The December 2024 US-Japan Extended Deterrence Guidelines institutionalize joint contingency planning, which raises interoperability standards and accelerates the procurement of common encrypted communication equipment. These dynamics enlarge the Japan aerospace and defense market by opening budget headroom for both acquisition and sustainment.

Expansion of Next-Generation Fighter Aircraft and Combat Aviation Programs

GCAP launched a trilateral government organization in December 2023 to field a sixth-generation fighter by 2035, with Mitsubishi Heavy Industries leading domestic workshare. Revised export rules issued in March 2024 permit the aircraft to be sold to third countries, a move intended to increase production volume and reduce unit cost. Parallel F-35A and F-35B deliveries continue, expanding aerial deterrence while mitigating risks to the GCAP schedule. However, engineering resources are stretched as the same teams juggle F-35 final assembly, F-2 upgrades, and early F-3 prototyping. The workstream fuels subsystem orders for advanced sensors, composite wings, and next-generation turbofans, lifting the Japan aerospace and defense market during the development phase and into serial production.

Stringent Export-Control Policies Limiting Production Scale and Market Expansion

Revised export rules permit the sale of co-developed systems only with unanimous partner approval, introducing a veto risk that curbs production runs and keeps unit costs high. Without foreign orders, the F-3 program would be able to build fewer than 100 airframes, which would undermine economies of scale. Domestic primes continue to lobby for additional liberalization, but public opinion remains cautious about arms exports, constraining the near-term upside for the Japan aerospace and defense market.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Recovery in Commercial Aviation MRO Demand

- Government Incentives for Indigenous Missile and Hypersonic Development

- Advanced Manufacturing Talent Shortages and Supply Chain Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Defense secured 63.32% of 2025 revenue, reflecting sustained Type 12 missile, F-35, and frigate procurement, while aerospace is projected to grow at a 5.52% CAGR through 2032. The Japan aerospace and defense market relies on defense for scale but turns to commercial aviation for momentum. Japan Airlines and ANA Holdings added 154 wide bodies in 2024-2025, pushing engine and landing gear suppliers to full capacity. Meanwhile, the GCAP fighter injects high-tech workshare, and unmanned systems gain budget priority for island defense.

Commercial recovery also draws global maintenance traffic to domestic hangars, reinforcing service revenue. The government's mandate that 60% of defense contract value flow to local suppliers nurtures small electronics and composite firms; however, the cap on export volumes restrains aggregate sector growth. Continued liberalization and timely technology transfers will determine whether aerospace achieves parity with defense in the Japan aerospace and defense market by the early 2030s.

Aerial platforms generated 34.21% of 2025 revenue and are expected to rise at a 5.31% CAGR, positioning them at the center of future expansion. Fixed-wing programs encompass commercial narrowbody aircraft, F-35 fighters, and P-1 patrol aircraft. Rotary-wing production remains modest but steady, while unmanned aerial systems receive record allocations worth JPY 50 billion (USD 320 million) in FY 2025. The Japan aerospace and defense market size for aerial unmanned assets is projected to widen once GCAP avionics and autonomy modules mature.

Terrestrial systems emphasize 8X8 wheeled vehicles and 155mm howitzers optimized for island maneuvering, whereas naval platforms target frigates and submarines fitted with lithium-ion batteries for extended, silent patrols. All three domains converge on sensor fusion, EW, and secure data links, prompting cross-domain component commonality that lowers sustainment cost and strengthens the Japan aerospace and defense market.

The Japan Aerospace and Defense Market Report is Segmented by Sector (Aerospace and Defense), Platform (Aerial, Terrestrial, Naval, and Space), Service Type (Manufacturing and Maintenance, Repair, and Overhaul), and Component (Airframes and Structures, Propulsion Systems and Engines, Electronics and Mission Systems, Composite Materials and Carbon Fiber, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi Heavy Industries, Ltd.

- Kawasaki Heavy Industries, Ltd.

- ShinMaywa Industries, Ltd.

- Toshiba Corporation

- IHI AEROSPACE Co., Ltd.

- SUBARU CORPORATION

- Toray Advanced Composites

- Lockheed Martin Corporation

- BAE Systems plc

- The Boeing Company

- Northrop Grumman Corporation

- Thales Group

- NEC Corporation

- Fujitsu Limited

- Sojitz Aerospace Corporation

- ANA HOLDINGS

- JAL Engineering Co.

- Airbus SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising defense spending aligned with the 2% of GDP target

- 4.2.2 Expansion of next-generation fighter aircraft and combat aviation programmes

- 4.2.3 Post-pandemic recovery in commercial aviation MRO demand

- 4.2.4 Government incentives for indigenous missile and hypersonic system development

- 4.2.5 Transition toward domestic MRO hubs under the US-Japan forward sustainment strategy

- 4.2.6 Build-out of defense satellite constellations supporting surveillance and targeting

- 4.3 Market Restraints

- 4.3.1 Stringent export-control policies limiting production scale and market expansion

- 4.3.2 Advanced manufacturing talent shortages and supply chain bottlenecks

- 4.3.3 Increasing cybersecurity and regulatory compliance costs for defense SMEs

- 4.3.4 Dependence on foreign intellectual property and licensing for core defense platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sector

- 5.1.1 Aerospace

- 5.1.1.1 Civil Aerospace

- 5.1.1.2 Military Aerospace

- 5.1.2 Defense

- 5.1.2.1 Land Systems

- 5.1.2.2 Naval Systems

- 5.1.2.3 Air Combat Systems

- 5.1.1 Aerospace

- 5.2 By Platform

- 5.2.1 Aerial

- 5.2.1.1 Fixed Wing Aircraft

- 5.2.1.2 Rotary Wing Aircraft

- 5.2.1.3 Unmanned Aerial Systems

- 5.2.2 Terrestrial

- 5.2.2.1 Armored Vehicles

- 5.2.2.2 Artillery and Missile Systems

- 5.2.2.3 Soldier Systems and Electronics

- 5.2.3 Naval

- 5.2.3.1 Surface Combatants

- 5.2.3.2 Submarines

- 5.2.3.3 Naval Aviation

- 5.2.4 Space

- 5.2.4.1 Navigation Satellites

- 5.2.4.2 Earth Observation/Remote Sensing Satellites

- 5.2.4.3 Scientific Research/Astronomical Satellites

- 5.2.4.4 Communication Satellites

- 5.2.1 Aerial

- 5.3 By Service Type

- 5.3.1 Manufacturing

- 5.3.2 Maintenance, Repair, and Overhaul (MRO)

- 5.4 By Component

- 5.4.1 Airframes and Structures

- 5.4.2 Propulsion Systems and Engines

- 5.4.3 Electronics and Mission Systems

- 5.4.4 Composite Materials and Carbon Fibre

- 5.4.5 Electronic Warfare (EW) and Sensors

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Mitsubishi Heavy Industries, Ltd.

- 6.4.2 Kawasaki Heavy Industries, Ltd.

- 6.4.3 ShinMaywa Industries, Ltd.

- 6.4.4 Toshiba Corporation

- 6.4.5 IHI AEROSPACE Co., Ltd.

- 6.4.6 SUBARU CORPORATION

- 6.4.7 Toray Advanced Composites

- 6.4.8 Lockheed Martin Corporation

- 6.4.9 BAE Systems plc

- 6.4.10 The Boeing Company

- 6.4.11 Northrop Grumman Corporation

- 6.4.12 Thales Group

- 6.4.13 NEC Corporation

- 6.4.14 Fujitsu Limited

- 6.4.15 Sojitz Aerospace Corporation

- 6.4.16 ANA HOLDINGS

- 6.4.17 JAL Engineering Co.

- 6.4.18 Airbus SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment