PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035154

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035154

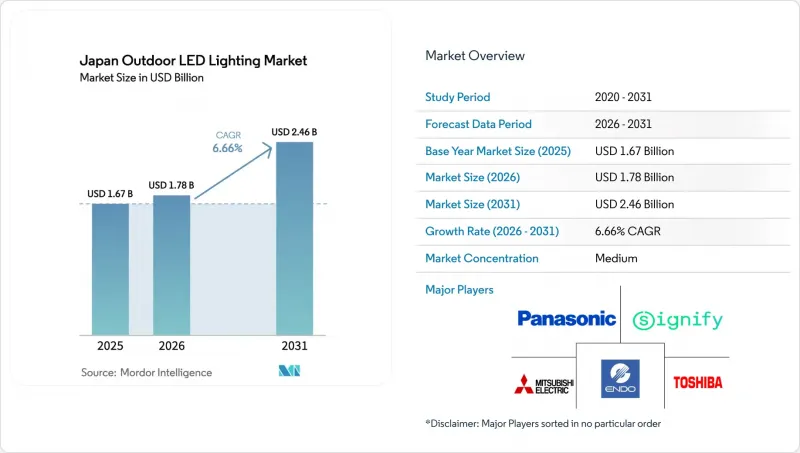

Japan Outdoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan outdoor LED lighting market size was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.78 billion in 2026 to reach USD 2.46 billion by 2031, at a CAGR of 6.66% during the forecast period (2026-2031).

Market size expansion is driven by the mandatory phase-out of mercury-vapor lamps planned for fiscal year 2026, energy-efficiency directives issued by the Agency for Natural Resources and Energy, and declining LED component prices that shorten municipal payback periods. Smart-city programs in the Tokyo-Nagoya-Osaka corridor amplify demand by bundling 5G small-cell equipment and environmental sensors with luminaires, converting lighting poles into multifunctional assets. Human-centric amber LEDs are gaining traction in environmentally sensitive areas because they reduce insect attraction and light pollution. At the same time, supply-chain exposure to imported gallium-nitride wafers and shrinking municipal budgets outside major metros challenge short-term growth.

Japan Outdoor LED Lighting Market Trends and Insights

Energy-efficiency mandates reshape procurement.

Japan's national efficiency standards oblige municipalities to meet predefined energy-intensity targets, making LED conversion a legal requirement rather than a discretionary upgrade. Local governments now bundle street, parking, and transit lighting in a single tender to maximize rebate eligibility, resulting in larger contract sizes and shorter project timelines. Transparent reporting rules enable city managers to benchmark their performance, fueling peer pressure that drives uptake among lagging jurisdictions. Penalties for non-compliance further compel rapid deployment even when capital budgets are tight.

Mercury-vapor ban compresses the replacement cycle.

Approximately 3 million mercury-vapor fixtures must be removed by the FY 2026 deadline, forcing municipalities to accelerate their upgrade schedules, which normally span a decade. The regulatory cut-off also stops the import of spare parts, leaving cities with a binary choice between full LED retrofits or non-functional lighting networks. This compressed window pulls demand forward and strains installation capacity, particularly for tunnel and bridge retrofits that need custom brackets.

Municipal budget freezes slow rural projects

COVID-19 stimulus funding ended in 2024, leaving many small cities with austerity budgets that prioritize healthcare and disaster resilience over lighting upgrades. Lengthy grant-application processes for green bonds further delay projects, resulting in a two-speed Japan outdoor LED lighting market where major metropolitan areas forge ahead while rural areas stall.

Other drivers and restraints analyzed in the detailed report include:

- Price erosion boosts ROI and rural demand.

- Smart-city corridor turns poles into digital assets.

- Retrofit complexity in Showa-era tunnels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires captured 71.63% of the Japan outdoor LED lighting market share in 2025 as municipalities favored complete system replacement for warranty coverage and uniform optical performance. The Japan outdoor LED lighting market size for luminaires benefits from integrated wireless controls and modular sensor bays that future-proof assets. Lamp-only replacements grow at 8.02% CAGR, a pace that outstrips the total market because they fit mixed-vintage poles where structural elements remain sound.

Manufacturers differentiate luminaires through cloud-managed platforms that push firmware updates and diagnostic alerts. Panasonic's LANTERNA fixture demonstrates content broadcasting, converting poles into digital signage for municipal messaging. Lamps remain popular in maintenance cycles where truck rolls coincide with routine inspection, allowing quick LED swaps without rewiring.

Street and roadway projects accounted for 47.10% of the Japan outdoor LED lighting market size in 2025, as regulatory deadlines focus on public safety corridors. Sports and stadium venues, however, post the fastest 8.78% CAGR as broadcast-grade luminance and dynamic dimming drive procurement ahead of global tournaments.

Venue owners install RGBW fixtures that synchronize with entertainment systems, enhancing spectator experience while meeting television color-rendering standards. Parking lots, transit hubs, and architectural facades follow with steady demand as falling component costs broaden the economic case for non-essential illumination upgrades.

The Japan Outdoor LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Application (Street and Roadway Lighting, Architectural and Landscape, and More), Installation Type (New Installation, and Retrofit Installation), Distribution Channel (Direct Sales, Wholesale, Retail, and E-Commerce). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Panasonic Holdings Corporation

- Toshiba Lighting and Technology Corporation

- Mitsubishi Electric Corporation

- Sharp Corporation

- Nichia Corporation

- Citizen Watch Co., Ltd.

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Iwasaki Electric Co., Ltd.

- Endo Lighting Corporation

- Odelic Co., Ltd.

- Ushio Inc.

- MinebeaMitsumi Inc.

- NEC Lighting, Ltd.

- Signify N.V.

- OSRAM GmbH

- Acuity Brands, Inc.

- Zumtobel Group AG

- Seoul Semiconductor Co., Ltd.

- Musco Sports Lighting, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency mandates from Japan's Agency for Natural Resources and Energy

- 4.2.2 Rapid phasing-out of mercury-vapor street lamps mandated for FY-2026

- 4.2.3 LED price erosion enabling faster municipal ROIs

- 4.2.4 Tokyo-Nagoya-Osaka mega-corridor smart-city projects

- 4.2.5 Growing demand for human-centric "amber" LEDs to curb insect populations

- 4.2.6 Deployment of 5G small-cell infrastructure piggy-backing on LED poles

- 4.3 Market Restraints

- 4.3.1 Budget freezes in smaller municipalities post-COVID fiscal stimulus tapering

- 4.3.2 High retrofit complexity for Showa-era tunnel lighting fixtures

- 4.3.3 Supply-chain exposure to gallium-nitride substrate imports

- 4.3.4 Increasing glare-related litigation from residential groups

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Application

- 5.2.1 Street and Roadway Lighting

- 5.2.2 Architectural and Landscape

- 5.2.3 Sports and Stadium

- 5.2.4 Tunnel and Bridge

- 5.2.5 Parking and Transit Areas

- 5.2.6 Other Applications

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Wholesale

- 5.4.3 Retail

- 5.4.4 E-commerce

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Panasonic Holdings Corporation

- 6.4.2 Toshiba Lighting and Technology Corporation

- 6.4.3 Mitsubishi Electric Corporation

- 6.4.4 Sharp Corporation

- 6.4.5 Nichia Corporation

- 6.4.6 Citizen Watch Co., Ltd.

- 6.4.7 Koito Manufacturing Co., Ltd.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Iwasaki Electric Co., Ltd.

- 6.4.10 Endo Lighting Corporation

- 6.4.11 Odelic Co., Ltd.

- 6.4.12 Ushio Inc.

- 6.4.13 MinebeaMitsumi Inc.

- 6.4.14 NEC Lighting, Ltd.

- 6.4.15 Signify N.V.

- 6.4.16 OSRAM GmbH

- 6.4.17 Acuity Brands, Inc.

- 6.4.18 Zumtobel Group AG

- 6.4.19 Seoul Semiconductor Co., Ltd.

- 6.4.20 Musco Sports Lighting, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment