PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035150

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035150

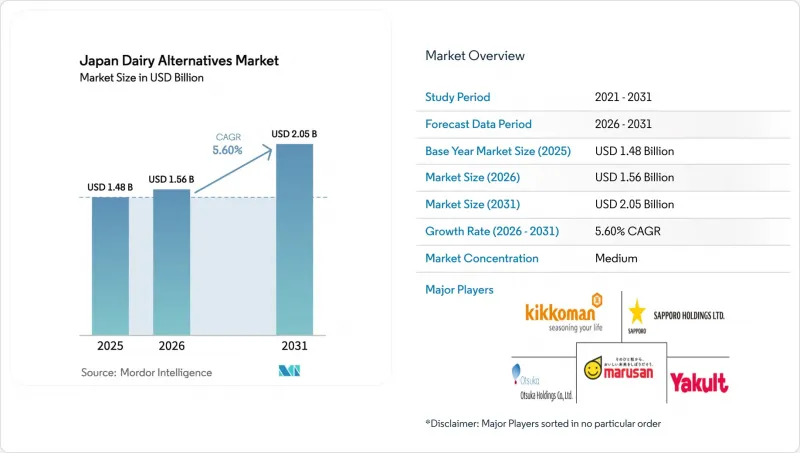

Japan Dairy Alternatives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Japan Dairy Alternatives Market size in 2026 is estimated at USD 1.56 billion, growing from 2025 value of USD 1.48 billion with 2031 projections showing USD 2.05 billion, growing at 5.60% CAGR over 2026-2031.

This growth trajectory reflects Japan's evolving dietary landscape, where traditional dairy consumption patterns intersect with rising health consciousness and demographic shifts. The market's expansion is underpinned by Japan's aging population, with 29.1% of citizens over 65 years old, creating heightened demand for digestible alternatives to conventional dairy products . Rising health consciousness, transparent labeling, and demographic aging underpin this steady growth in the Japan non-dairy products market. Manufacturers continue to refine protein functionality through fermentation technology, delivering products that approximate dairy taste while remaining easier to digest for the 85% of adults who show lactose malabsorption. Macroeconomic headwinds-including a 17% jump in average food prices in 2024-have not derailed demand; instead, they have accelerated premiumization, positioning non-dairy alternatives as functional food options rather than simple substitutes. Retailers respond by expanding shelf space, while food-service operators leverage plant-based offerings to refresh post-pandemic menus, further normalizing non-dairy choices among mainstream consumers in the Japan non-dairy products market.

Japan Dairy Alternatives Market Trends and Insights

Rising Awareness of Lactose Intolerance

Japan's genetic predisposition to lactose intolerance affects approximately 85% of the adult population, yet awareness of this condition has only recently gained mainstream recognition through healthcare initiatives and media coverage. The Ministry of Health, Labour and Welfare's 2024 dietary guidelines explicitly acknowledge lactose sensitivity as a nutritional consideration, marking a significant policy shift from traditional dairy promotion strategies . This official recognition catalyzes consumer education campaigns by healthcare providers, creating informed demand for lactose-free alternatives. The demographic most responsive to this messaging includes urban professionals aged 25-45, who demonstrate higher health literacy and disposable income to support premium non-dairy purchases. Pharmaceutical companies like Otsuka Holdings have leveraged this trend by positioning their plant-based products as functional foods rather than mere dairy substitutes, emphasizing digestive wellness benefits. The regulatory framework supporting this driver includes JAS (Japanese Agricultural Standards) labeling requirements that mandate clear lactose content disclosure, enabling consumers to make informed dietary choices.

Convenient, Ready-to-Drink Packaging Options

Japan's convenience-oriented culture drives packaging innovation that prioritizes portability, shelf stability, and single-serving formats aligned with on-the-go consumption patterns. The success of ready-to-drink formats reflects deeper societal shifts toward time-compressed lifestyles, particularly among working professionals who increasingly rely on convenience stores for meal solutions. Ezaki Glico's "Almond Effect" line exemplifies this trend, featuring 200ml single-serve packages designed for commuter consumption, supported by celebrity endorsement campaigns featuring actress Hana Matsushima that launched in September 2024. Packaging technology advances include aseptic processing that extends shelf life without refrigeration, addressing Japan's limited cold storage infrastructure in rural convenience stores. The regulatory environment supports this driver through MHLW food safety standards that facilitate ambient-stable formulations, while packaging waste regulations incentivize lightweighting and recyclability improvements. Distribution partnerships between non-dairy producers and convenience store chains like 7-Eleven create ubiquitous availability that normalizes non-dairy consumption as part of daily routines.

High Prices Limit Mass Adoption

Non-dairy products in Japan command premium pricing that significantly constrains market penetration, with typical retail prices 2-3 times higher than conventional dairy equivalents. Teikoku Databank's 2024 food pricing analysis reveals that raw material inflation, specialized processing equipment, and limited production scale create structural cost disadvantages for plant-based alternatives. Import dependency for key ingredients like almonds and oats exposes producers to currency fluctuations and international commodity price volatility, with the yen's weakness in 2024 further pressuring input costs. Rural consumers, who face both lower average incomes and higher transportation costs for specialty products, demonstrate particularly strong price sensitivity that limits adoption rates. The challenge is compounded by Japan's deflationary economic environment, where consumers have been conditioned to expect stable or declining prices for food products. Government subsidy programs for domestic plant protein production remain limited compared to traditional dairy support, creating an uneven competitive landscape that perpetuates pricing disparities.

Other drivers and restraints analyzed in the detailed report include:

- Growing Vegan and Flexitarian Population

- Influence of Global Food Trends

- Limited Awareness in Rural Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-dairy milk maintains commanding market leadership with 89.85% share in 2025, driven by consumer familiarity and versatile application across traditional Japanese beverages and cooking. Soy milk continues as the foundational segment, leveraging Japan's centuries-old tofu manufacturing expertise and established supply chains for domestic soybean processing. Oat milk emerges as the premium growth driver, with companies like Oatly establishing local production partnerships to reduce import dependency and customize formulations for Japanese taste preferences. Almond milk faces headwinds from import cost inflation, while coconut milk benefits from established Southeast Asian trade relationships and tropical flavor acceptance in dessert applications.

The fastest-growing non-dairy cheese segment, expanding at 6.06% CAGR through 2031, reflects sophisticated consumer demand for functional dairy alternatives in traditional Japanese cuisine applications. Fermentation technology advances enable texture improvements that better replicate dairy cheese characteristics, with companies investing in precision fermentation capabilities to produce casein-like proteins. Hemp milk and hazelnut milk remain niche segments, primarily targeting health-conscious consumers willing to pay premium prices for perceived nutritional benefits. Cashew milk demonstrates potential in foodservice applications, particularly in specialty coffee shops where baristas value its frothing properties for latte art creation.

The Japan Dairy Alternatives Market is Segmented by Type (Non-Dairy Desserts, Non-Dairy Cheese, Non-Dairy Milk, Non-Dairy Yogurt, and Others), Packaging Type (PET Bottles, Cans, Cartons, Others), and Distribution Channel (Off-Trade, On-Trade). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

List of Companies Covered in this Report:

- Kikkoman Corporation

- Marusan-AI Co., Ltd.

- Ezaki Glico Co., Ltd.

- Oatly Group AB

- Sapporo Holdings Ltd.

- Otsuka Holdings Co., Ltd.

- Vitasoy International Holdings Ltd.

- Nestle S.A.

- The Coca-Cola Company

- Meiji Holdings Co., Ltd.

- Morinaga Milk Industry Co., Ltd.

- Yakult Honsha Co., Ltd.

- Tsukuba Dairy Products Co., Ltd.

- Minor Figures Ltd.

- Daiya Foods Inc.

- Elmhurst 1925 Inc.

- Vego Foods Ltd.

- Oddlygood

- Saputo Inc.

- Marinfood Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising awareness of lactose intolerance

- 4.2.2 Convenient, ready-to-drink packaging options

- 4.2.3 Growing vegan and flexitarian population

- 4.2.4 Influence of global food trends

- 4.2.5 Celebrity endorsements boost product awareness

- 4.2.6 Wider retail and e-commerce availability

- 4.3 Market Restraints

- 4.3.1 High prices limit mass adoption

- 4.3.2 Limited awareness in rural areas

- 4.3.3 Taste differs from traditional dairy

- 4.3.4 Consumer skepticism on nutritional value

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME )

- 5.1 By Type

- 5.1.1 Non-Dairy Milk

- 5.1.1.1 Oat Milk

- 5.1.1.2 Hemp Milk

- 5.1.1.3 Hazelnut Milk

- 5.1.1.4 Soy Milk

- 5.1.1.5 Almond Milk

- 5.1.1.6 Coconut Milk

- 5.1.1.7 Cashew Milk

- 5.1.2 Non-Dairy Cheese

- 5.1.3 Non-Dairy Desserts

- 5.1.4 Non-Dairy Yogurt

- 5.1.5 Others

- 5.1.1 Non-Dairy Milk

- 5.2 Packaging Type

- 5.2.1 PET Bottles

- 5.2.2 Cans

- 5.2.3 Cartons

- 5.2.4 Others

- 5.3 Distribution Channel

- 5.3.1 On-trade

- 5.3.2 Off-trade

- 5.3.2.1 Convenience Stores

- 5.3.2.2 Supermarkets and Hypermarkets

- 5.3.2.3 Online Retail Stores

- 5.3.2.4 Others Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Kikkoman Corporation

- 6.4.2 Marusan-AI Co., Ltd.

- 6.4.3 Ezaki Glico Co., Ltd.

- 6.4.4 Oatly Group AB

- 6.4.5 Sapporo Holdings Ltd.

- 6.4.6 Otsuka Holdings Co., Ltd.

- 6.4.7 Vitasoy International Holdings Ltd.

- 6.4.8 Nestle S.A.

- 6.4.9 The Coca-Cola Company

- 6.4.10 Meiji Holdings Co., Ltd.

- 6.4.11 Morinaga Milk Industry Co., Ltd.

- 6.4.12 Yakult Honsha Co., Ltd.

- 6.4.13 Tsukuba Dairy Products Co., Ltd.

- 6.4.14 Minor Figures Ltd.

- 6.4.15 Daiya Foods Inc.

- 6.4.16 Elmhurst 1925 Inc.

- 6.4.17 Vego Foods Ltd.

- 6.4.18 Oddlygood

- 6.4.19 Saputo Inc.

- 6.4.20 Marinfood Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK