PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035147

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035147

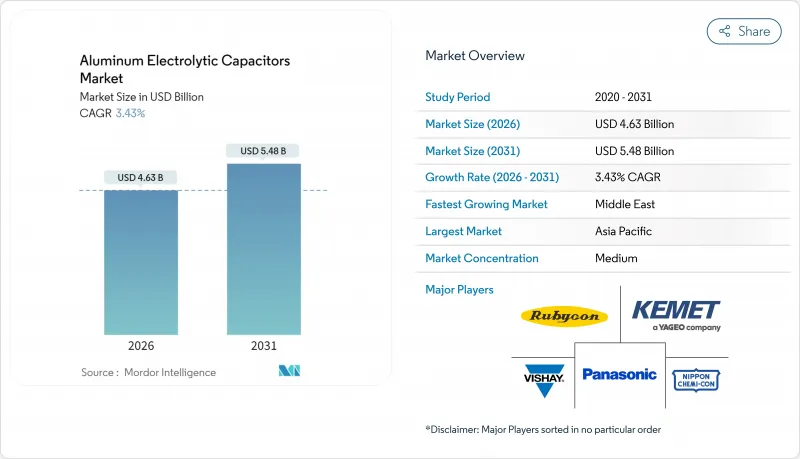

Aluminum Electrolytic Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The aluminum electrolytic capacitors market size is USD 4.63 billion in 2026 and is forecast to reach USD 5.48 billion by 2031, reflecting a 3.43% CAGR through the period.

Momentum stems from a shift toward high-voltage inverter topologies, 800 V electric-vehicle (EV) battery platforms, and wide-bandgap power devices that demand lower equivalent series resistance (ESR) and longer lifetime. Component miniaturization in smartphones, higher ripple-current densities in EV traction inverters, and renewable-energy mandates in the Middle East are reshaping product design and geographic demand patterns. Supplier strategies now emphasize hybrid polymer technology, captive etched-foil capacity, and automotive reliability qualifications to offset aluminum price volatility. At the same time, regional specialists leverage proximity and cost advantages to win design slots in consumer electronics and industrial automation.

Global Aluminum Electrolytic Capacitors Market Trends and Insights

Shrinking PCB Real Estate Driving Ultra-Miniaturised Capacitors

Power-management circuits in smartphones and tablets continue to shrink, forcing suppliers to deliver identical capacitance in packages occupying 30% less board area than 2023 designs. Surface-mount aluminum electrolytic capacitors under 3 mm profile are displacing parallel banks of ceramics that create acoustic noise, an advantage demonstrated by Nichicon's GYG hybrid series released in 2025. Demand is concentrated in Asia Pacific, where contract manufacturers prioritize square-millimetre savings to sustain razor-thin margins. The driver's 0.5% uplift to the overall CAGR reflects the sheer shipment volume of mobile devices. Capital investment in low-profile polymer cathode lines underlines the transition from traditional liquid electrolytes. Suppliers that cannot meet miniaturization roadmaps risk exclusion from next-generation handset reference designs.

Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

Automakers are migrating from 400 V to 800 V pack voltages to shorten DC-fast-charging sessions and trim copper mass. The change doubles voltage stress on DC-link capacitors and pushes ripple current beyond 50 A RMS, overheating conventional liquid-electrolyte parts. Panasonic's ZL automotive series and Eaton's EHBSA hybrid family illustrate the move to AEC-Q200 hybrid polymer solutions rated at 135 °C and ESR below 10 mΩ. EV adoption drives a 0.7% boost to market CAGR, with North America and Europe joining China in high-voltage rollouts. Onboard charger and traction-inverter suppliers increasingly stipulate polymer cathodes to eliminate derating, locking in higher average-selling-price (ASP) growth.

Aluminium Price Volatility Compressing Margins

London Metal Exchange spot prices reached USD 2,955 per metric ton in December 2025, 20% higher than early-year forecasts, trimming gross margins for capacitor makers locked into three-month customer price lists. Etched foil comprises roughly 30% of bill-of-material cost, and a 60- to 90-day pass-through lag hampers price adjustments. The U.S. Department of Energy's proposed carbon-border adjustments could add further cost pressure in coal-reliant grid regions. Smaller firms under USD 100 million revenue lack hedging leverage, heightening bankruptcy risk and limiting R&D budgets.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investments in Utility-Scale Solar Inverters

- Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- Supply Risk of High-Purity Etched Foil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-voltage aluminum electrolytic capacitors above 500 V are forecast to grow at 4.4% annually, eclipsing the 3.43% aluminum electrolytic capacitors market CAGR as solar inverters and industrial drives lift DC-bus voltages for efficiency. Low-voltage parts still command 64.21% of 2025 revenue thanks to phones, tablets, and 12-48 V automotive rails. High-voltage oxide layers require anodization precision near 1.2 nm per volt, pushing cleanroom investments and inline defect inspection.

Utility-scale solar projects in the Middle East and 800 V EV onboard chargers blur segmentation boundaries, with 450-500 V capacitors straddling both tiers. Panasonic's ZL series targets this crossover with 135 °C endurance, underscoring thermal-management challenges in under-hood environments. As wide-bandgap semiconductors enable intermediate 600-700 V buses, the aluminum electrolytic capacitors market is likely to realign around new voltage clusters rather than the historical 500 V breakpoint.

Solid polymer capacitors should advance at 4.9% CAGR on the back of 5G base-station thermal demands, while non-solid liquid designs held 61.47% share in 2025. Hybrid polymer parts that marry aluminium oxide anodes with conductive-polymer cathodes bridge cost and performance gaps, extending life to 10,000 hours at 105 °C.

Solid polymer reliability above 125 °C remains a hurdle: conductive polymers degrade, limiting automotive under-hood deployment. Liquid electrolytes therefore retain dominance in applications below 85 °C and currents under 2 A RMS. The aluminum electrolytic capacitors market size for hybrid polymer formats is expected to expand steadily as qualification data accumulates, especially in automotive DC-DC converters where ESR dictates thermal-design budgets.

The Aluminum Electrolytic Capacitors Market Report is Segmented by Voltage (High Voltage (Above 500 V), and Low Voltage (Up To 500 V)), Electrolyte Type (Non-Solid Liquid, Solid Polymer, and Hybrid Polymer), Mounting Configuration (Surface-Mount, Through-Hole (Radial, and Axial), and More), Application (Industrial Automation, Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 45.38% of 2025 revenue, anchored by Chinese smartphone assembly plants, Japanese auto electronics, and Korean foundries. Domestic demand plus export volumes make the region the epicentre of the aluminum electrolytic capacitors market. Governments in Thailand, Malaysia, and Vietnam offer tax holidays, drawing capacity from Murata, Panasonic, and others.

The Middle East posts the fastest 4.7% CAGR thanks to giga-scale solar farms such as Saudi Arabia's 10 GW NEOM project and the United Arab Emirates' 2.6 GW Mohammed bin Rashid Al Maktoum Solar Park. Inverters for these plants need 600-900 V capacitors rated for 100,000 hours at 85 °C, boosting high-voltage demand. Hitachi Energy's Xi'an line tripled output in 2025 to serve Gulf Cooperation Council installations, underlining the region's pull-on Chinese capacity.

North America benefits from EV assembly expansions and hyperscale datacentre builds that require low-ESR DC-bus capacitance. Europe faces energy-price headwinds but sustains premium demand for automotive and industrial parts through electrification mandates. South America grows from a smaller base, led by Brazilian auto suppliers adopting hybrid platforms, while Africa remains an emerging market focused on off-grid solar controllers.

- Nippon Chemi-Con Corporation

- Panasonic Holdings Corporation

- Yageo Corporation (KEMET)

- Vishay Intertechnology Inc.

- Nichicon Corporation

- Rubycon Corporation

- TDK Corporation (EPCOS Brand)

- Cornell Dubilier Electronics

- Lelon Electronics Corporation

- Samwha Capacitor Group

- Nantong Jianghai Capacitor Co.

- NIC Components Corp.

- Elna Co., Ltd.

- Suncon (Sanyo)

- Illinois Capacitor (Cornell)

- Hitano Enterprise Corp.

- Samyoung Electronics Co., Ltd.

- Taiwan Chinsan Electronics Industrial Co., Ltd.

- Cheng Tung Industrial Co., Ltd.

- CapXon Group

- Jianghai Europe Electronic Components GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shrinking PCB Real Estate Driving Ultra-miniaturised Capacitors

- 4.2.2 Push Toward 800 V Battery Systems in EVs Elevates Ripple Current Requirements

- 4.2.3 Growing Investments in Utility-Scale Solar Inverters

- 4.2.4 Government Incentives for Smart Manufacturing (Industry 4.0)

- 4.2.5 Wide-bandgap Power Devices Creating Need for Low-ESR Bulk Capacitance

- 4.2.6 Edge AI Hardware Proliferation in 5G Base-Stations

- 4.3 Market Restraints

- 4.3.1 Aluminium Price Volatility Compressing Margins

- 4.3.2 Supply Risk of High-Purity Etched Foil

- 4.3.3 Solid Polymer Reliability Concerns Above 125 °C

- 4.3.4 Design-in Shift Toward Multi-layer Polymer Capacitors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Buyers

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Voltage

- 5.1.1 High Voltage (Greater than 500 V)

- 5.1.2 Low Voltage (Up to 500 V)

- 5.2 By Electrolyte Type

- 5.2.1 Non-solid (Liquid) Electrolyte

- 5.2.2 Solid Polymer Electrolyte

- 5.2.3 Hybrid Polymer

- 5.3 By Mounting Configuration

- 5.3.1 Surface-Mount

- 5.3.2 Through-Hole (Radial, Axial)

- 5.3.3 Snap-In

- 5.3.4 Screw Terminal

- 5.3.5 Other Mounting Configurations

- 5.4 By Application

- 5.4.1 Industrial Automation

- 5.4.2 Telecommunications

- 5.4.3 Consumer Electronics

- 5.4.4 Automotive (ICE and EV)

- 5.4.5 Energy and Power

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nippon Chemi-Con Corporation

- 6.4.2 Panasonic Holdings Corporation

- 6.4.3 Yageo Corporation (KEMET)

- 6.4.4 Vishay Intertechnology Inc.

- 6.4.5 Nichicon Corporation

- 6.4.6 Rubycon Corporation

- 6.4.7 TDK Corporation (EPCOS Brand)

- 6.4.8 Cornell Dubilier Electronics

- 6.4.9 Lelon Electronics Corporation

- 6.4.10 Samwha Capacitor Group

- 6.4.11 Nantong Jianghai Capacitor Co.

- 6.4.12 NIC Components Corp.

- 6.4.13 Elna Co., Ltd.

- 6.4.14 Suncon (Sanyo)

- 6.4.15 Illinois Capacitor (Cornell)

- 6.4.16 Hitano Enterprise Corp.

- 6.4.17 Samyoung Electronics Co., Ltd.

- 6.4.18 Taiwan Chinsan Electronics Industrial Co., Ltd.

- 6.4.19 Cheng Tung Industrial Co., Ltd.

- 6.4.20 CapXon Group

- 6.4.21 Jianghai Europe Electronic Components GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment