PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035152

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035152

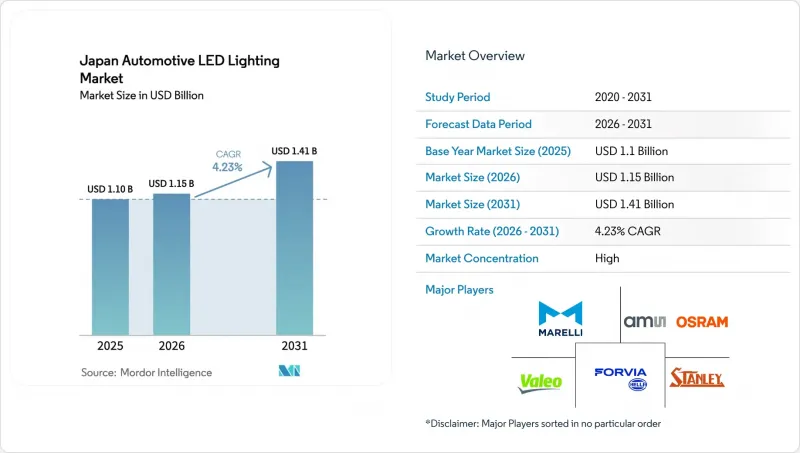

Japan Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan automotive LED lighting market size is expected to grow from USD 1.1 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 1.41 billion by 2031 at 4.23% CAGR over 2026-2031.

Steady electrification mandates, shortening LED cost curves, and stringent efficiency rules effective as of 2026 keep the growth trajectory intact as automakers integrate low-power, software-updatable lighting into next-generation battery-electric vehicle (BEV) platforms. Domestic champions Koito Manufacturing, Stanley Electric, and Ichikoh Industries reinforce a technology flywheel by funneling research and development (R&D) into adaptive driving beams (ADB), high-resolution headlamps, and sensor-lighting fusion, which in turn enables Japanese original-equipment manufacturers (OEMs) to maintain global leadership in exterior safety features. Supply-chain pressures triggered by gallium export restrictions from China have prompted manufacturers to adopt multi-regional sourcing strategies. However, ongoing Mobility DX subsidies partially offset the margin squeeze, ensuring that most model launches in 2026-2027 will feature full-LED systems as standard. Widespread 48V and zone-based electrical architectures are also streamlining wiring looms, reducing weight, and freeing energy budgets for new infotainment and autonomous driving workloads.

Japan Automotive LED Lighting Market Trends and Insights

Surging OEM demand for adaptive LED headlamps

Koito's BladeScan MEMS-based ADB elevates nighttime visibility by 40% relative to static LEDs and will scale to 16,000-pixel versions for 2025 model years, transforming lamps into predictive safety systems that cooperate with vehicle-to-vehicle messages. Toyota's rollout across premium trims underscores how ADB is shifting from luxury to baseline safety equipment, guaranteeing deep pull-through for suppliers that can refine optical algorithms, reduce power draw, and meet Japanese photometric standards.

Rapid LED cost decline and efficiency gains

Single-sided aluminum substrates and chip-on-board (COB) packaging have cut thermal resistance and slashed module bill-of-materials by more than 30%, making LEDs cost-competitive with halogen even in kei-car classes. Active-matrix driver ICs operating at 48 V trim wiring bulk and boost reliability, while research funded by the IEEE Electronics Packaging Society shows next-gen thermal interface materials sustaining lumen output over 10,000 h duty cycles.

Slower two-wheeler LED uptake outside urban prefectures

Rural riders prize repairability over sophistication, and fragmented dealer networks rarely stock LED retrofit kits certified under Japan's photometric test regimen, muting penetration until distribution and training widen.

Other drivers and restraints analyzed in the detailed report include:

- Japan's 2026-onward GHG/efficiency norms boosting LED penetration

- Integration of LEDs with ADAS sensor housings

- Dependence on imported high-power LED chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The OEM segment accounted for 84.40% of Japan automotive LED lighting market share in 2025, a dominance rooted in the deep vertical collaboration typical of Japan's keiretsu arrangements. Factory-fitted systems marry adaptive luminaires with ADAS domain controllers, making field retrofits impractical and cementing OEM volume. In value terms, the Japan automotive LED lighting market size for OEM installations hit USD 0.93 billion in 2025. OEM preference for calibrated, in-line programming sustains demand even as chip prices fall, because automakers treat lighting as core to vehicle safety ratings.

Aftermarket avenues rise at 5.38% CAGR as owners modernize halogen fleets; yet the segment stays constrained by regulatory photometry checks that require certified workshops and by limited rural dealer density. Online channels grow briskly, but professional installation packages from PIAA and Car Mate dominate revenue because vehicle inspection compliance demands beam-pattern validation equipment unavailable to do-it-yourself enthusiasts.

Passenger cars contributed 67.12% of Japan automotive LED lighting market size in 2025, reflecting the class's role as a proving ground for BladeScan, micro-LED taillamps, and welcome-light scripts. The segment's 8.29% CAGR outpaces all others as BEV rollouts multiply LED points per vehicle. Crossovers such as the 2025 RAV4 embed matrix headlamps and animated turn signals, spurring tier-one suppliers to accelerate pixel counts and low-glare algorithms.

Commercial vans and light trucks adopt LEDs primarily for durability; ROI stems from longer service intervals rather than branding. Heavy trucks migrate to LED clusters that integrate fog, DRL, and cornering functions, reducing harness weight by up to 3 kg per cab. Two-wheeler adoption remains bipolar, thriving in dense prefectures where scooter sharing schemes favor energy savings yet stalling in agricultural regions sensitive to upfront premiums.

The Japan Automotive LED Lighting Market Report is Segmented by Sales Channel (OEM, and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Installation Type (New Installation, and Retrofit Installation), Application (Exterior Lighting, and Interior Lighting). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Ichikoh Industries, Ltd.

- Valeo S.A.

- HELLA GmbH & Co. KGaA

- Magneti Marelli CK Holdings Co., Ltd.

- Varroc Engineering Limited

- Hyundai Mobis Co., Ltd.

- Denso Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- ams-OSRAM AG

- Cree LED (SMART Global Holdings, Inc.)

- J.W. Speaker Corporation

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- TDK Corporation

- Seoul Semiconductor Co., Ltd.

- Rohm Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging OEM demand for adaptive LED headlamps

- 4.2.2 Rapid LED cost decline and efficiency gains

- 4.2.3 Japan's 2026-onward GHG/efficiency norms boosting LED penetration

- 4.2.4 Integration of LEDs with ADAS sensor housings

- 4.2.5 Connected-car styling customisation trend

- 4.2.6 Growth of EV platforms needing low-power lighting

- 4.3 Market Restraints

- 4.3.1 Slower two-wheeler LED uptake outside urban prefectures

- 4.3.2 Dependence on imported high-power LED chips

- 4.3.3 Aftermarket price wars squeezing margins

- 4.3.4 Rising rare-earth material costs for phosphors

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sales Channel

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Exterior Lighting

- 5.4.1.1 Headlamps

- 5.4.1.2 Daytime Running Lights

- 5.4.1.3 Taillights

- 5.4.1.4 Fog Lamps

- 5.4.1.5 Turn Signals

- 5.4.1.6 Other Exterior Lightings

- 5.4.2 Interior Lighting

- 5.4.2.1 Dome and Map Lights

- 5.4.2.2 Ambient Lighting

- 5.4.2.3 Instrument Cluster and Infotainment Backlighting

- 5.4.2.4 Others Interior Lightings

- 5.4.1 Exterior Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koito Manufacturing Co., Ltd.

- 6.4.2 Stanley Electric Co., Ltd.

- 6.4.3 Ichikoh Industries, Ltd.

- 6.4.4 Valeo S.A.

- 6.4.5 HELLA GmbH & Co. KGaA

- 6.4.6 Magneti Marelli CK Holdings Co., Ltd.

- 6.4.7 Varroc Engineering Limited

- 6.4.8 Hyundai Mobis Co., Ltd.

- 6.4.9 Denso Corporation

- 6.4.10 Panasonic Automotive Systems Co., Ltd.

- 6.4.11 Nichia Corporation

- 6.4.12 Lumileds Holding B.V.

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 ams-OSRAM AG

- 6.4.15 Cree LED (SMART Global Holdings, Inc.)

- 6.4.16 J.W. Speaker Corporation

- 6.4.17 Texas Instruments Incorporated

- 6.4.18 Renesas Electronics Corporation

- 6.4.19 TDK Corporation

- 6.4.20 Seoul Semiconductor Co., Ltd.

- 6.4.21 Rohm Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment