PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035130

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035130

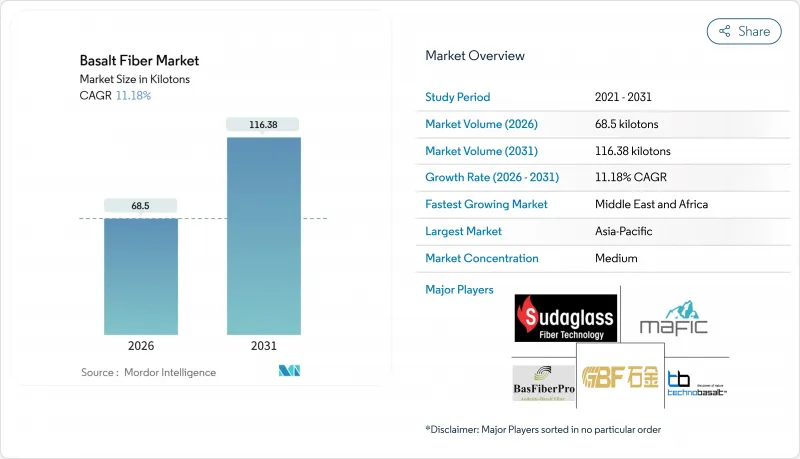

Basalt Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Basalt Fiber Market size is estimated at 68.5 kilotons in 2026, and is expected to reach 116.38 kilotons by 2031, at a CAGR of 11.18% during the forecast period (2026-2031).

The surge is tied to infrastructure decarbonization programs, offshore wind construction, and vehicle lightweighting mandates that reward basalt fiber's superior corrosion and heat resistance. Global producers are scaling capacity to address demand for continuous rovings in turbine blades and automotive body panels, while discrete fiber formats for concrete mixes and insulation gain traction. Regulatory recognition in major codes, coupled with heightened lifecycle-cost scrutiny, is compressing the adoption curve. Intensifying competition and early technical approvals signal a pivotal phase for the basalt fiber market over the next five years.

Global Basalt Fiber Market Trends and Insights

EU Net-Zero Mandates Accelerating Basalt Rebar

The revised EU Net-Zero Industry Act compels project owners to adopt low-GWP reinforcements, placing basalt rebar on specification lists for bridge decks and seawalls. Tensile strengths of 800-1,200 MPa and triple the corrosion resistance of steel lengthen service life to 100 years in chloride-rich environments. EN 13706 now references basalt, removing earlier regulatory gaps. France and Germany are piloting basalt rebar in bridge deck overlays and coastal infrastructure, where chloride ingress has historically required steel replacement every 25 years. This regulatory push is compressing payback periods for basalt rebar to under 15 years in high-exposure applications, making it economically viable for public infrastructure budgets constrained by net-zero compliance costs.

Offshore Wind-Blade Build-Out Needs Heat-Resistant Fabrics

Next-generation 15 MW turbines require spar caps that withstand curing exotherms and lightning strikes. Basalt retains strength up to 650°C, outperforming E-glass at 460°C. Flexural strengths of roughly 400 MPa support 120-meter blade spans. The American Bureau of Shipping's guide for floating offshore wind turbines references basalt fiber as a compliant reinforcement for mooring and dynamic cable protection systems, signaling regulatory acceptance that will accelerate adoption in the 80-gigawatt offshore wind pipeline planned for the North Sea and East China Sea through 2030.

Easy Availability of Substitutes

Glass fiber maintains a 10-to-1 cost advantage over basalt fiber in non-performance-critical applications such as general-purpose composites and insulation, limiting basalt's penetration into the 7-million-tonne-per-year global glass fiber market. E-glass fiber costs approximately USD 2-3 per kilogram, whereas basalt fiber ranges from USD 20-30 per kilogram, a premium justified only when thermal stability, corrosion resistance, or cryogenic performance is required. Carbon fiber, priced similarly to basalt, offers 30% higher specific strength for aerospace. Steel rebar still holds a 95% share in concrete reinforcement, thanks to entrenched codes and installer familiarity, stalling basalt uptake in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Vehicle Lightweighting Roadmap Favoring Basalt Fiber Usage

- GCC Desalination Expansion Driving Basalt FRP Pipelines

- Basalt-Ore Freight-Rate Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Continuous rovings controlled 68.18% volume in 2025 as turbine blades and auto body panels require unidirectional strength exceeding 4,800 MPa. Discrete fiber volume will expand at a 13.28% CAGR to 2031. The basalt fiber market size for discrete formats is on track to surpass 30 kilotons by 2031, driven by ready-mix concrete mixes that cut on-site labor. Tests show 1% discrete addition lifts flexural strength 25% and shrinks crack width 40% under seismic load. Continuous makers are diversifying into fiber grids for tunnel linings to defend their share.

Project owners in Asia-Pacific and the Middle East favor discrete mixes because they pour faster and meet stricter durability codes. The American Concrete Institute now offers design guidance for both continuous and discrete basalt reinforcement, closing technical gaps. Continuous suppliers leverage economies of scale, producing 6-13 µm filaments suited to high-end aerospace and premium auto parts. As building codes evolve, the basalt fiber market share of discrete formats will keep rising despite the continuous fiber's entrenched base.

The Basalt Fiber Market Report is Segmented by Form (Continuous and Discrete), Usage (Composites and Non-Composites), End-Use Industry (Building and Construction, Automotive, Industrial, Marine, Energy Industry, and Other (Sports, Chemical Industry, Petroleum Industry)), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held 48.75% volume in 2025. China leads through Hengdian's 20,000 tpa plant and additional tank-kiln lines since 2019. Japan and South Korea apply basalt in coastal retrofits, and India's USD 1.4 trillion infrastructure push fuels rebar demand. Proximity to ore and lower labor costs keep regional pricing competitive.

The Middle East and Africa, advancing at a 15.52% CAGR to 2031, will benefit from desalination and LNG investments. Saudi Aramco lists basalt FRP in corrosive service guidelines. South African mining upgrades and GCC megaprojects extend the order book, solidifying the region as the basalt fiber market's fastest-growing cluster.

North America leverages the USD 1.2 trillion Infrastructure Act, with the University of Maine's ARPA-I work aiming to update AASHTO codes. Canada deploys basalt in Arctic builds, and Mexico integrates it in EV battery enclosures. Europe's EN 13706 standards and net-zero mandates drive coastal and seismic retrofits. South America gains momentum in Brazil's hydro dam repairs and Argentina's grain silos, though import costs temper uptake.

- Albarrie Canada Limited

- Arab Basalt Fiber

- ARMBAS

- Basalt Engineering LLC

- Basaltex

- Basanite Industries LLC

- BASTECH

- Deutsche Basalt Faser GmbH

- EcoBasalt Solutions

- Fiberbas construction and building technologies

- Final Advanced Materials

- Galen Ltd

- Hengdian Group Holdings Limited

- INCOTELOGY GmbH

- Isomatex SA

- JiLin Tongxin Basalt Technology Co.,Ltd

- Kamenny Vek

- MAFIC SA

- Rockwool A/S

- Sudaglass Fiber Technology

- Technobasalt Invest

- Zhejiang Shijin Basalt Fiber Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Net-Zero Mandates accelerating basalt rebar

- 4.2.2 Offshore wind-blade build-out needs heat-resistant fabrics

- 4.2.3 Vehicle-lightweighting roadmap in several countries favoring basalt fiber usage

- 4.2.4 GCC desalination expansion driving basalt FRP pipelines

- 4.2.5 LNG platforms requiring cryogenic-tolerant reinforcements

- 4.3 Market Restraints

- 4.3.1 Easy availability of substitutes

- 4.3.2 Basalt-ore freight-rate volatility

- 4.3.3 Abrasive wear on processing equipment raising OPEX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Continuous

- 5.1.2 Discrete

- 5.2 By Usage

- 5.2.1 Composites

- 5.2.2 Non-Composites

- 5.3 By End-Use Industry

- 5.3.1 Building & Construction

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Marine

- 5.3.5 Energy Industry

- 5.3.6 Other (Sports, Chemical Industry, Petroleum Industry)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Albarrie Canada Limited

- 6.4.2 Arab Basalt Fiber

- 6.4.3 ARMBAS

- 6.4.4 Basalt Engineering LLC

- 6.4.5 Basaltex

- 6.4.6 Basanite Industries LLC

- 6.4.7 BASTECH

- 6.4.8 Deutsche Basalt Faser GmbH

- 6.4.9 EcoBasalt Solutions

- 6.4.10 Fiberbas construction and building technologies

- 6.4.11 Final Advanced Materials

- 6.4.12 Galen Ltd

- 6.4.13 Hengdian Group Holdings Limited

- 6.4.14 INCOTELOGY GmbH

- 6.4.15 Isomatex SA

- 6.4.16 JiLin Tongxin Basalt Technology Co.,Ltd

- 6.4.17 Kamenny Vek

- 6.4.18 MAFIC SA

- 6.4.19 Rockwool A/S

- 6.4.20 Sudaglass Fiber Technology

- 6.4.21 Technobasalt Invest

- 6.4.22 Zhejiang Shijin Basalt Fiber Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Increasing Adoption of Environmentally Friendly Materials