PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035156

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035156

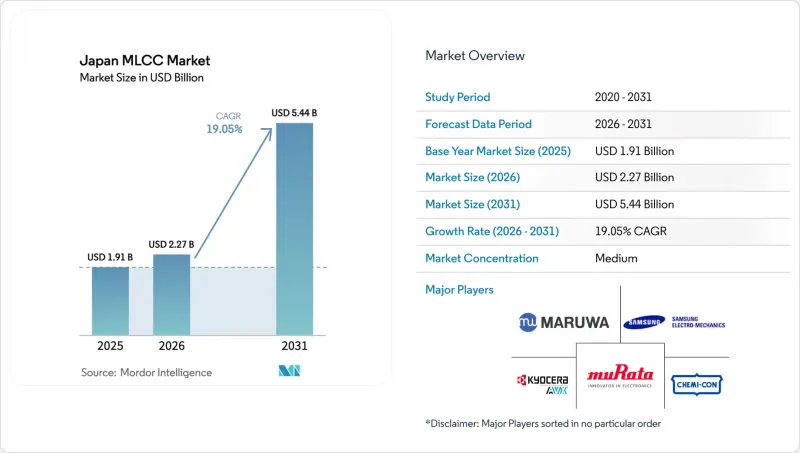

Japan MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan MLCC market size was valued at USD 1.91 billion in 2025 and estimated to grow from USD 2.27 billion in 2026 to reach USD 5.44 billion by 2031, at a CAGR of 19.05% during the forecast period (2026-2031).

The growth rests on sustained domestic leadership in automotive electrification, national 5G expansion, and high-value semiconductor investment that underpins the innovation of multilayer ceramic capacitors. Automotive OEM electrification strategies, combined with government semiconductor subsidies, provide the Japan MLCC market with clear demand visibility across powertrain, power management, and RF front-end circuits. At the same time, 5G small-cell rollouts and the adoption of Mini-LED displays raise high-frequency component needs, while industrial edge nodes elevate long-life reliability specifications. Competitive intensity remains elevated as Japanese vendors deploy advanced materials and precision manufacturing to defend differentiation against Korean and Taiwanese rivals, yet supply-chain risks tied to rare-earth sourcing and export-control compliance temper near-term margins.

Japan MLCC Market Trends and Insights

EV Powertrain MLCC Surge

Electric vehicles use six to ten times more capacitors than combustion cars, with luxury BEVs exceeding 10,000 MLCCs per unit. Domestic OEMs have pledged aggressive electrification timelines, driving demand for AEC-Q200-qualified parts rated from -55 °C to 150 °C and with 20-year lifetimes. New 100 V automotive MLCCs in the 3225 size extend capacitance thresholds while reducing pack volume. The outcome is long-cycle visibility for the Japan MLCC market as Tier-1 suppliers lock multi-year sourcing contracts with domestic vendors.

Mini-LED and Micro-LED Backlighting Demand

Display makers moving to Mini-LED backlights multiply the number of per-panel capacitor counts three to five times because every local-dimming segment includes its own driver and power filter. DNP's 50 µm diffuser film enables sub-6 mm panel thickness, forcing the use of 0402-size MLCCs with superior ESR control. Japanese suppliers leverage ceramic know-how to deliver ultra-compact parts that maintain capacitance at MHz switching frequencies, unlocking higher dollar-content per panel.

Rare-Earth and Precious-Metal Price Volatility

Sudden 200% swings in rare-earth costs squeeze dielectric and electrode margins, with every 1% uptick in geopolitical risk lifting unit import prices 0.429%. Base-metal-electrode migration eases palladium exposure, yet high-capacitance designs still rely on rare-earth dopants. Diversification into Australian and Canadian refiners mitigates future shocks but remains three to five years from commercial scale.

Other drivers and restraints analyzed in the detailed report include:

- 5G Small-Cell Infrastructure Roll-out

- IoT Edge-Node Proliferation

- Automotive PPAP Qualification Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 1 MLCCs retained a 61.95% share of the Japan MLCC market in 2025 and are expected to widen their revenue at a 20.12% CAGR through 2031. The class's low-loss, temperature-stable behavior satisfies -55 °C to 150 °C automotive powertrain envelopes. Consequently, Class 1 parts, which anchor inverter DC-link buffers and ADAS regulators, allow the Japan MLCC market size for Class 1 products to rise alongside EV penetration.

Manufacturers capture pricing premiums through proprietary ceramic chemistries and BME stacks that maintain capacitance drift within +-15% across the entire temperature spectrum. Solid-state micro-battery research further broadens Class 1 relevance as shared sintering lines cut scale-up costs.

The legacy 201 format held 55.83% share in 2025, mirroring entrenched smartphone and notebook PCB footprints. Yet the 402 format leads with 20.05% CAGR because 5G handsets and wearables adopt thinner boards. Murata's 47 µF 0402 milestone highlights how the Japanese MLCC market leverages ceramic process leadership to achieve extreme volumetric efficiency.

Thinner dielectric stacks heighten mechanical fragility, prompting soft-termination launches that disperse flex stress. Vendors deploying automated optical inspection at sub-5 µm resolution help sustain defect yields even as layer counts climb.

The Japan MLCC Market Report is Segmented by Dielectric Type (Class 1, Class 2), Case Size (201, 402, 603, 1005, 1210, Other Case Sizes), Voltage (Low Voltage, Mid Voltage, High Voltage), MLCC Mounting Type (Metal Cap, Radial Lead, Surface Mount), End-User Application (Aerospace and Defence, Consumer Electronics, Industrial, Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kyocera AVX Components Corporation

- Maruwa Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH and Co. KG

- Yageo Corporation

- Panasonic Holdings Corporation

- ROHM Co., Ltd.

- Samwha Capacitor Group Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Darfon Electronics Corp.

- Shenzhen Sunlord Electronics Co., Ltd.

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Tai-Tech Advanced Electronics Co., Ltd.

- KEMET Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Powertrain MLCC Surge

- 4.2.2 Mini-LED and Micro-LED Backlighting Demand

- 4.2.3 5G Small-Cell Infrastructure Roll-out

- 4.2.4 IoT Edge-Node Proliferation

- 4.2.5 Solid-state Battery RandD Alignment.

- 4.2.6 Smart-Manufacturing Quality-Zero Defect Push.

- 4.3 Market Restraints

- 4.3.1 Rare-earth and Precious-metal Price Volatility

- 4.3.2 Automotive PPAP Qualification Bottlenecks

- 4.3.3 High-Density Board Warpage Failures.

- 4.3.4 Geopolitical Export-Control Risks on Fabrication Tools.

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 201

- 5.2.2 402

- 5.2.3 603

- 5.2.4 1005

- 5.2.5 1210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage

- 5.3.1 Low Voltage (less than or equal to 100 V)

- 5.3.2 Mid Voltage (100 - 500 V)

- 5.3.3 High Voltage (above 500 V)

- 5.4 By MLCC Mounting Type

- 5.4.1 Metal Cap

- 5.4.2 Radial Lead

- 5.4.3 Surface Mount

- 5.5 By End-User Application

- 5.5.1 Aerospace and Defence

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunication

- 5.5.8 Other End-User Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kyocera AVX Components Corporation

- 6.4.2 Maruwa Co., Ltd.

- 6.4.3 Murata Manufacturing Co., Ltd.

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics Co., Ltd.

- 6.4.6 Taiyo Yuden Co., Ltd.

- 6.4.7 TDK Corporation

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Walsin Technology Corporation

- 6.4.10 Wurth Elektronik GmbH and Co. KG

- 6.4.11 Yageo Corporation

- 6.4.12 Panasonic Holdings Corporation

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Samwha Capacitor Group Co., Ltd.

- 6.4.15 Holy Stone Enterprise Co., Ltd.

- 6.4.16 Darfon Electronics Corp.

- 6.4.17 Shenzhen Sunlord Electronics Co., Ltd.

- 6.4.18 Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- 6.4.19 Tai-Tech Advanced Electronics Co., Ltd.

- 6.4.20 KEMET Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment