PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035157

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035157

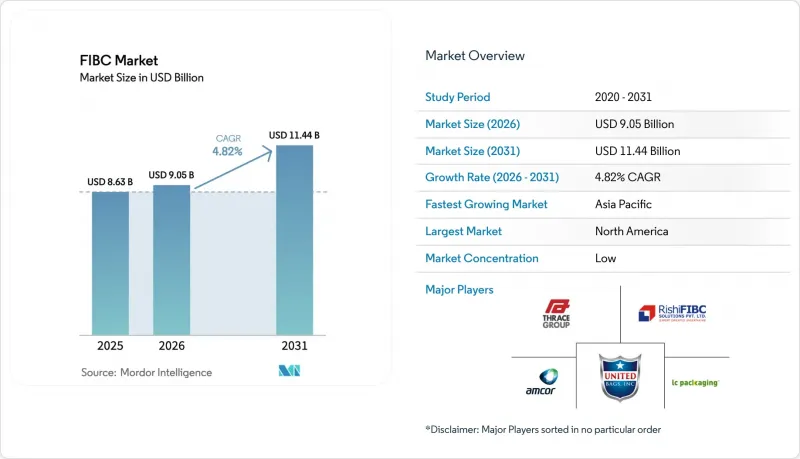

FIBC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The flexible intermediate bulk container market size is expected to grow from USD 8.63 billion in 2025 to USD 9.05 billion in 2026 and is forecast to reach USD 11.44 billion by 2031 at 4.82% CAGR over 2026-2031.

Demand continues to come from chemicals, agriculture and construction, but stronger growth now comes from sustainable packaging mandates, in-plant automation and the rapid scale-up of lithium and rare-earth supply chains. North America held the largest flexible intermediate bulk container market share at 38.74% in 2024 on the back of stringent safety rules and sizeable agricultural exports, whereas Asia-Pacific is expanding at 8.12% CAGR through 2030 on the strength of capacity additions in China, India and Southeast Asia. Tightened global hazardous-goods regulations have lifted premium demand for Type C and Type D electrostatic-safe bags, while circular-economy policies accelerate adoption of recycled-content polypropylene variants.

Global FIBC Market Trends and Insights

Food and Agro Commodities Bulk-Export Boom

Global reshoring of grain and specialty-crop supply chains is boosting demand for food-grade flexible bulk bags that lower per-unit freight cost and prevent cross-contamination. Updated U.S. agricultural-water rules effective 2024 require tighter produce traceability, pushing exporters toward barcode-ready FIBCs that integrate seamlessly with digital record systems. Countries expanding port infrastructure, such as Brazil and India, are investing in bulk-handling silos designed around FIBC discharge equipment, reinforcing mid-term growth. Commodity-price swings further encourage growers to choose flexible intermediate bulk container market solutions that cut packaging spend while protecting margins. The confluence of food-safety regulation and cost discipline therefore underpins the segment's resilience.

Hazardous-Chemical Handling Rules Boosting Demand

OSHA's 2024 alignment with UN GHS revision 7 raises the technical bar for containers that carry flammable powders and solvents. Type C and Type D bags with conductive yarns and CROHMIQ fabrics are now standard at chemical plants, pharmaceutical mixers and lithium-ore processors. Procurement managers are switching from commodity sacks to certified units despite premiums of 20-30%, viewing them as risk-mitigation assets that reduce downtime and insurance exposure. Short 18-month compliance windows have pulled forward orders, keeping utilization high for specialty lines in North America and Europe. The result is a durable uplift in the flexible intermediate bulk container market for electrostatic-safe variants.

PP Resin Price Volatility

Polypropylene feedstock swings, driven by crude-oil moves and refinery outages, make up 60-70% of bag production cost, undermining smaller converters that lack hedging tools. June 2024 resin drops offered brief relief, yet chronic uncertainty compels buyers to delay blanket orders or renegotiate quarterly. Larger manufacturers offset exposure by backward integrating into resin compounding and accelerating adoption of recycled PP, but mid-tier players face margin squeeze. The short-term drag on the flexible intermediate bulk container market gradually eases as futures-based contracts and recycled feedstocks gain traction.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Fulfilment Shift to Bulk Secondary Packaging

- Smart-FIBC Rollout for Real-Time Traceability

- Growth of Rigid-IBC Rental Pools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type A containers supplied 65.74% of 2025 demand, underscoring their value positioning across grain, cement and non-flammable chemical flows. Electrostatic-safe Type D bags, however, expand at 7.53% CAGR as lithium-ore refiners and pharmaceutical dryers specify non-grounded solutions to avert ignition risks.

Intensifying regulatory oversight and the absence of external grounding wires position Type D as the premium choice, enabling remote mines and offshore rigs to cut compliance complexity. High-tensile CROHMIQ fabrics have clocked more than 40 million safe trips, validating reliability in harsh environments and reinforcing future gains for the flexible intermediate bulk container market.

Baffle or Q-Bag variants held 34.12% share in 2025 owing to internal panels that stop bulging and unlock higher stack density, a decisive benefit for ship holds and urban DCs. U-Panel sacks track at 8.28% CAGR through 2031, supported by tight dimensional tolerances that mate smoothly with robotized filling frames.

Circular and 4-Panel designs maintain presence where maximum volume or precise discharge is required, yet continual lean-warehouse initiatives favor baffles. Automated facilities scanning pallets welcome the uniform footprint, sustaining the flexible intermediate bulk container market momentum for engineered geometries.

FIBC Market is Segmented by Type (A, B, C, D), Design (U-Panel, Baffle, Circular, 4-Panel, Others), End-User (Food, Chemicals, Pharma, Construction, Mining, Others), Capacity (Up To 500kg, 500-1000kg, 1000-1500kg, Above 1500kg), Material (Virgin PP, Recycled PP, UV PP, Paper, Bio-Based), and by Geography. Forecasts in Value (USD).

Geography Analysis

North America generated 38.25% of global revenue in 2025, underpinned by a mature chemical supply chain, high agricultural export volumes and strict OSHA compliance that favors higher-margin certified bags. The region keeps a stable growth path as asset owners reinvest in smart-packaging retrofits and domestic shale-chemicals output holds firm.

Asia-Pacific records the most rapid 7.78% CAGR due to heavy investment in battery metal refining and broad-based manufacturing expansion. China's Baotou rare-earth hub, India's production-linked incentives and Southeast Asia's agribusiness exports converge to lift regional orders for conductive and high-stack designs. Local producers such as Bulkcorp International scale capacity and secure export contracts, testifying to competitive depth that fuels the flexible intermediate bulk container market.

Europe retains a significant share by pioneering recycled-material specifications under the Green Deal and by deploying reverse logistics that complement multi-trip models. South America benefits from soy, corn and lithium-brine exports that require food-grade or heavy-duty sacks, while the Middle East and Africa gain from petrochemical expansions and infrastructure megaprojects. Regional diversification therefore spreads opportunity across the flexible intermediate bulk container market landscape.

- Greif Inc.

- Amcor Plc

- LC Packaging International BV

- Thrace Group

- Rishi FIBC Solutions Pvt Ltd

- United Bags Inc.

- Bag Corp

- Bulk Lift International LLC

- Conitex Sonoco

- Intertape Polymer Group

- Emmbi Industries Ltd

- Schoeller Allibert Group BV

- BAG Supplies Canada Ltd

- Southern Packaging LP

- Plastipak Group

- FlexiTuff International Ltd

- Bulk Pack Exports Ltd

- J&HM Dickson Ltd

- Houston Bulk Bag Co.

- Jumbo Bag Corporation

- Mule Bag Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food and agro commodities bulk export boom

- 4.2.2 Hazardous-chemical handling regulations boosting demand

- 4.2.3 E-commerce fulfilment shift to bulk secondary packaging

- 4.2.4 Smart-FIBC (IoT/RFID) rollout for real-time traceability

- 4.2.5 Paper and recycled-PP FIBC adoption under circular-economy mandates

- 4.2.6 Mining super-sack standardisation in lithium and rare-earth supply chains

- 4.3 Market Restraints

- 4.3.1 PP resin price volatility

- 4.3.2 Stringent static-dissipation certification costs

- 4.3.3 Ocean-freight container shortages disrupting FIBC supply

- 4.3.4 Growth of rigid-IBC rental pools cannibalising one-way FIBC demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Type A

- 5.1.2 Type B

- 5.1.3 Type C

- 5.1.4 Type D

- 5.2 By Design Type

- 5.2.1 U-Panel

- 5.2.2 Baffle / Q-Bag

- 5.2.3 Circular

- 5.2.4 4-Panel

- 5.2.5 Other Designs

- 5.3 By End-user Industry

- 5.3.1 Food and Agriculture

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Pharmaceuticals

- 5.3.4 Building and Construction

- 5.3.5 Mining and Minerals

- 5.3.6 Others

- 5.4 By Capacity

- 5.4.1 Up to 500 kg

- 5.4.2 500 - 1,000 kg

- 5.4.3 1,000 - 1,500 kg

- 5.4.4 Above 1,500 kg

- 5.5 By Material / Polymer Type

- 5.5.1 Virgin PP

- 5.5.2 Recycled-content PP

- 5.5.3 UV-stabilized PP

- 5.5.4 Paper-based Composite

- 5.5.5 Bio-based Polymer Blends

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Greif Inc.

- 6.4.2 Amcor Plc

- 6.4.3 LC Packaging International BV

- 6.4.4 Thrace Group

- 6.4.5 Rishi FIBC Solutions Pvt Ltd

- 6.4.6 United Bags Inc.

- 6.4.7 Bag Corp

- 6.4.8 Bulk Lift International LLC

- 6.4.9 Conitex Sonoco

- 6.4.10 Intertape Polymer Group

- 6.4.11 Emmbi Industries Ltd

- 6.4.12 Schoeller Allibert Group BV

- 6.4.13 BAG Supplies Canada Ltd

- 6.4.14 Southern Packaging LP

- 6.4.15 Plastipak Group

- 6.4.16 FlexiTuff International Ltd

- 6.4.17 Bulk Pack Exports Ltd

- 6.4.18 J&HM Dickson Ltd

- 6.4.19 Houston Bulk Bag Co.

- 6.4.20 Jumbo Bag Corporation

- 6.4.21 Mule Bag Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment