PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035129

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035129

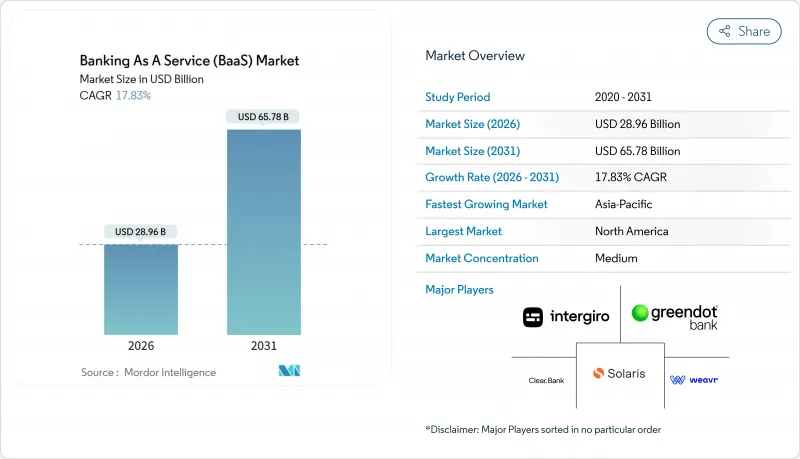

Banking As A Service (BaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The banking as a service market size is USD 28.96 billion in 2026 and is projected to reach USD 65.78 billion by 2031 at a 17.83% CAGR.

This trajectory reflects a structural shift as ISO 20022 adoption standardizes payment messaging and compresses integration timelines for bank connectivity via APIs. Growth also aligns with open banking mandates that normalize permissioned data sharing and expand developer access to account and payment functionality across regions. Embedded finance models are scaling within vertical software and marketplace platforms, which monetize financial workflows such as acceptance, payouts, and working capital without carrying licenses. Instant payment infrastructure and data portability rules are reinforcing this platform-led distribution of financial services across the banking-as-a-service market.

Global Banking As A Service (BaaS) Market Trends and Insights

Rising Adoption of Open-Banking Regulations

Mandatory account data-sharing frameworks are enabling providers in the banking-as-a-service market to deliver payment initiation and account aggregation on top of incumbent systems through standardized APIs. The United Kingdom reported 13.3 million active open banking users in 2025, alongside 31 million open banking payments made, underscoring scalable demand for API-based connectivity in consumer and merchant journeys. Canada's Consumer-Driven Banking framework under Bill C-69 targets a phased launch in early 2026 and aligns with ISO 20022-based real-time rails, which support interoperable data payloads for more reliable clearing and settlement. India's UPI processed 131.1 billion transactions in fiscal 2024 and runs in multiple countries, which demonstrates how open-loop API rails can serve as cross-border infrastructure for the banking-as-a-service market. Across major markets, rulemaking and implementation timetables continue to normalize consumer-permissioned data access, which strengthens the foundations for embedded experiences and partnerships.

Digital Transformation Initiatives Among Incumbent Banks

Banks are shifting from monolithic cores to API-first architectures to accelerate product launches and integrate real-time payment, onboarding, and fraud capabilities within weeks rather than quarters across the banking-as-a-service market. SWIFT's final migration deadline in November 2025 for ISO 20022 has driven structured, machine-readable data fields that improve reconciliation and screening use cases across payment flows. The Federal Reserve completed the Fedwire Funds Service migration to ISO 20022 on July 14, 2025, enabling enriched remittance data that can reduce manual intervention and exception handling. A Bank for International Settlements survey indicates that many real-time gross settlement operators plan to expose APIs within the medium term, signalling a steady expansion of direct interconnectivity pathways. These investments channel demand to orchestration platforms that bundle compliance workflows, ledgering, and network connectivity in the banking-as-a-service market.

Heightened Regulatory Scrutiny on Sponsor Banks

United States agencies clarified in July 2024 that banks remain fully accountable for compliance and safety obligations when partnering with fintechs, which has increased due diligence requirements and tightened oversight across the banking-as-a-service market. The FDIC proposed enhanced recordkeeping in September 2024 for deposit accounts held on behalf of multiple consumers, a response aimed at improving reconciliation and customer protections when third parties are involved. Recent supervisory actions have prompted several banks to reassess onboarding standards and reserve practices for partner programs as examiners evaluate third-party arrangements. European guidance on outsourcing imposes requirements for exit plans, data portability, and audit rights, which increase contractual complexity and ongoing monitoring costs for bank-fintech partnerships. These steps raise the bar for documentation, controls, and operational resilience across the sponsor ecosystem that underpins the banking-as-a-service market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Embedded-Finance Revenue Models

- API Standardization Lowering Integration Costs

- Complex Cross-Border Compliance Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payment Gateway captured 33.79% of the banking as a service market share in 2025, reflecting broad adoption of virtual cards to streamline corporate spend and procurement. The segment's role in the banking as a service market is reinforced by merchant and enterprise demand for instant payouts, tokenized credentials, and richer ISO 20022 data for reconciliation. Embedded Finance Software is forecasted to grow at 22.12% through 2031 as vertical SaaS platforms integrate lending and acceptance, which expands addressable revenue beyond subscription fees. Bank Account and Core Banking modules enable deposit accounts with associated KYC and ledger capabilities that can be surfaced through APIs to non-bank brands. Lending and Credit Services leverage cash flow data and platform histories to underwrite segments that traditional models underserved, a pattern visible in point-of-sale installment adoption.

Mastercard expanded an embedded virtual-card program with SAP Concur and SAP Taulia in 2025, inserting one-time-use credentials into booking and invoice workflows to limit fraud exposure and support straight-through processing. As enterprise workflows standardize around API-based payouts and acceptance, providers in the banking as a service market are packaging fraud controls, sanctions screening, and onboarding checks as managed services. Affirm reported 23 million active consumers by June 2025, which signals momentum for embedded credit models that are integrated at checkout or invoice submission. TransUnion reported that fintechs originated a significant portion of new personal loan balances in 2025, which shows rising trust in digital origination and alternative data models where permitted. These shifts pull more transaction volume, and lending flows toward modular stacks across the banking-as-a-service market.

Large Enterprises held 62.18% of deployments in 2025 due to complex treasury, multi-entity operations, and audit needs that benefit from industrial-grade API orchestration and evidence-grade logging. These buyers also require resilience, scalability, and integration to existing ERP systems, which sustains demand for bank-grade controls in the banking as a service market. Small and Medium Enterprises are projected to grow at a 20.42% CAGR as independent software vendors bundle acceptance, issuing, payouts, and reconciliation into single dashboards. This approach simplifies back-office tasks and reduces manual reconciliation as financial operations become embedded in the software SMEs already use. The banking-as-a-service market continues to add features that reduce setup effort and time to value for smaller firms, which accelerates adoption when paired with vertical workflow integrations.

Banks and platforms are expanding co-branded offerings that let software vendors integrate business banking and payment features while the bank maintains regulatory relationships. U.S. Bank expanded its embedded payments suite in 2025 with new API endpoints for issuing, acquiring, and real-time payouts, a model that aligns with SME needs for fast onboarding and unified reporting. Green Dot announced a strategic split in November 2025 that created separate bank and non-bank entities, a move intended to align balance-sheet capacity and risk oversight with large-scale sponsor programs. These steps illustrate how the banking-as-a-service industry aligns infrastructure with distinct buyer needs across enterprise tiers while safeguarding compliance and operational continuity. Adoption patterns in this segment are likely to remain stable as large customers prioritize reach and resilience, and SMEs emphasize speed and simplicity.

The Banking As A Service Market Report is Segmented by Product Type (Payment Gateway, Bank Account and Core Banking, and More), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End User (Banks, Fintech Corporations, Other End Users), Component (Platform and Infrastructure, Services), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value in USD.

Geography Analysis

North America held 35.33% of the banking as a service market share in 2025. The FedNow Service expanded from launch to more than 1,500 participating institutions by late 2025, which strengthened the case for API-exposed instant payouts and bill pay in retail and commercial contexts. Consumer research also reflects strong preferences for faster payments that support everyday transactions, which encourages banks and platforms to integrate request for pay and instant disbursements. Request for pay is expected to gain commercial adoption as treasury and billing platforms automate collection flows within embedded finance journeys. Interoperability between Canada's Real-Time Rail and the country's Consumer-Driven Banking framework is set to reinforce API connectivity with real-time, ISO 20022-rich clearing.

Asia-Pacific is projected to grow at 21.05% through 2031 on the strength of real-time infrastructure and API-based innovations. India's UPI processed 20.47 billion transactions in November 2025 and continues to extend into additional markets, which expands cross-border use cases for API-initiated payments. The program's share of retail digital payments underscores the scale of API-first rails supporting embedded experiences. Japan's policy and industry steps to increase cashless adoption, together with bank investments in digital transformation, sustain the case for modern payment and onboarding stacks. Regional hubs such as Singapore are providing grants and sandboxes that encourage adoption of advanced financial technology and data sharing.

Europe, the Middle East, and Africa display varied adoption patterns shaped by payment regulation and supervisory frameworks. The European Payments Council's SEPA Instant requirements effectively mainstreamed euro instant payments, and DORA elevated resilience obligations for ICT providers that serve financial institutions. The United Kingdom counted 13.3 million open banking users in 2025 with growing monthly payment volumes, reinforcing the role of standardized APIs in retail and small-business flows. Central banks in the Gulf have advanced multi-jurisdiction projects that pilot cross-border settlements and have introduced guidance for digital assets that interact with traditional banking. Regulatory modernization across these regions reinforces the case for unified compliance and technical orchestration within the banking-as-a-service market.

- Solaris SE

- ClearBank

- Green Dot Corp.

- Intergiro

- Weavr

- Velmie

- Treasury Prime

- MatchMove Pay Pte Ltd

- Railsr (BNKBL Ltd.)

- Treezor

- Starling Bank

- NymCard

- Column

- FIS

- FISERV

- Agora Financial Technologies

- Episode Six

- Unit Finance

- Griffin

- Alviere

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of open-banking regulations

- 4.2.2 Digital transformation initiatives among incumbent banks

- 4.2.3 Shift toward embedded-finance revenue models

- 4.2.4 API standardization lowering integration costs

- 4.2.5 Surging VC funding for BaaS infrastructure start-ups

- 4.2.6 Generative-AI-driven hyper-personalization of financial products

- 4.3 Market Restraints

- 4.3.1 Heightened regulatory scrutiny on sponsor banks

- 4.3.2 Complex cross-border compliance requirements

- 4.3.3 Rising fintech failures are increasing counterparty risk

- 4.3.4 Cloud-concentration risk with a handful of hyperscalers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Payment Gateway

- 5.1.2 Bank Account/Core Banking

- 5.1.3 Lending and Credit Services

- 5.1.4 Embedded Finance Software

- 5.1.5 Other Product Types

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small & Medium Enterprises (SMEs)

- 5.3 By End User

- 5.3.1 Banks

- 5.3.2 Fintech Corporations

- 5.3.3 Other End Users

- 5.4 By Component

- 5.4.1 Platform / Infrastructure

- 5.4.2 Services (Compliance, KYC, Fraud, etc.)

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Solaris SE

- 6.4.2 ClearBank

- 6.4.3 Green Dot Corp.

- 6.4.4 Intergiro

- 6.4.5 Weavr

- 6.4.6 Velmie

- 6.4.7 Treasury Prime

- 6.4.8 MatchMove Pay Pte Ltd

- 6.4.9 Railsr (BNKBL Ltd.)

- 6.4.10 Treezor

- 6.4.11 Starling Bank

- 6.4.12 NymCard

- 6.4.13 Column

- 6.4.14 FIS

- 6.4.15 FISERV

- 6.4.16 Agora Financial Technologies

- 6.4.17 Episode Six

- 6.4.18 Unit Finance

- 6.4.19 Griffin

- 6.4.20 Alviere

7 Market Opportunities & Future Outlook

- 7.1 Monetization of banking infrastructure by incumbent banks

- 7.2 Cloud platforms drive demand for BaaS providers offering payments and KYC/AML